Alphabet 2Q25 Earnings Comment

Alphabet 2Q25 Earnings Comment

TradingKey - Alphabet (GOOGL) (GOOG) released its earnings for the second quarter of the fiscal 2025 on July 23rd after the bell.

- 2Q25 Earnings per share: $2.31 vs $2.18 estimate (+22% y/y)

- 2Q25 Revenue: $96.43 vs $93.92bn estimate (+14% y/y)

Firstly, the ad revenue remained quite resilient with 10% year-over-year growth, despite the expectations of a slowdown, and if there is any coming slowdown in the global ad spending, the big players like Alphabet and Meta will be rather immune due to their superior AI tools helping advertisers. YouTube recorded 13% annual growth, also above market expectations, and that doesn’t even include the subscription revenue.

Definitely, Cloud business is the most impressive point of these earnings, as not only the growth re-accelerated to 32% (from 28% in the previous quarter) but we saw a significant expansion in the operating margin to 21%. In the previous three quarters there was barely any margin expansion, peaking at 17-18% mostly due to supply constraints when it comes to AI infrastructure and GPU/TPU shortages. Now when we see the removal of this bottleneck, we expect the margin to continue expanding to high 20s-mid 30s.

In terms of Capex, the company increased its projection of spending to $85 billion from $75 billion. Many view this as something negative, but we would disagree with this sentiment. Firstly, we see the capex spending as a necessity to stay competitive in the battle for AI rather than an unnecessary expense. Second, the tariffs will surely have an upside impact on the capex estimates overall, as most of the estimates were set at the very beginning of the year. Third, the very strong cash-generating ability combined with solid balance sheet provides a strong cushion against extra spending.

During the call, the management didn’t share many updates about the ongoing antitrust struggles, however we still expect certain development in the coming months.

Conclusion

The stock went up less than 2% in the post-market session, implying that the market is not so impressed by the earnings. However, the valuation still remains compelling at less than 22x PE.

Alphabet 2Q25 Earnings Preview

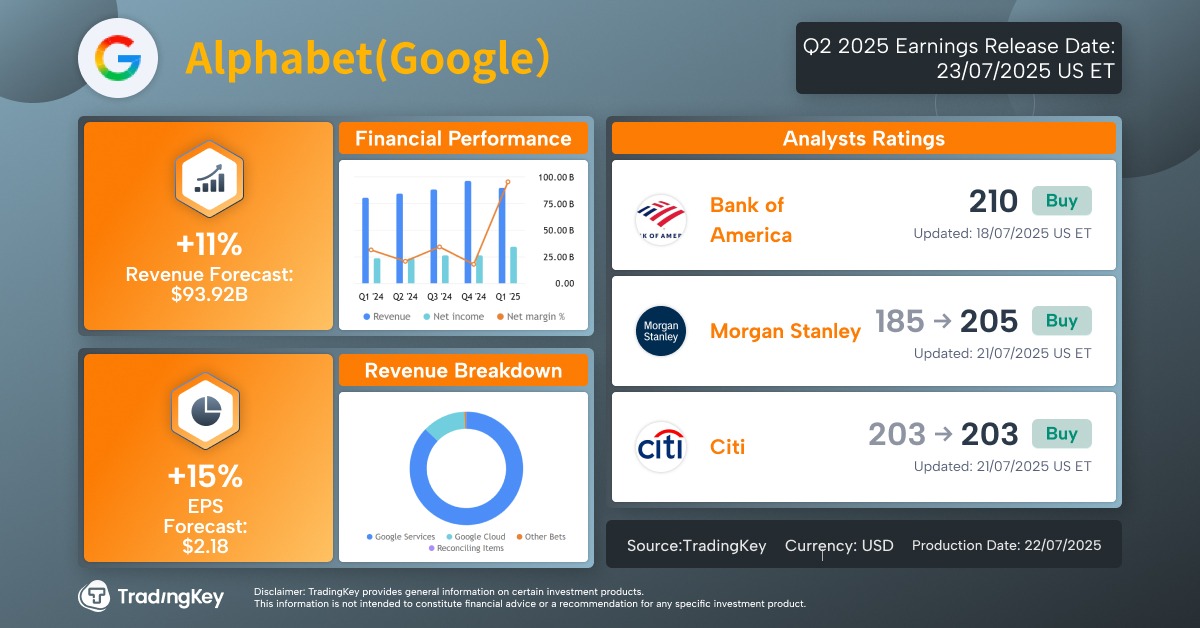

TradingKey - Alphabet (GOOGL) will release its earnings for the second quarter of the fiscal 2025 on July 23rd after the bell.

● 2Q25 Earnings per share: $2.18 estimate vs. 2Q24 actual of $1.89 (+15% y/y)

● 2Q25 Revenue: $93.92bn estimate vs. 2Q24 actual of $84.74bn (+11% y/y)

Honestly, there is a lot to look for in GOOGL’s results this coming week.

Firstly, we have the ad business. The management will give a proper disclosure of the current state of the online ad business, considering GOOGL is the biggest online ad provider. We will see the effect of the tariffs, the economic slowdown. For the ad business, we should pay attention to YouTube, as the platform continues to gain market share in terms of TV time.

Secondly, we have the Cloud and AI story. As the competition with Amazon and Microsoft is quite intense, any wrong step in the cloud direction will be frowned by investors.

We are also curious about the progress of Gemini LLM versus GPT, and what will be the company’s response to the recent efforts by X with Grok and Meta’s huge AI hiring spree.

CapEx spending will be in the spotlight too, as we want to see if there is any tampering of the AI sentiment.

Other aspects that can move the stock are, of course, the autonomous taxi business, Waymo, as well as any updates on the recent anti-monopoly legal battles.

Conclusion

There is a lot being put on the table with these earnings and a lot can get wrong (or right), but what keeps us less uncomfortable about GOOGL is the attractive valuation.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.