[IN-DEPTH ANALYSIS] Does Walmart Deserve its High Valuation?

TradingKey - Investors tend to misunderstand Walmart‘s business(WMT.US). We should no longer see it as a mature supermarket chain with growing e-commerce arm, but more as a e-commerce business with a very strong network of fulfilemnt centers (physical stores) and various growing business lines to support the e-commerce. The valuation may seem hefty at first sight, but with a very high level of business execution, limited downside in revenue and large opportunity in grocery e-commerce ahead, Walmart surely deserves a high PE. Moreover, Amazon in its high growth stage during the 2010s was constantly traded at 60x PE or above, implying more room for Walmart stock to grow.

Source: TradingView

Takeaways from the Latest Earnings Release

The feelings towards Walmart 2026Q1 earnings were rather mixed with some positive developments but also concerns:

● Earnings per share: 61 cents, adjusted vs. 58 cents expected (-3.1% year-over-year)

● Revenue: $165.61 billion vs. $165.84 billion expected (+2.5% year-over-year)

On the bright side, the earnings per share beat the expectations. Inventory seems to be well managed, thus markdowns are still on the lower side. Advertising is growing fast - up 31% year over year, and that’s excluding the Vizio smart TV business, the company acquired last year. Membership revenue is accelerating. Most importantly, ecommerce inflected to profitability for the first time in the business' history.

On the not-so-bright side, the company is facing uncertainty with the tariffs and economic slowdown. Walmart is also facing a political pressure to absorb the cost impact, so as to hold prices steady.

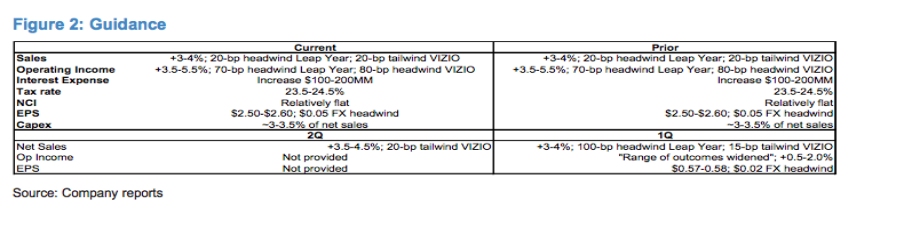

Guidance

For 2026FY, the management reiterated its guidance, showcasing the underlying resilience of WMT's business. However, for Q2, WMT expects net sales +3.5-4.5% (vs. Street +3.3%) but this comes without guidance for Operating Income and EPS, sending a message to investors that the situation will still remain quite uncertain in the near future.

Source: Company Presentation

Beyond the Tariffs and the Economic Slowdown

The company can maneuver the tariff volatility better than competitors, through the diversification of its revenue streams across membership and advertising, as well as a more favorable product mix. However, in order to see the true value of Walmart, we have to look longer-term, beyond the tariffs and the macro headwinds.

E-commerce as the Centerpiece of WMT Business Model

Walmart posted its first profitable quarter for its e-commerce business both in the U.S. and globally, which is a major milestone.

The company does not disclose the exact operating profit of the e-commerce business. However, we believe the outlook is quite positive:

First, Walmart is primarily a grocery business with 60% of the total revenue coming from groceries. In terms of e-commerce in 2024, the grocery revenue in the US was $58.9 billion, which is the dominant portion (74%) of the total US e-commerce revenue for the same period – $79.3 billion.

Amazon’s grocery e-commerce revenue for 2024 is lower, around $40 billion, implying that Walmart still dominates this product segment. In fact, Amazon has put a significant amount of effort into this business for many years, but at this stage it seems improbable for them to take over Walmart due to the following reasons:

- Amazon has a strong track record with various types of products, but they don’t have the expertise and capabilities when it comes to groceries products due to their perishable nature which makes the storage and inventory management much more complex

- Amazon’s fulfillment centers cannot compete with the Walmart supermarkets. The supermarket business provides the Walmart e-commerce operations with ready-to-use fulfillment centers with all the needed functionalities for storage and inventory management

- Amazon does not have the same level of mind share as Walmart when it comes to groceries. Grocery shopping is quite habitual and hard to change, as consumers usually stick to one grocery provider. Thus, it will be very challenging for Amazon to take customers from Walmart

- Walmart prices are still lower than Amazon

- Last but not least, Amazon prioritizes cloud business, data center and AI, as that is the main destination of their huge capex spending, thus not leaving too much leeway of them investing in grocery facilities

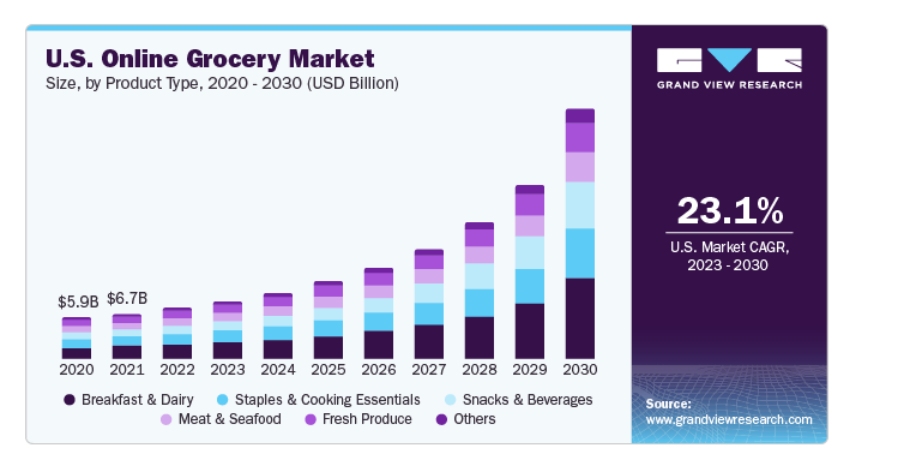

Secondly, the secular opportunity for the grocery e-commerce business is big. The penetration of e-commerce of the total grocery market is relatively small, around mid-teen digits percent. This implies the CAGR to be quite high - above 20% expected.

Source: grandviewresearch.com

To sum up, the competitive moat combined with the high secular growth will be the main engine of Walmart’s business for years to come.

Any Danger from the Peers?

Understandably, other supermarket chains like Costco and Kroger are trying to replicate the same business model as Walmart by developing their own e-commerce businesses.

Source: Scott Moses/Solomon Partners, "U.S. Grocery: A Few Things You Might Not Know" report

Walmart has certain advantages against supermarket peers:

- Size matters: With the biggest market share, WMT revenue is greater than the following three players by size (Kroger, Costco, Albertsons) all together. The large size enables Walmart to negotiate better deals with suppliers. Cheaper products imply better unit economics for e-commerce which is a big advantage compared with other e-commerce platforms.

- Solid network: Walmart is also leading decisively in number of stores, which enables them to optimize the delivery time. The strong fulfillment network allows Walmart to achieve same-day delivery to over 90% of the US households.

- First-mover advantage: While nearly 20% of Walmart’s total revenue comes from e-commerce, the percentage is lower for other industry players (Kroger – 9%, Costco – 7%, Albertson’s – 8%). By being a more e-commerce-native, Walmart can adjust its business operations towards e-commerce in a more efficient way than the rest of the large supermarket chains.

Other Walmart Initiatives Supporting the Main Business

With e-commerce as its core, Walmart is trying to build an ecosystem with several other pieces:

- Advertising and Media: Walmart Connect, the company’s advertising platform reported 31% growth year-over-year for 26Q1 and the estimated revenue from advertising for FY2025 has been around $6 billion. The acquisition of Vizio (a smart TV seller) is an entry point for further expanding the WMT advertising revenue and diving into the entertainment industry.

- Subscription: Subscription is an integral part of Walmart’s strategy to provide goods at competitive prices. Walmart+ (the company’s subscription-based membership program) has double-digit increase in income for 2026Q1.

- Third Party Fulfilling: Walmart Fulfillment Services (WFS) supports third-party sellers on Walmart's marketplace by handling storage, packing, shipping, and returns, and nearly half of Walmart’s marketplace sellers used WFS in fiscal 2025. In 2026Q1 third-party GMV growth continues to be at 20%, as more third-party retailers choose Walmart e-commerce ecosystem instead of Amazon’s. With more third parties on the Walmart platform, WFS can provide fulfillment services for them, providing an extra revenue source.

Valuation

Currently the forward 2026E PE ratio of Walmart is around 37-38x. For many investors, this may not seem very attractive, especially if we consider the macro and tariff headwinds affecting the EPS growth in the near term.

However, the company deserves a higher multiple due to the following reasons:

- Limited business downside: Will not see a revenue drop even in economic downturns

- Strong competitive moat in groceries, very hard for Amazon to compete

- Fast-growing e-commerce business combined with early stage of online penetration in groceries

- Fast-growing advertising, subscription and fulfillment businesses supporting the e-commerce business

We believe Walmart multiple should be higher, as Amazon average PE back in the 2010s, when the e-commerce business was rapidly growing, was around 60x. Of course, 60x is generous for WMT as the e-commerce is still a small portion of the total business and the grocery product mix implies a lower profit margin compared with the other e-commerce peers in the long run. But 45x seems perfectly reasonable, implying a share price of $117 (+20% upside).

Risks

The risks related to Walmart can be summarized into short-term and long-term ones.

The short-term ones are mostly related to macro factors – the slowdown in consumer spending and the tariffs. Walmart has to navigate the expectations from consumers and the government demanding lower product prices, as well as navigating the expectations of the suppliers by not squeezing their profit too much.

On the long-run, competition from Amazon remains a risk, as Amazon is still investing heavily. Also, investments from Walmart side may also pose certain risk by not justifying the ROI.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.