Netflix 2Q25 Earnings Comment

Netflix 2Q25 Earnings Comment

TradingKey - Netflix released its 2Q25 earnings on July 17th after the market closure. The earnings for the quarter can be summarized like this:

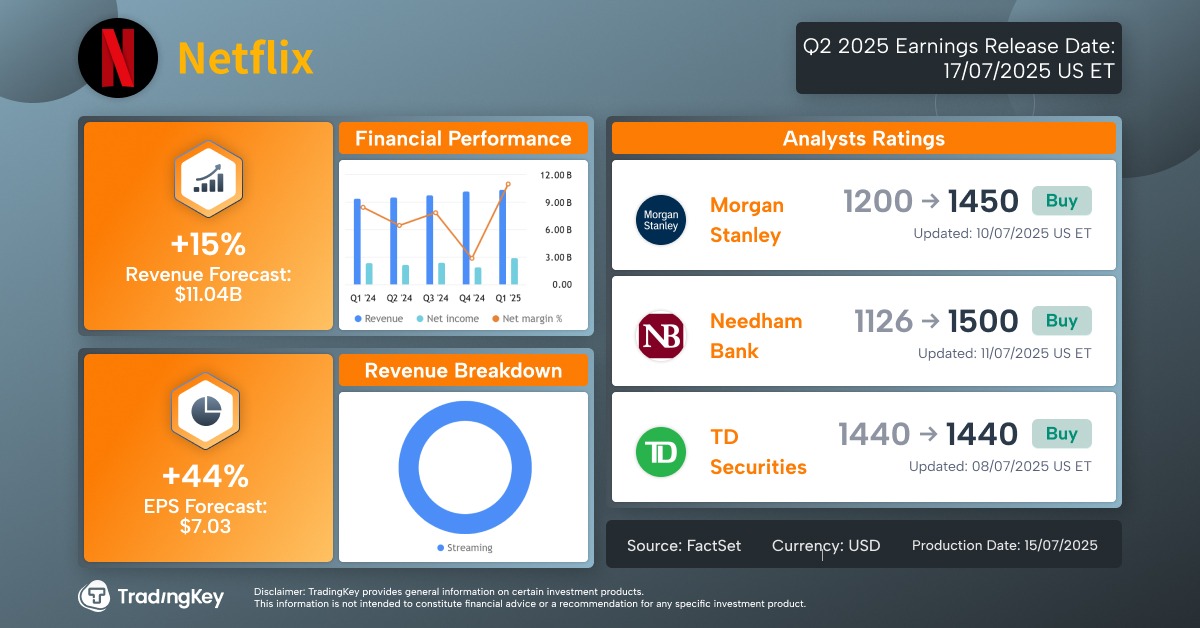

- 2Q25 Earnings per share: $7.19 vs. estimate of $7.03 (+47.3% y/y)

- 2Q25 Revenue: $11.08 billion vs. estimate of $11.04 billion (+15.8% y/y)

The earnings and revenue beat, as well as the alleviated year-end forecast, to a large extent, can be explained by the weakening US dollar. The greenback is an important factor here because roughly 60% of the company’s revenue is from overseas, and the foreign currencies appreciating would mean higher revenue in terms of USD. We believe the investors expected a more confident beat and that’s the reason the stock is down post-market.

Another thing is the operating margin continued to inch higher and higher at 34.1%, and that looks impressive to say at least compared to the 31.7% in 2025Q1 and 27.2% in 2024Q2. But let’s not celebrate too fast, they still have to amortize a bit of content hence the margin expectations for the next two quarters will be below what we saw just now, and the expected full-year margin will be close to 30%

Netflix, also, continues to make strides in ad business with expecting revenue of $3.9 billion for the fiscal 2025, more than double of the $1.9 billion last year.

The company reiterated its solid pipeline of TV shows coming, and also emphasized a bit on the live events, which are an area of huge potential. Netflix will be bidding for the rights to broadcast F1 in the US in 2026; however, we think the chances of getting it are not high, considering Apple is among the contenders.

Conclusion

Business-wise Netflix is doing what it has to do, but the valuation is high and the expectations for some enormous earnings beats are already unrealistic.

Netflix 2Q25 Earnings Preview

TradingKey - Netflix will release its 2Q25 earnings on July 17th after the market closes. The expectations for the quarter are the following:

- 2Q25 Earnings per share: $7.03 estimate vs 2Q24 actual of $4.88 (+44% y/y)

- 2Q25 Revenue: $11.04bn estimate vs 2Q24 actual of $9.56bn (+15% y/y)

The EPS expectations for NFLX are scary high, but how could it be different– the company is firing on all cylinders - the stock price is up 50% since April, margins are hitting new heights, blockbuster content is getting released…

So, what will investors watch on July the 17th?

The content pipeline is strong: Squid Game Season 3 just got released less than two weeks ago, while Wednesday and Stranger Things are expected in the coming months. Regular release of blockbuster shows will keep the level of subscribers. And even though the company will not disclose these numbers anymore, content release will make sure the subscribers’ number is kept in check.

Any plans with regard to content will also be expected from investors, especially in newly penetrated arras such as sports entertainment.

Price increases: As the company is in a rather mature growth stage when it comes to subscribers, the main top line driver will be price increases, rather than subscribers’ growth. Investors will be expecting news with regard to increase in pricing across geography and given that price increase usually comes after successful content releases, expectations are there.

Ad Revenue: Revenue from advertising is still at a nascent level (bellow 10% of total revenue) but the expectations are already high, and the investors closely follow these developments. The push towards ad-friendly content like sports events and WWE shows will be of some help towards diversifying away from the pure subscription revenue.

Conclusion

Netflix seems unstoppable at the moment, with great content, ability to boost prices and emerging advertising revenue. But the higher you climb, the harder you fall.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.