Netflix’s Hidden Transformation Unfolds

- Netflix’s Q1 2025 operating margin reached 31.7%, up 400 basis points year-over-year, with $2.66 billion in free cash flow.

- The company’s proprietary ad tech platform launched in the U.S. and is expanding to 10 new global markets in 2025.

- Live events like WWE RAW and Taylor vs. Serrano are boosting user acquisition and driving new retention flywheels.

- International revenues surged, with APAC growing 23% and LATAM achieving 27% constant-currency growth in Q1 2025.

TradingKey - Netflix’s (NFLX) first-quarter 2025 numbers constituted a turning point, not only for its stock, but for its developing persona as a global monetization and entertainment platform. Consensus opinions still see Netflix as a premium content subscription company, yet the company’s trajectory of finances, as well as its operating disclosures, indicates it is gradually being reshaped as a multi-tentacled digital infrastructure with repeat monetization layers across advertising, games, and live events.

Behind the veil of record operating income and widening margins is a broader metamorphosis: a movement toward precision monetization, control of ad tech, as well as hyperscale content production locally. The investment thesis, as such, rests less on the growth of subscribers, and increasingly on operating leverage, as well as scalable flywheels, supported by solid free cash flow discipline.

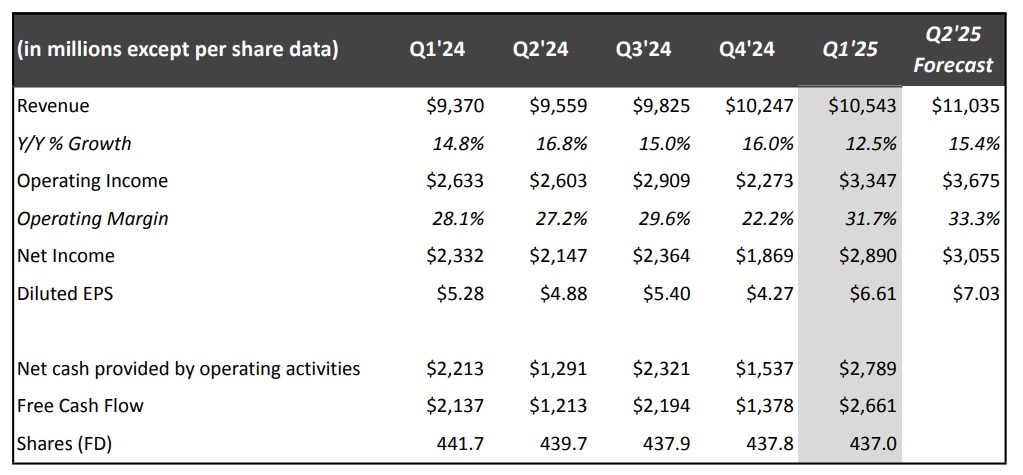

Netflix stock can be said to be priced for perfection, trading on forward multiples higher than its peers such as Disney and Warner Bros. Discovery. Yet its differentiated margin structure, content amortization efficiency, as well as measured discipline on capex, indicate a structurally advantageous business that can re-rate higher. With operating margin for Q1 2025 reaching 31.7%, up by as much as 400 bps YoY, free cash flow of $2.66 billion (+25% YoY) per quarter, Netflix is now experiencing a compounding of margins where each additional dollar of revenue is yielding 2–3 times as much of net income. In such context, the valuation premium is not so much about growth exuberance, as much as it is about carefully managed monetization mechanics.

Source: Shareholder letter

From Studio to Platform: Expanding the Netflix Business Model

Netflix’s evolution from a streaming company with a global reach to a vertically integrated content-tech hybrid has proceeded quietly so far in 2025. No longer does it only distribute content of the highest quality, it monetizes it through layered ecosystems of participation, information, and IP extensions. Its new first-party ad technology platform debuted in the U.S. during April and is being introduced to 10 further markets. In contrast to rivals that have outsourced their ad infrastructure, Netflix owns the full stack, giving it total control over targeting, pacing, and inventory control. The choice of internalizing ad tech is reminiscent of the earlier model of internalizing key value chain elements by Amazon for driving margin growth.

Live content is another undervalued growth driver.

With live events such as WWE RAW now appearing on Netflix’s global Top 10 for several weeks and the Taylor vs. Serrano rematch set to break new record levels, Netflix is fast becoming the destination of choice for appointment viewing. Critically, they’re not only brand extensions, these are user acquisition drivers with downstream effects on retention. Although only a fraction of total view hours, management assured that live content generates “outsized positives around acquisition and conversation” with an asymmetrical ROI profile.

Gaming is early-stage but indicates intelligent capital deployment. Instead of over-focusing on initial investment, Netflix is layering immersive, IP-anchored games such as Squid Game: Unleashed and Black Mirror's Thronglets that create universe expansion of established hits. Notably, spend on gaming is still low as a percent of total cost of content, implying option value upside with balance sheet support.

A Global Gauntlet: Competitive Positioning through Localized Scale

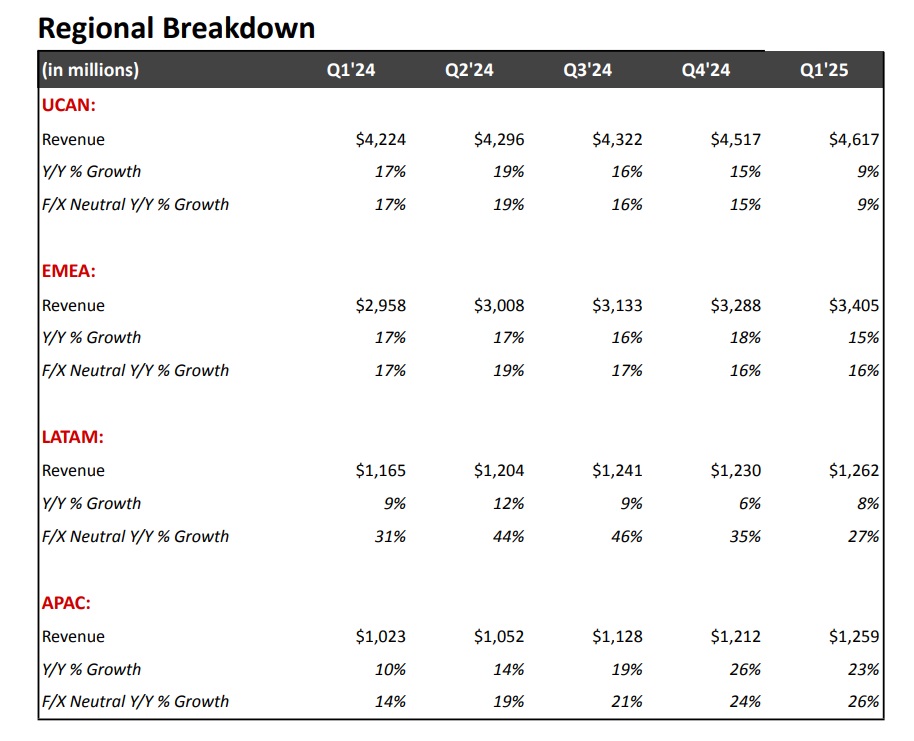

Whereas Netflix dominates world-wide streaming by view share, it is a minority player by total TV time, fewer than 10% in most markets. But it is taking share methodically through regional execution rather than world-wide homogeneity. In Q1 2025, revenues of UCAN grew only 9% YoY, slowing from 15% growth in Q4, but much of that reflects phasing of price increases as well as absence of NFL-driven advertising revenues in Q1. By contrast, revenues rose 23% in the APAC region and 8% in LATAM, with constant-currency growth in LATAM reaching 27%, confirming Netflix’s localization approach.

This international reach is underpinned by deep regional infrastructure. Netflix now creates original series from more than 50 territories and has committed over $6 billion of investment in the U.K. creative industries since 2020. In Q1, it had in excess of 28 stages of production up across Shepperton, Longcross, and Uxbridge studios, driving hits such as Adolescence, the U.K.'s top-rated streaming title, as well as one point of share gains for Netflix for TV time (up from 8.0% to 9.0%).

Netflix’s moat is not only content here, it’s operational latency and IP logistics. Localized staff with deep roots among creators, production facilities near story ecosystems, and live data feedback loops enable Netflix to iterate before competitors can. Disney, Prime Video spend in international content, whereas the scale, cultural specificity, and logistics alignment enable Netflix’s international expansion to be more defendable.

Source: Shareholder letter

Precision Monetization: Where Financial Discipline Meets Layered Growth

The monetization maturity of Netflix can be seen through its income statement as well as its capital deployment. Q1 revenue stood at $10.54 billion, up 13% YoY. The operating income grew by 27% to $3.35 billion. Particularly, the outperformance came from higher-than-projected ad as well as subscription revenues with less-than-expected expense timing, a reflection of execution accuracy. The diluted EPS rose to $6.61, up by 25% YoY, well surpassing the consensus of $5.68.

This profit growth is not coincidental, a function of intentional trade-offs. Netflix achieved operating margins of over 31% even as it ramped up ad infrastructure, grew live content, and spent on games. CFO Spencer Neumann noted that fluctuations are a function of content slates, not cost inefficiency. 29% is still the full-year guidance, including additional content launches and Q3–Q4 sales ramp.

The biggest short-term lever of margins is advertising. Proprietary ad technology is now live, and programmatic capabilities are expanding seasonally across EMEA, as well as across LATAM. Netflix is hoping to double advertising revenue in 2025. Although still a small portion of total revenue, their incremental margin contribution (well north of 60%) could have disproportionate effects on operating income.

Capital discipline is still stringent as well. Free cash flow reached $2.66 billion for Q1, up from a year ago at $2.14 billion, and Netflix reiterated full-year FCF of $8 billion. Share repurchases amounted to $3.5 billion for the quarter, leaving the company with $13.6 billion of remaining authorization. Debt is under control with $7.2 billion of cash for only $15 billion of gross debt, and refinance maturities are financed.

.jpg)

Source: Shareholder letter

Valuation: High Multiples, Justified by Platform Economics

Netflix is trading on higher forward multiples, 43x P/E and 11x EV/Sales, standing 157% and 495% higher than the sector median. However, such valuations are 11–12% less than Netflix’s own 5-year averages, indicating investors are paying less for structurally higher earnings quality. The PEG ratio (1.8x FWD) is only slightly above peers, as it indicates the growth premium is not out of control considering widening monetization through ads, live events, and gaming.

More significantly, Netflix turns revenue into profit with a speed unchallenged by competitors. On $2.66B of Q1 free cash flow, with a goal of $8B by 2025, the yield on free cash flow is a healthy 3.2% based on a 31.7% operating margin and capital-light growth. Old fundamentals seem stretched, but they miss Netflix’s transition to a monetization platform. The valuation is not low, but it’s reasonable based on its earnings leverage and multi-layered top-line model.

Conclusion

Netflix transitioned from being a growth stock to a monetization engine for a platform, now one that is starting to unlock the operating leverage investors had for so long expected. The company's competitive advantage is no longer based solely on content, however, but rather its power to layer on high-margin businesses (ads, live events, games) over an enormous user base, while being financially disciplined with a dominance of FCF. With expanding margins as the new flywheel, the trajectory for structurally higher profits looks not only feasible but probable.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.