Moody's Downgrades U.S. Rating: How Could a Short-Term Event Possibly Sway the Long-Term Bull Market of U.S. Stocks?

TradingKey - Against the backdrop of elevated debt levels, large amount of interest payments, and deepening partisan divides, Moody's downgraded the U.S. sovereign credit rating from Aaa to Aa1 on 16 May 2025. Given the precedents set by S&P's downgrade in 2011 and Fitch's in 2023, financial markets have shown a desensitized response to this event. We believe the impact of this downgrade has largely dissipated. Looking ahead, with the Federal Reserve resuming its rate-cutting cycle, domestic tax reductions, and robust corporate earnings, we remain optimistic about the U.S. stock market. Additionally, U.S. Treasury prices are expected to rise, driven by their safe-haven appeal and the impact of lower policy rates.

Source: Mitrade

On 16 May 2025, Moody's downgraded the U.S. sovereign credit rating from Aaa to Aa1, while adjusting the outlook from negative to stable (Figure 1).

Figure 1: Rating Agency Downgrades

Source: Refinitiv, TradingKey

The primary reasons for Moody's downgrade of the U.S. sovereign credit rating are escalating debt levels, excessive interest payments, and deepening partisan divisions:

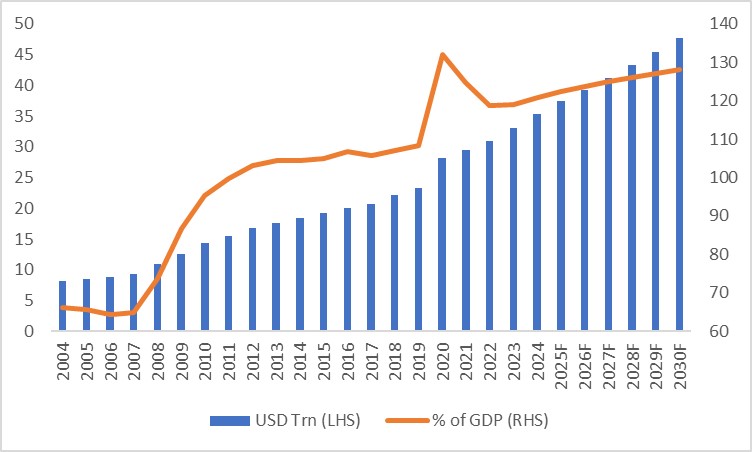

- The U.S. debt has reached an unprecedented $36 trillion (Figure 2). This, combined with $6.5 trillion in U.S. Treasuries maturing in June, places immense pressure on U.S. fiscal stability.

- Amid this massive debt, interest payments on U.S. debt in 2024 accounted for 73% of total federal expenditure. These high interest costs are crowding out other critical government spending.

- Persistent bipartisan disputes over government revenue and expenditure have hindered fundamental solutions to the U.S. fiscal challenges. Against this backdrop, the IMF projects that U.S. government gross debt will rise to 128.2% of GDP by 2030, an increase of approximately 6.5 percentage points from current levels.

Figure 2: General Government Gross Debt

Source: Refinitiv, TradingKey

Moody's downgrade decision on 16 May 2025, marks the completion of credit rating downgrades by all three major global rating agencies for the U.S. sovereign credit rating. Historically, on 5 August 2011, S&P's downgrade triggered massive sell-offs in U.S. equities, leading to sharp declines in stock prices. In contrast, after Fitch's downgrade on 2 August 2023, U.S. stocks experienced a decline, but the drop was significantly milder than in 2011. Following Moody's downgrade on 16 May 2025, U.S. markets saw a slight dip on the day. However, U.S. equities quickly rebounded thereafter. This resilience is largely attributed to the market's desensitization to such downgrades, shaped by the experiences of the prior two events.

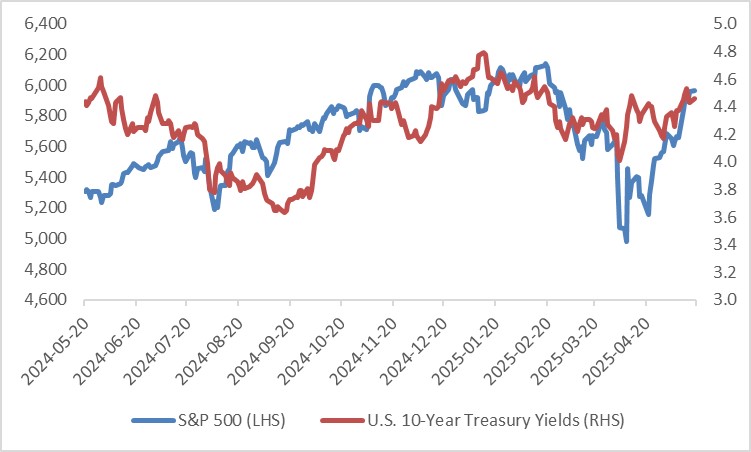

The impact of Moody's downgrade is expected to have largely dissipated. Looking ahead, we remain optimistic about U.S. equities, driven by the Federal Reserve's resumption of its rate-cutting cycle, domestic tax reductions, and strong corporate earnings. Regarding U.S. Treasuries, while some economists question their safe-haven status, we believe their foundation as a safe-haven asset remains robust. This is underpinned by the vast scale of the U.S. economy, the high liquidity and low transaction costs of the Treasury market, and the enduring confidence of global investors. A fundamental shift toward riskier assets is unlikely in the near term. If economic growth continues to slow alongside Fed rate cuts, U.S. Treasury prices are likely to resume their upward trajectory (Figure 3).

Figure 3: U.S. Stocks and Treasuries

Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.