NOV: Undervalued, Overlooked, and Cash-Rich

- NOV trades at a forward EV/EBIT of 8.83x, about 21% below peer median, and at 0.71x EV/Sales, signaling deep structural undervaluation.

- With a P/FCF of just 3.18, NOV delivers a 19% FCF yield, far exceeding sector averages, despite minimal CapEx requirements of ~3.5% of sales.

- NOV’s asset-light, high-margin services model and integrated digital tools drive EBITDA-to-cash conversion, enhancing stability amid volatile rig cycles.

- At $12.84, NOV’s implied fair value ranges between $15.60–$17.10/share, offering potential upside of 21–33% without growth assumptions.

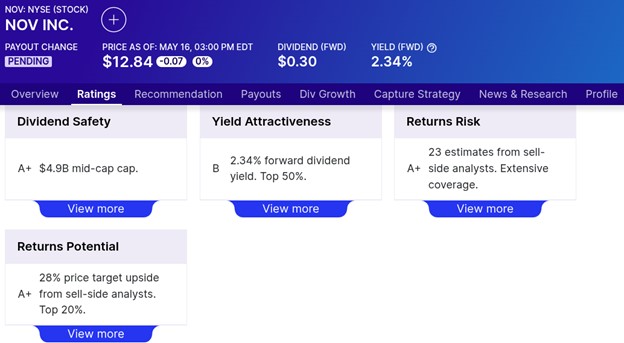

TradingKey - NOV Inc. (NOV) exists in an interesting paradox: trading at multi-year discounted valuation multiples, it generates free cash flow consistency along with operating leverage indicative of a company set to re-rate in the long run. At $12.84 a share, NOV trades at a forward EV/EBIT multiple of only 8.83x and an EV/sales ratio below 1x, a marked discount to its cyclical industrial peers. The market, however, seems to underprice NOV more akin to a cyclical, margin-sensitive commodities player rather than a structurally repositioned energy and industrial enabler with inherent leverage to infrastructure, decarbonization, and digitalization trends.

There exists a transformation beneath the surface. NOV's post-pandemic realignment focuses on capital efficiency, recurring revenue streams through aftermarket and digital services, and leaner operations that have materially improved its EBITDA-to-cash conversion. Yet, said inflection isn’t yet priced in, particularly as investor attention still tightly centers on dividend yield (now at 2.34%) as well as traditional oilfield cyclicality. With normalized earning power enhancing, a rerating opportunity can potentially arise as NOV aligns its free cash flow story with secular infrastructure capex cycles as well as digital oilfield adoption.

Source: Dividend.com

Operational Flywheel: Transition from Drilling Origins to Online Services

NOV's business model centers upon three main segments, namely, Rig Technologies, Wellbore Technologies, and Completion & Production Solutions. Historically considered a capital equipment provider to the oil & gas industry, NOV reshaped its operational framework to generate a greater proportion of revenue from aftermarket, digital, and modular production technologies, particularly in offshore, renewables, and LNG-supportive applications.

What distinguishes NOV is vertical integration as well as a modular product set. NOV holds intellectual property along the entire rig supply chain, drilling gear, pipe handling systems, blowout preventers, as well as more and more software-based automation solutions. This systems-level competence not only underlies pricing power in bespoke deployments but also creates a profitable aftermarket services flywheel as more rigs run NOV hardware, recurring maintenance, spares, and upgrade sales become sticky revenue anchors. Essentially, this transforms NOV's revenue mix from boom-and-bust CapEx orders to a mix of high-margin services, smoothing out earnings volatility as well as increasing long-term clarity.

Besides, NOV's remote diagnostics and drilling automation, which are branded as NOVOS and eVolve, are increasingly in demand. The technologies enable closed-loop control systems, which lower downtime, ensure increased safety, and maximize operational efficiency for E&Ps. This positions NOV as a key enabler for digitalizing upstream operations, aligning it to AI as well as edge computing trends in industrial infrastructure.

The key point from this paragraph is that NOV is quietly transitioning a historically hardware-heavy business into a high-margin, technology-enabled industrial platform.

Source: Q1-Deck

Competitive Landscape: Underappreciated Optionality in a Packed Competitive Field

NOV operates in a more competitive industrial environment with exposure to diversified capital goods companies like TechnipFMC and Siemens Energy, as well as traditional oilfield service companies like Schlumberger and Baker Hughes. Although bigger peers diversified into wider energy markets first, NOV still holds defensible moats as a result of its deep OEM integration as well as specialized rig systems, which prove hard to replace.

Notably, while Schlumberger and Halliburton are investing heavily in reservoir modeling with AI and cloud-based solutions, NOV's moat exists in the physical plane, particularly in field operations at the data systems interface. NOV's unique strength in integrating analytics into hardware (as compared to attaching them retrospectively) provides it a competitive advantage in retrofit applications as well as low-infrastructure regions like Africa, Latin America, and offshore Asia.

However, regardless of this ecosystem lock-in, the market seems to be valuing NOV at a structural discount to its innovation-adjusted peers. For example, NOV trades at 0.71x EV/Sales and 4.47x EV/EBITDA (TTM), while sector medians stand at 1.88x and 6.29x, respectively. Even omitting technology-heavy comparisons and considering only capital equipment peers, NOV's EV/EBIT of 8.83x remains 21% lower than the median. This indicates investors are discounting to account for sustainability in its cash flows, despite margin normalizing trends as well as growth in services revenue.

The key point here is that NOV's built-in IP and hardware-data integration are significantly undervalued relative to superior-branded digital energy equivalents.

Source: Ycharts

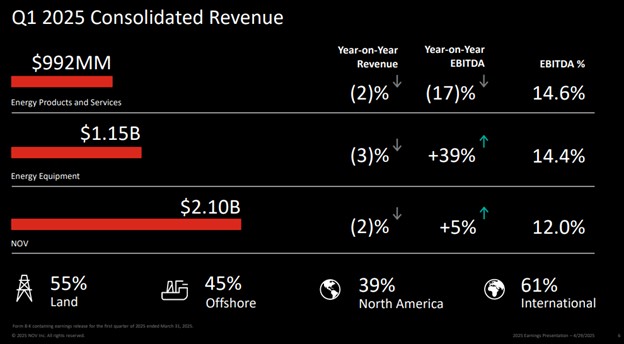

Operating & Finance Deep Dive: An Industrial Cash Machine

From a financial performance point of view, NOV's most recent trailing metrics show a disciplined cost base and efficient capital usage. While its P/E (GAAP) ratio (TTM) of 8.58, some 33% lower than its sector average, tells only part of the story, the more telling tale is in its cash generation: NOV's price-to-cash flow (TTM) ratio of a mere 3.18 indicates strong free cash flow in comparison to price.

The firm also reported an EV/EBIT (TTM) of 6.17, significantly lower than the median for its group at 11.15, which can imply that NOV continues to be seen by the market as a lag-cycle industrial reliant upon upstream CapEx. Yet NOV’s shifting mix of business, particularly its focus on low-fixed-cost servicing strategies, has insulated much of its earnings power from strict rig count volatility. Future EV/EBIT at a level of 8.83x further highlights earnings resiliency as visibility in its bookings increases.

Furthermore, with a forward price/book of 0.75, NOV is trading at a 47% discount to its group, even as it continues to execute asset-light service growth and only experiences low levels of CapEx requirements. Historically, the company has operated with a level of CapEx/sales of approximately 3.5%, which means it is far more agile than its heavy infrastructure counterparts. These dynamics underlie a structural margin growth thesis, particularly as pricing in the aftermarket as well as digitized solutions strengthens.

More tellingly, however, is NOV's FWD EV/Sales of 0.71, which values the entire business at less than 1x future sales, a level more often seen in structurally distressed or highly cyclical companies. But NOV's actual volatility metrics as well as its top-line cadence indicate that it's moving toward a hybrid industrial-services business with SaaS-like features in its maintenance, repair, and digital services top-line.

The big point here is that NOV is generating high cash flow and margin stability that historically gets rewarded by markets, but it's still trading as if it's a legacy cyclical.

Source: Q1-Deck

Compression of Valuations: A Multiple Mismatch With Strategic Implications

NOV's valuation picture presents a tale of dislocation. The stock's current P/E stands at 10.99, about 9% lower than its peers, and a 59.8% discount to its five-year history of 27.32x. EV/EBITDA (TTM) at 4.47x compares to its five-year average of 17.01x, a mind-boggling 73% compression. This indicates that even if NOV only reverts to mid-cycle valuation, there's considerable upside with no revenue growth assumption.

On a normalized FCF basis, NOV stands out. Investors are only paying more than 5x for future cash flows, given a trailing P/FCF of 3.18 and a forward P/FCF of 5.29, which is only 6.6% above its sector median. This suggests a forward FCF yield of nearly 19%, which, for a company with increasing margin quality as well as no overhanging debt, is a high number.

Of note, however, the dividend yield at 2.34% falls more than 50% behind its sector median. But perhaps this "D" grade is misleading: NOV maximizes reinvestment and buyback, especially as its capital expenditure base is still light and its ROIC continues to increase. That is to say, low dividends could indicate capital constraint, not a capital shortage.

Taking all valuation factors together, a reasonable target multiple for NOV based on forward EV/EBIT of 10–11x and 2025E EBIT of ~$750M implies an enterprise value of ~$7.5–$8.25B. After adjusting for ~$400M net debt, the implied equity value would sit near $7.1–$7.8B, or ~$15.60–$17.10/share, representing 21–33% upside from current levels.

The key point here is that NOV's valuation does not reflect its actual duration of earnings, efficiency in capital, and strategic optionality.

Source: SeekingAlpha

Risk Considerations: Structural versus Sentiment Headwinds

As NOV's transformation process continues to proceed, a number of risks exist that can support its valuation discount. For one, in spite of diversification strategies, the company continues to generate a large proportion of revenue from upstream drilling, exposing it to oil price volatility as well as exploration CapEx cycles. Any extended decrease in rig counts or geopolitical dislocations can stall growth trends.

Second, while digital offerings such as NOVOS offer stickiness over a period of time, monetization is still limited. The company, however, needs to establish that its software layer isn't a mere add-on but a monetization engine with scale in recurring revenue margins. Without that, comparisons to higher-multiple industrial technology peers can still only be aspirational.

Third, NOV's capital deployment stance, albeit disciplined, has yet to generate investor excitement. The low dividend payout and absence of buyback aggression can repel yield-hunting investors, provided FCF isn't prominently reinvested in high-ROI growth.

Lastly, execution risks in new markets, foreign currency volatility, and supply chain constraints (particularly in specialized components) might cause margin noise and slow down long-term normalizing. However, NOV represents a mispriced industrial transformer with undervalued optionality in digital oilfield services as well as modular infrastructure solutions.

Source: The Crude Chronicles

Conclusion

Cash-generative operations, a lean cost base, and a recurring revenue blend underlie a re-rating opportunity not yet priced into its significantly discounted multiples. With a range of $15.60-$17.10/share, NOV presents an asymmetric upside to patient investors who can see past legacy oilfield assumptions.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.