[IN-DEPTH ANALYSIS] LULU: Can it Recover from the Drop?

Source: TradingView

TradingKey - Thesis

Among the stocks of the twenty largest clothing companies by revenue, Lululemon has the fifth lowest forward PE ratio. With all the negative sentiment revolving around the stock, we believe their multiple should be higher. The negative aspects such as suppressed consumer spending, margin headwinds from tariffs and intensified competition in athleisure are most likely already priced in. At the end of the day, Lululemon remains a household name in the apparel industry, with growth opportunities in both overseas and men’s wear.

Takeaways from the Latest Earnings Release

The recent earnings release put Lululemon in a nosedive with a 20% drop in the share price, despite the fact that the revenue and the earnings guidance were met:

· Earnings per share: $2.60 vs. $2.58 expected (+2.4% year-over-year)

· Revenue: $2.37 billion vs. $2.36 billion expected (+7.3% year-over-year)

So, what made investors so spooked?

On the top line, the struggles in the US market continue with revenue growth still at low single digits and apparently the growth was driven by store expansion, considering the same store growth in their biggest market was actually -2%.

The full year EPS guidance was revised down from $14.95-$15.15 to $14.58-$14.78 which is almost identical to the EPS for the previous fiscal year, implying barely any earnings growth. The main reason behind this is the uncertainty over the tariffs.

Inventory position is another aspect that rings an alarm with inventory up 14% just within one quarter. However, the increase in inventory may imply potential front-running of costs, as the company is trying to buy as many raw materials as possible before the price increases take place.

On the top of this, the announced price increase for some of the products will partially help offset the margin headwinds but this may potentially result in lower growth near-term and more inventory will pile up.

Enough Reasons not to be so Scared

A lot of the worries come from macro factors such as suppressed consumer spending. However, we should bear in mind this affects the whole industry, not just Lululemon.

As for the tariffs, lowered guidance due to uncertainty is something we have already seen in other clothing brands’ earnings reports. It is true that Lululemon has a lot of exposure to overseas suppliers, but unlike other peers, Lulu is mostly reliant on Vietnam and on a very little extend on China. This is good news for the company because trade talks between the US and Vietnam have the potential to be much less politically charged and complex as the trade talks with China, making it easier for Lulu to get rid of the tariff burden.

Also, for Lululemon specifically, there is a solid pattern of revenue cyclicality. Lulu is a premium brand which is often used for gifts, therefore the last quarter of the fiscal year (when the holidays are) has way more weight. Thus, low growth numbers now have a rather limited effect on the final year’s guidance, giving precious time for the company to improve its operations in the meantime.

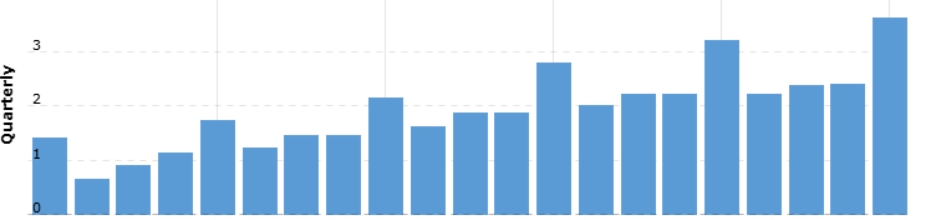

Source: Macrotrends

Lulu and the Athleisure Competition

As the above-mentioned factors are rather temporary and affect all the industry players in the same way. Competition from emerging athleisure brands, however, is often seen as a sign that Lululemon as a brand is becoming less relevant. Two such brands are Alo and Vuori.

In some ways, they follow a lot of the tactics of Lululemon – targeting consumers in urban areas with heavy emphasis on DTC. Alo Yoga and Vuori have both allegedly reached $1billion of annual sales with revenue growth way above 20%. Their following on Instagram is catching up with Lululemon.

Source: Instagram

Despite this, an intense competition in the athleisure market is not so probable.

First of all, no matter how similar the two companies are to Lululemon, there are certain differences between the targeted customer base. The average customers buying Alo and Vuori are more likely to be girls in their 20s, closely following influencers. Lululemon as a relatively older brand caters for more mature customers in their 30s and 40s.

Secondly, the athleisure industry is a subsegment of the broader apparel sector. The apparel industry has a different structure than other sectors. In other sectors, it is more common to see a more apparent dominance of one or a very few market players. For example, we can see Nvidia dominating the GPU market, Amazon dominating the American e-commerce market or Meta and Alphabet dominated the online advertising market.

This kind of dynamic will not happen in the clothes business, simply because for consumers, clothes are a way of self-expression.

In the tech industry we can say that iPhone is the best phone brand, Nvidia chips are the best for AI and Google is the best search engine, but we cannot say which is the best luxury cloth brand or the best athleisure brand. Some people may like LV, some people may like Chanel, some people may like Alo and some people may like Lululemon. Thus, we don’t believe other brands may cause existential threat to Lululemon.

Valuation

After the major drop, LULU is trading at around 17 times the projected full-year earnings. We can see this valuation from two contexts – compared with the historical PE ratio and compared with peers, and in both cases we can see a massive discount at the current price.

At the moment, LULU’s PE ratio is at historical low, compared with the average of around 30x.

Source: Macrotrends

In order to get a clearer picture of the industry we also compiled a list of the largest clothing brand stocks by revenue and their respective valuation. It appears that lululemon has the fifth lowest PE right after Dior, JD Sports, VF Corporation and PVH. The majority of the other peers are traded in their 20s. Even Nike, experiencing one of its most difficult periods ever, is traded at nearly 30x.

Source: Yahoo Finance

It is also worth mentioning that the management has been quite aggressive in repurchasing the stock. Just within two years the diluted outstanding shares went from 128 million to 121 million, demonstrating the management conviction that the stock is undervalued.

Source: TradingKey

We do not expect a quick recovery in the LULU share price, as the negative sentiment will weigh for a while. However, the risk reward ratio seems quite favorable, with more clarity on tariffs as the time goes, we can see the upside.

Lululemon attractive business model has also drawn strong support from some of the largest institutional investors such as Vanguard Learn. Learn more at TradingKey’s Star Investors:

https://www.tradingkey.com/tools/star-investors/the-vanguard/portfolio

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.