[IN-DEPTH ANALYSIS] Tesla’s Robotaxi Ambition Amid the Trump-Musk Political Tensions

TradingKey - Key Takeaways

· Political Feud Impact: Musk’s clash with Trump risks Tesla’s subsidies and SpaceX’s federal contracts, essential for growth.

· Robotaxi Opportunity: Tesla’s scalable robotaxi could have great potential but faces regulatory and competitive hurdles.

· Valuation Insight: Tesla’s $450/share target reflects our balanced growth assumptions in auto, energy and service segments.

Source: TradingKey

Musk vs. Trump: The Public Fallout

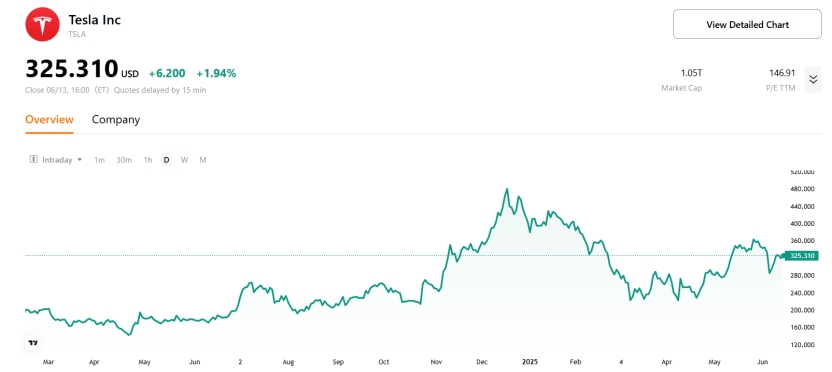

Trump and Musk recently got into a verbal fight on social media and triggered a significant correction in Tesla’s stock price. According to New York Times, the fight began when Trump suddenly withdrew his nomination of Jared Isaacman to lead NASA after learning Isaacman had donated to Democrats during election. Isaacman is Musk’s close friend and an important partner for SpaceX’s NASA projects. This embarrassed Musk because he recommended Isaacman to Trump. Soon after, Musk publicly criticized Trump’s Big Beautiful Bill, saying it would increase the national debt and undo DOGE efforts.

Source: X

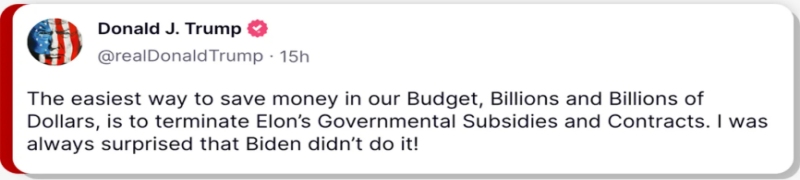

The conflict quickly got worse. Trump responded by threatening to cut federal contracts and subsidies for Musk’s companies, including Tesla and SpaceX.

Source: Truth Social

Musk later softened his tone and apologized for some harsh comments. Trump also said he was open to making peace, though he didn’t rush to fix their relationship. For Tesla, government incentives have been key to staying profitable, while SpaceX depends on NASA and military contracts for its revenue.

Reliance on Government Support

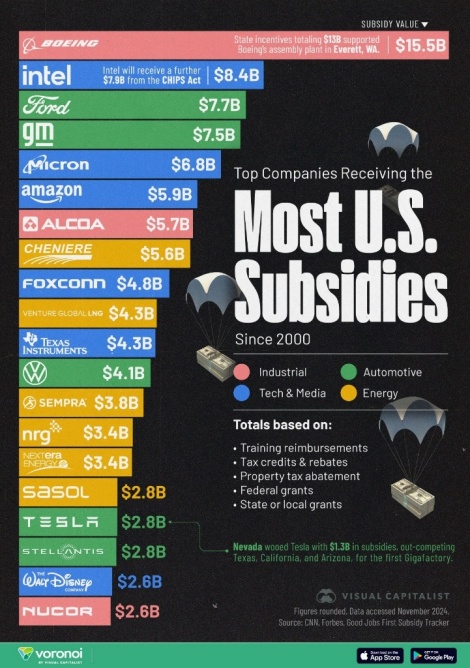

Regulatory credit is a critical factor in Tesla’s profitability. While these credits represent less than 3% of Tesla’s total revenue, they contribute around 25% to 30% of net income. In fiscal 2024, Tesla earned a record $2.76 billion from selling regulatory credits, and in the first quarter of 2025 alone, it generated $595 million. These credits are essentially pure profit, as Tesla produces zero-emission vehicles and sells these credits to traditional automakers who need them to meet emissions standards. Without this income, Tesla would have reported losses in recent quarters, showing how vital these credits are to its financial health.

Source: Visual Capitalist

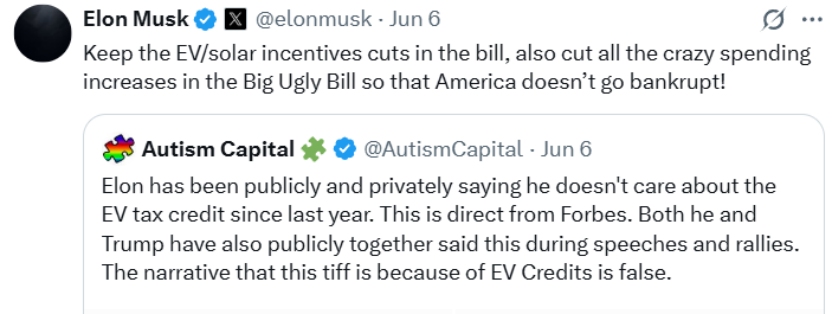

However, proposed policy changes, such as efforts by Senate Republicans to eliminate penalties under the Corporate Average Fuel Economy (CAFE) standards, threaten to dismantle the market for these credits. Musk has publicly downplayed the importance of these subsidies. He has framed Tesla’s success as driven more by innovation and scale rather than by government incentives and argued that removing these credits would hurt competitors more than Tesla itself.

Source: X

Despite Musk’s public rejection of relying on government support, Tesla’s profits still depend a lot on money from government programs. That could explain why Musk tries to keep good relationships with politicians from all sides, including trying to make peace with Trump despite their disagreements, to protect these important sources of revenue.

Meanwhile, SpaceX operates independently from Tesla, with its own distinct financial and business model. According to Elon Musk’s recent tweet, SpaceX is projected to generate approximately $15.5 billion in revenue in 2025, up from an estimated $13.1 billion in 2024. This growth is largely driven by two main segments: its Starlink satellite internet service, which is expected to generate around $12.3 billion and serves millions of subscribers worldwide, and second is its launch services business, including government and commercial rocket launches.

Government contracts contribute significantly to SpaceX’s revenue. NASA contracts are expected to provide roughly $1.1 billion annually, supporting high-profile missions such as the Roman Space Telescope, Europa Clipper, and crew and cargo transportation to the International Space Station (ISS), with agreements extending through the ISS’s anticipated retirement around 2030. The U.S. Space Force awarded SpaceX approximately $5.9 billion in contracts covering 28 national security space launch missions, primarily scheduled between 2027 and 2032 under the National Security Space Launch Phase 3 program. This implies an average annual revenue of about $1 billion from Space Force contracts during those years.

Although Tesla and SpaceX are separate companies with independent operations, Musk’s political challenges inevitably affect both, given their shared reliance on public sector support and regulatory environments. Musk’s ability to navigate these political waters is critical to sustaining the growth and profitability of both enterprises.

Robotaxi Debut

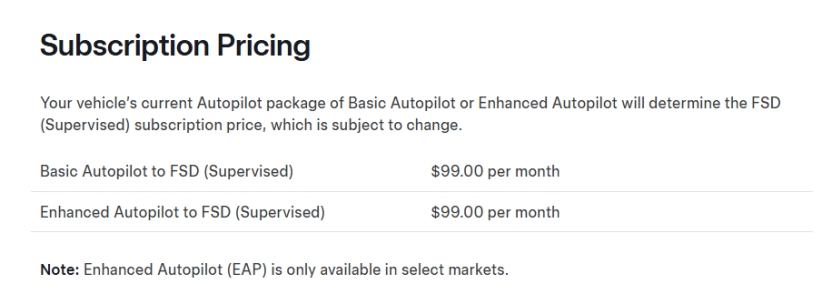

Turning to Tesla’s much-anticipated robotaxi program, recent developments have captured the attention of investors and industry watchers. Currently, Tesla is testing about ten robotaxis in Austin, Texas, with ambitious plans to expand the fleet to 1,000 cars in the coming months.

These vehicles are equipped with Tesla’s Full Self-Driving (FSD) software. Tesla’s FSD software contributes significantly to Tesla’s software and services revenue. Subscription plan as follows:

Source: Tesla

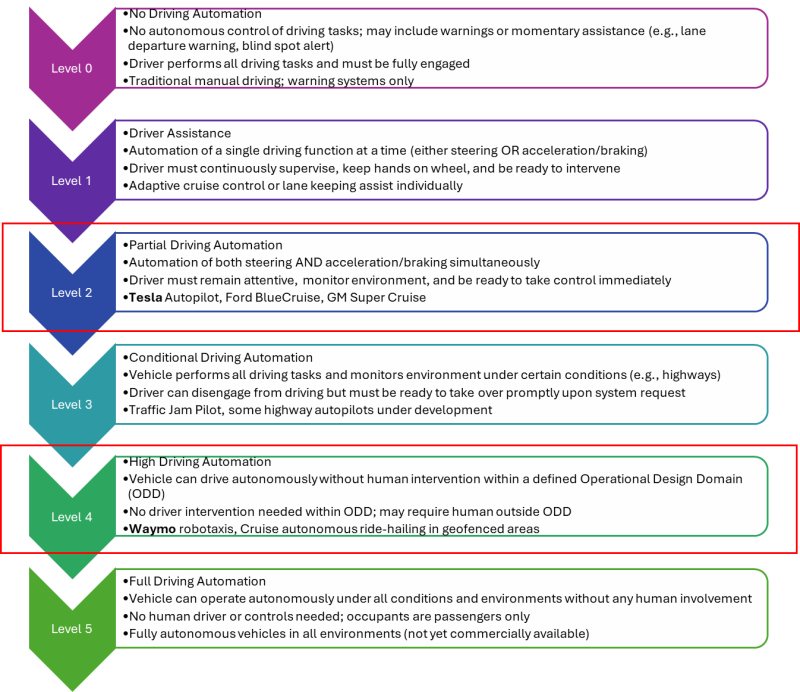

However, the autonomy level of these robotaxis remains ambiguous. If remote human drivers are in control or ready to intervene, the system aligns with SAE Level 2 automation, this is where Tesla is for now. For Tesla to reach Level 4 where vehicles operate fully autonomously within a defined operational domain without human intervention, it must demonstrate that its cars can handle all driving tasks independently.

Source: CarADAS, TradingKey

The National Highway Traffic Safety Administration (NHTSA) has expressed concerns and requested more operational data to evaluate safety, highlighting the regulatory hurdles Tesla faces.

Tesla Vs Waymo

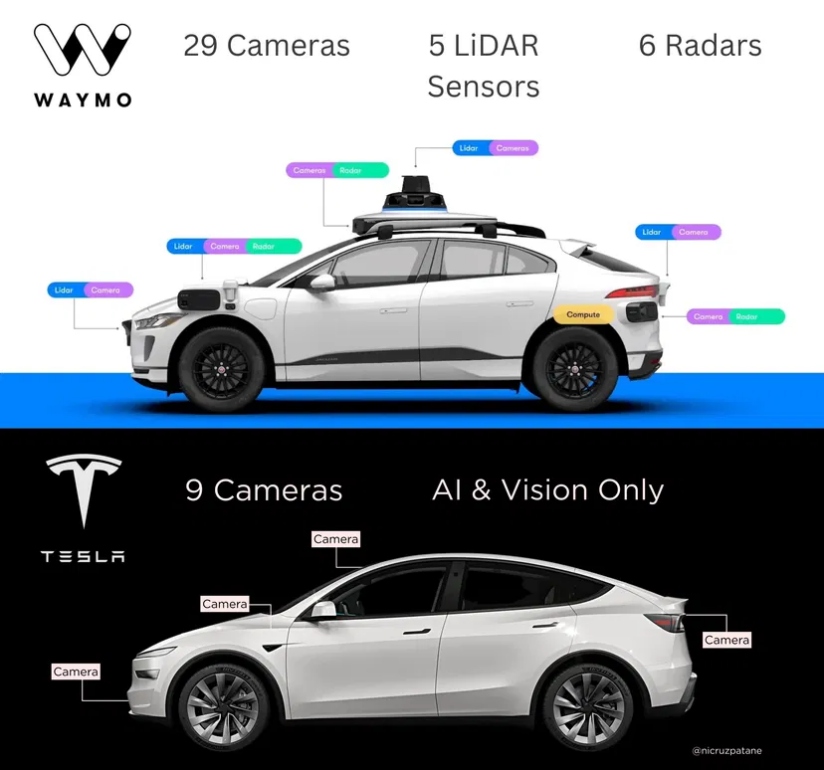

Comparing Tesla’s approach to that of Waymo (Alphabet’s autonomous vehicle subsidiary) reveals contrasting philosophies. Waymo’s vehicles are classified as Level 4 and use a sophisticated sensor fusion system combining 29 cameras, 5 lidar sensors, and 6 radars to ensure robust perception in diverse weather and lighting conditions. It relies on pre-mapped 3D maps. Business Insider and SwipeFile data from 2025 indicates Waymo’s sensor suite costs approximately $9,300 per vehicle, roughly 23 times Tesla’s sensor cost. This sensor redundancy provides greater environmental awareness and safety margins but comes with much higher upfront costs and operational complexity.

Tesla, on the other hand, relies exclusively on a vision-based system with 9 cameras and neural network AI, rejecting lidar and radar. BloombergNEF estimated the cost of Tesla’s camera-based sensor hardware is around $400 per vehicle. This minimalist hardware approach reduces costs and simplifies scalability but places enormous pressure on Tesla’s AI software to compensate for the lack of depth and redundancy in sensing.

Source: SwipeFile

The business models also differ. Tesla’s low-cost sensor suite enables rapid fleet scaling. Tesla produces thousands of vehicles daily, all potentially upgradable via software to robotaxi capabilities. Musk envisions a decentralized robotaxi model where individual owners can rent out their vehicles on Tesla’s network like Airbnb but for cars. Owners potentially can earn around $30,000 annually per vehicle. This leverages Tesla’s large production volume and real-world driving data from hundreds of thousands of vehicles equipped with FSD to continuously improve its AI performance.

Waymo operates a company-owned fleet of around 1500 cars, expected to grow to 3,500 by 2026, primarily Jaguar I-PACEs equipped with Waymo’s self-driving technology, and provides ride-hailing services in select U.S. cities. Waymo One, Waymo’s own ride-hailing service operating mainly in Phoenix, San Francisco, and Los Angeles, accounts for roughly 70–80% of Waymo’s fleet and trips. The remaining 20–30% of Waymo’s autonomous vehicles operate through its partnership with Uber, primarily in cities like Austin and Atlanta where Waymo robotaxis are available exclusively via the Uber app. Uber usually takes 10-20% of commissions and Waymo keeps the rest according to New York Times.

As of April 2025, Waymo provides over 250,000 paid robotaxi trips per week across Phoenix, Los Angeles, San Francisco, and Austin, according to Waymo’s official announcements, significant growth from 200,000 weekly trips in February. This translates to roughly 35,700 trips per day. Morgan Stanley projects Waymo’s revenue to reach approximately $181 million in 2025.

In Austin, Waymo robotaxis accounted for about 20% of all Uber rides by March 2025, showing strong consumer adoption shortly after the partnership launch. This collaboration allows Waymo to leverage Uber’s large customer base.

Waymo’s scale remains modest compared to Tesla’s massive car production capacity. While Tesla manufactures thousands of cars daily, Waymo vehicles are produced by partners like Jaguar and Magna, with plans to build over 2,000 annually at the new Arizona facility. This scale advantage, combined with Tesla’s AI-centric strategy, could prove pivotal if Tesla can overcome safety and regulatory challenges. Tesla’s planned robotaxi service (Cybercabs) could scale to 1,000 vehicles within months of launch, showing its potential for rapid fleet expansion compared to Waymo’s more partnership-dependent and capital-intensive model. Waymo’s fully driverless vehicles have driven about 56.7 million miles across their main markets (Phoenix, San Francisco, Los Angeles, and Austin) as of early 2025, while Tesla’s Full Self-Driving (FSD) fleet has collectively driven over 3.6 billion miles using its supervised autonomous system by early 2025.

Company | Miles Driven (Autonomous) | Notes |

Tesla | ~3.6 billion miles (driver supervised) | Supervised miles driven by a large fleet of consumer FSD-equipped vehicles; human driver always ready to take control |

Waymo | ~56.7 million miles (fully driverless) | Fully driverless miles in geo-fenced urban areas without human intervention |

Source: The Verge, Tesla North Blog

The NHTSA’s investigation shows the challenges Tesla faces in proving that its vision-only system can match or exceed the safety of human drivers. Elon Musk’s insistence on a camera-only approach is rooted in his belief that human vision is the ultimate model for autonomous driving. While this approach has the advantage of lower sensor costs and simpler hardware, it struggles with inherent limitations like depth perception errors and bad weather conditions. In contrast, Waymo’s sensor fusion provides richer environmental data

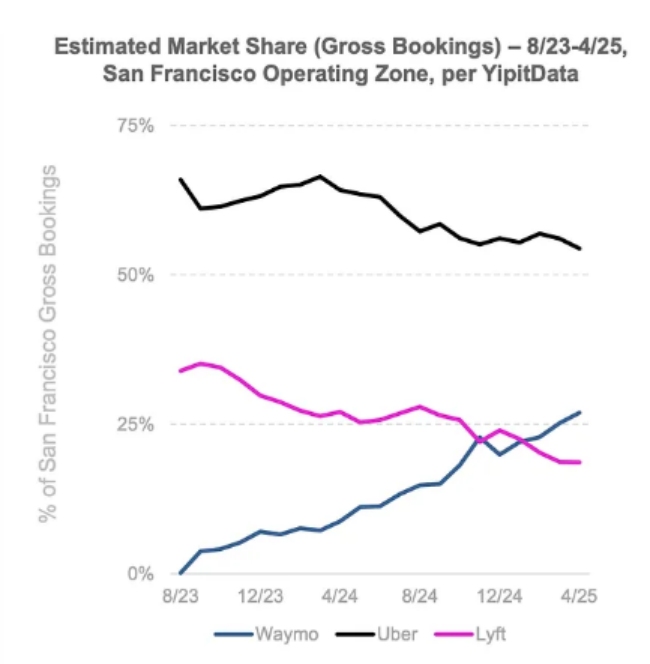

Ultimately, Tesla focuses on using its software and large-scale car production to make fully self-driving cars profitable, while Waymo puts more emphasis on having extra sensors and building very reliable systems. Both approaches have advantages and challenges, and the coming years will reveal which philosophy prevails. However, Waymo has a first-mover advantage, with its market share continuously growing.

Source: Bond Capital

Valuing Tesla: What’s Priced In, What’s at Stake

Tesla’s market value is not just about how many cars it sells or how many rockets Musk launches (this doesn’t affect Tesla’s revenue but will encourage market sentiment). The company’s stock price reflects a bet on a future where Tesla is more than a carmaker, it’s a software powerhouse (FSD), a big data &AI company (xAI), and possibly the world’s first truly scalable robotaxi platform (Cybercab).

Our assumptions:

· Core car business: In 2024, $77 billion in auto revenue and $14 billion in gross profit. We assume there is no growth in auto revenue and gross profit accounting for the fact Tesla sales are dropping in 2025. If the regulatory credits are cancelled, then gross profit will reduce from 14 billion to $12.8 billion.

· Regulatory credits: They contributed $595 million in Q1 2025. These credits are at significant risk due to a provision in Trump’s Big Beautiful Bill, currently being considered by the Senate Committee on Commerce, Science, and Transportation. This provision will effectively end the need for automakers to purchase regulatory credits like those Tesla sells. The bill is likely to pass in 2025, and if enacted, the changes are expected to take effect in the second half of the year, which means about 50% of profit from regulatory credits could be lost.

· Energy sector: $10 billion revenue in 2024. If the solar and storage expansion continues, using TTM Q1 2025 energy revenue growth of 80%. In 2025 revenue from energy is assumed to be $18 billion and 27% gross margin gives gross profit $4.86 billion.

· Services: $10 billion revenue in 2024, using TTM latest Q1 service revenue growth rate of 24% increase in 2024 and adding 250 million additional revenues from higher FSD take rate. The revenue in 2025 is assumed to be $12.65 billion. with gross margin 5.82%, 2025 gross profit is $736 million.

· Software and FSD: Tesla’s Full Self-Driving software, sold for $99 per month ($1188 annually). Total Tesla cars on road are about 5 million globally. In 2024, approximately 6% use FSD by industry estimate, that’s about $350 million. If 10% of Tesla’s fleet subscribes, that’s $594 million revenue a year, so around $250 million revenue is added.

Adding all three sectors’ gross profit gives $18.4 billion, which translates to net profit of $8.65 billion, assuming 47% (average of last 5 years) of gross profit can be converted to net profit. With 3.5 billion shares outstanding, EPS would be around $2.5.

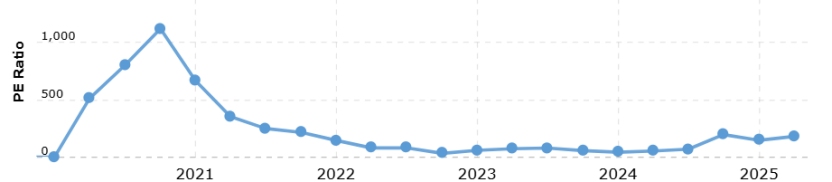

· Robotaxi dream: If Tesla’s robotaxi dream works, even in just a few cities, the upside is huge. According to Statista, the global ride-hailing market is expected to reach about $180 billion in total bookings by 2025. If Tesla captures 5% of this market and keeps 15–20% of the fare as revenue, its robotaxi business could earn between $1.35 billion and $1.8 billion each year. Although widespread robotaxi deployment is unlikely to happen in just one year, Tesla starting to test robotaxi indicates a pivotal step toward its goal. The market has already partially priced in this potential, which helps justify Tesla’s current high P/E (180). Given the difficulty of disproving Tesla’s robotaxi success at this stage, we apply a premium P/E of 180 to reflect continued investor optimism.

Source: Tesla’s historical PE from Macrotrends

Under our current assumptions, Tesla’s target price is projected to reach around $450 per share. This reflects a balanced but bullish view, recognizing both the company’s strong potential and the challenges it faces.

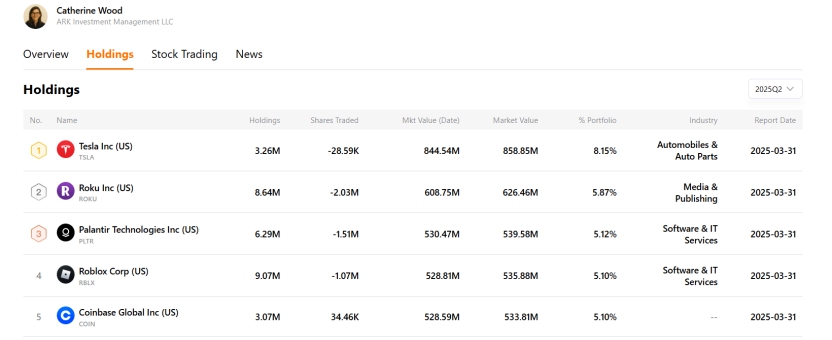

Tesla’s bold robotaxi strategy has also drawn strong support from investors like Cathie Wood, whose ARK Innovation ETF holds Tesla as its top position. Wood sees Tesla’s AI-driven approach as a ‘winner-take-most’ opportunity, projecting a $2,600 stock price by 2030. Learn more about her visionary bets at TradingKey’s Star Investors:

Source: TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.