Investing in AI Stocks

- AI’s monetization has shifted from hype to real-world infrastructure, with Nvidia and TSMC leading foundational growth.

- Cloud giants like Microsoft and Amazon are evolving into full-stack AI platforms with sticky enterprise monetization.

- Vertical AI applications in SaaS, healthcare, and automation offer expanding margins and long-term defensibility.

- Key risks include valuation compression, regulatory pressure, and hype dilution—but moats are deepening fast.

TradingKey - Artificial intelligence is no longer frontier technology, but an energetic force that is redefining enterprise software, infrastructure, hardware design, and consumer interaction. From cloud orchestration to application delivery down to the chip level, AI’s commercial presence is building momentum across the board. What used to remain a bet on the distant future has evolved into an arm’s race where the margins, ecosystem lock-in, and efficiency of inference decide the winners. For investors, that’s not just betting on “the next big thing.” It’s identifying asymmetric compounders within an all-new industrial stack.

While the earlier AI bubble had its fair bit of model hype along with GPU speculation, the second has its focus solely on monetizing actual-world inference. Enterprise workflows, infrastructure-as-a-service, along with domain-specific agents are creating steady streams of revenue that can scale into the trillions over the next decade. This sets up the stage for long-duration, cycle-resistant investment chances, if, of course, one knows where to look.

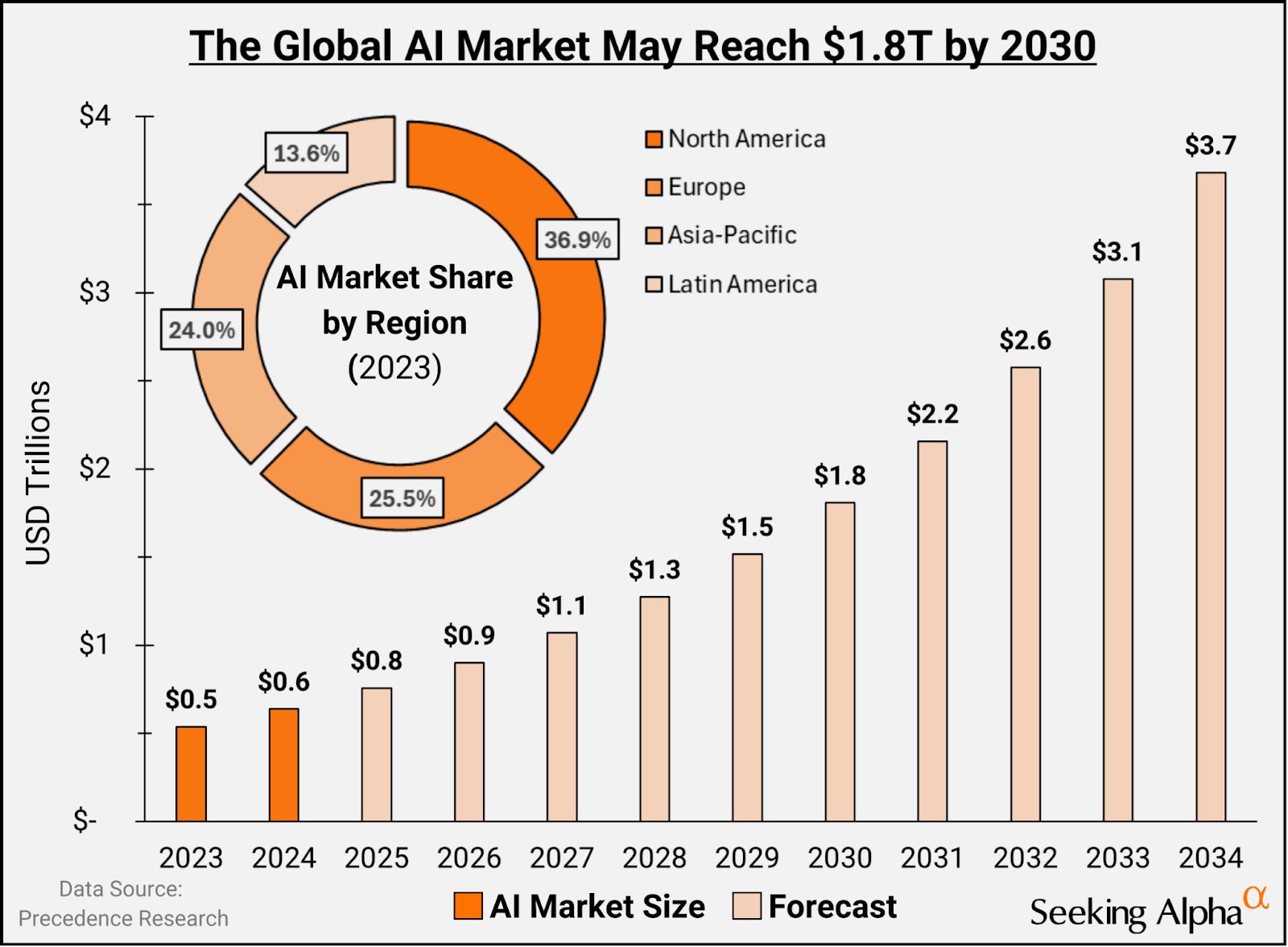

Source: seekingalpha.com

Infrastructure Leaders: Chips, Stacks, and Software Moats

At the heart of the AI ecosystem are those building the necessary compute engines, interconnects, and platforms to scale intelligent systems. Nvidia has become the undisputed AI compute monarch, not only because of GPU dominance but because of a vertically integrated stack from CUDA, networking, to server design. Nvidia is, in many cases, an AI-infrastructure utility more than a chipmaker. Continued free-cash-flow expansion and software-like margins are testimony to broad-based pricing power and customer stickiness.

Nor does the compute story end there, either, as the Taiwan Semiconductor Manufacturing Company (TSMC) remains the ultimate enabler, creating the globe’s most advanced AI chips for Nvidia, AMD, and Apple. Its second quarter reported sustained strength for advanced node requirements, most notably 3nm and 5nm technology, based on AI and HPC orders. TSMC’s dominance of leading-edge capacity for production means that it is amongst the most geopolitically sensitive, but indispensable) players across the value chain.

.jpg)

Source: https://www.ai-supremacy.com

On the other hand, such companies as Broadcom and Rambus are building complimentary AI memory interface design and processing throughput functionalities. These are not very glamorous companies, but they provide us the bandwidth and latency optimization that LLMs and real-time agents need. These business models, often licensing- or semi-custom based, have very attractive recurring revenue business with comparatively low CapEx needs.

Cloud Giants: From Compute Resellers to AI Platforms

With each step of maturity for the infrastructure layer, hyperscalers transform from hardware resellers to application-aware platforms. Microsoft, Amazon, and Google are all moving on from the sale of raw compute to supporting complete AI deployment stacks, including data pipelines, training orchestration, acceleration of inference, and monitoring.

Microsoft is one step ahead of the curve by integrating OpenAI’s models within the Azure stack. Having built generative capability natively into Office 365 (via Copilot), it has created an enterprise-native, high-margin use case monetized per-seat or per-user. It’s that kind of multi-layered monetization investors can only dream of: ground-floor infrastructure tied into business-as-usual use, and very minimal churn risk.

Amazon’s AWS is also still leading the way as the most-complete IaaS provider, but has also started releasing proprietary LLMs and AI-related services. Where Microsoft is for off-the-shelf applications, Amazon is all about developer flexibility and scalability, where clients can take in their own model or use modular services. This has been very sticky for commerce, logistics, and factory clients who are building homebound AI agents.

Google, however, less prominent in cloud market share, has surprised investors with its aggressive AI adoption, including Gemini into search, Google Workspace, and business use of YouTube. Google has one of the largest R&D budgets globally, and its AI activities have as much about building its data leadership and defensibility as they do short-term monetization.

Application Layer: Picking the Winners of the Vertical Race

With maturing foundation models and infrastructure, attention has shifted to vertical AI applications, the narrow, purpose-built products that accelerate productivity, simplify workflows, and optimize domain-specific business. These range from AI-infused CRM applications and code copilots to healthcare diagnosis and self-driving car technology.

Three primary buckets of investors to keep an eye on. Firstly, SaaS products that have AI built-in natively, e.g. enterprise search, integrated data, or integrated customer service. These have high switching costs and rising average revenue per user (ARPU) from paid AI subscriptions.

Second, regulated industries businesses, heath care and finance, that are creating customized AI models approved under compliance processes. These businesses generally enjoy first-mover advantages as well as multi-year enterprise contracts.

Third, automation and robotics companies use AI for the task of optimizing supply chains, self-navigating, and dynamic, real-time decision-making. From farmland to warehouses, what is valuable here is not merely that of cost reduction, but of building entire new business models.

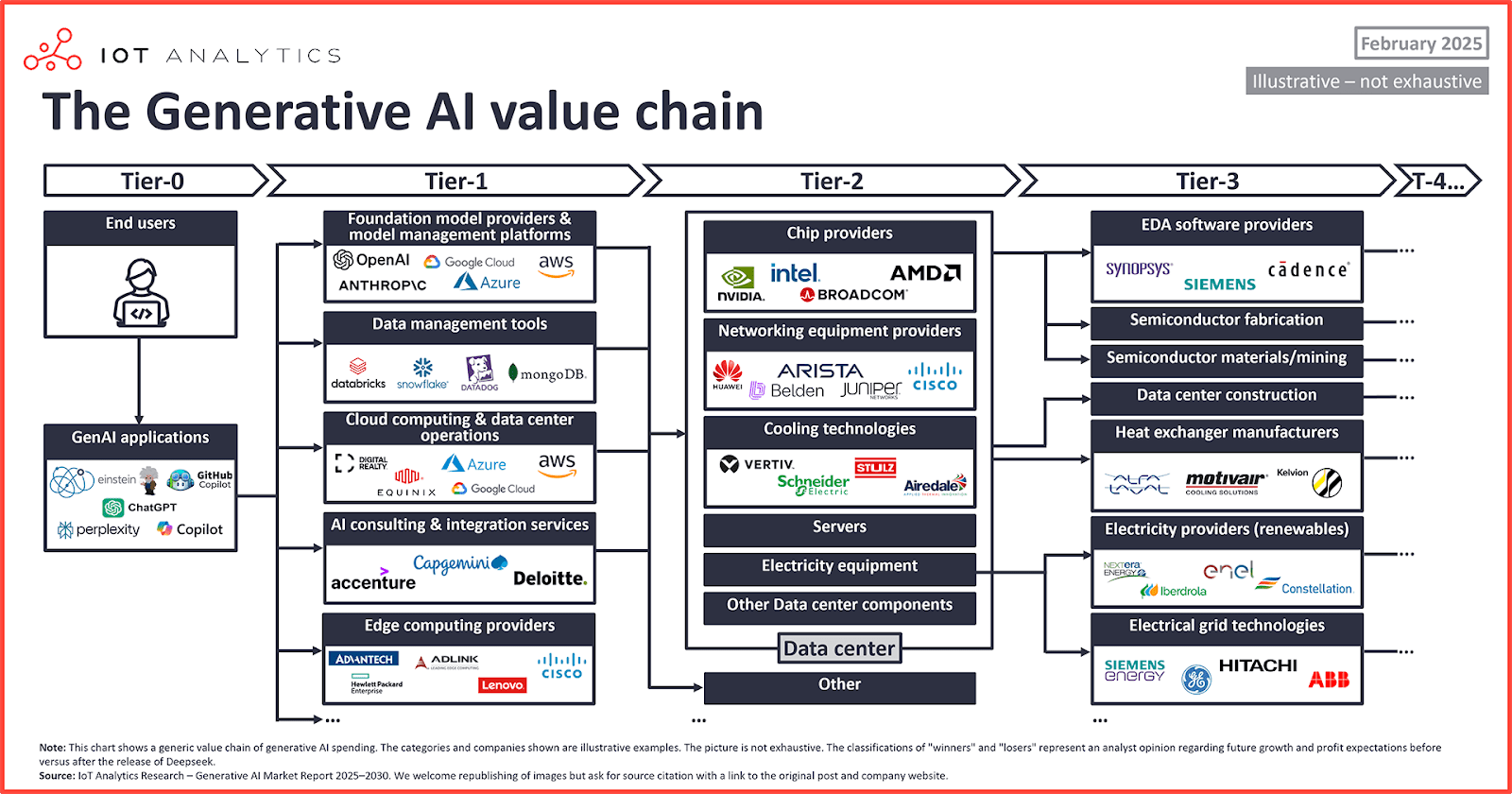

Source: iot-analytics.com

Risks, Metrics, and Long-Term Orientation

Where there is large potential, there is also large noise. AI stocks, and those most susceptible to hype cycles, are prone to violent expansion as well as violent contraction. Investors must separate sentiment-riding companies from those that have true unit economics. There are several key metrics that help to bring analysis back down to earth: use of inference growth, revenue-per-employee, gross margin expansion, and enterprise contract duration. These metrics help to reveal where the AI story is being translated into repeat business performance.

Regulatory is another challenge. From the EU’s AI Act to US Congressional testimony, the regulatory momentum for AI is growing. While large companies for the most part will conform, smaller AI-native start-ups could face disproportionate costs of compliance. Investors must measure legal moats and staying power. Valuation is a persistent tension. Most AI leaders sell at premium multiples, but the earnings power of the underlying business, particularly for the platform players, is growing even faster. Taking the long view, combined with scenario analysis, brings price into balance with potential.

Conclusion: Long-Term Bet on Smart Compounding

AI is not a fad, a tectonic shift in business operation, decision-making, and productivity reaping. Likely beneficiaries that are poised to win are those that sell the infrastructure, administer the cloud ecosystem, or use AI where verticals experience high-friction. Investing in AI today is not about being late to the bandwagon, the hour is about having sustained advantage in an automation-embedded world becoming ever more powered by intelligent automation. For selective, disciplined investors who have a far enough horizon, compounding of the coming decade could have already begun.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.