Meta’s Big Bet: Soaring Profits, Sky-High Risks

- Meta reported Q1 2025 revenue of $42.31B, up 16% YoY, and net income surged 35%, showcasing strong growth and a boosted 41% operating margin versus 38% last year.

- CapEx reached $13.69B in Q1, nearly 32% of revenue, signaling heavy investment in AI infrastructure as total-year guidance jumps to $64–72B, up from $60–65B.

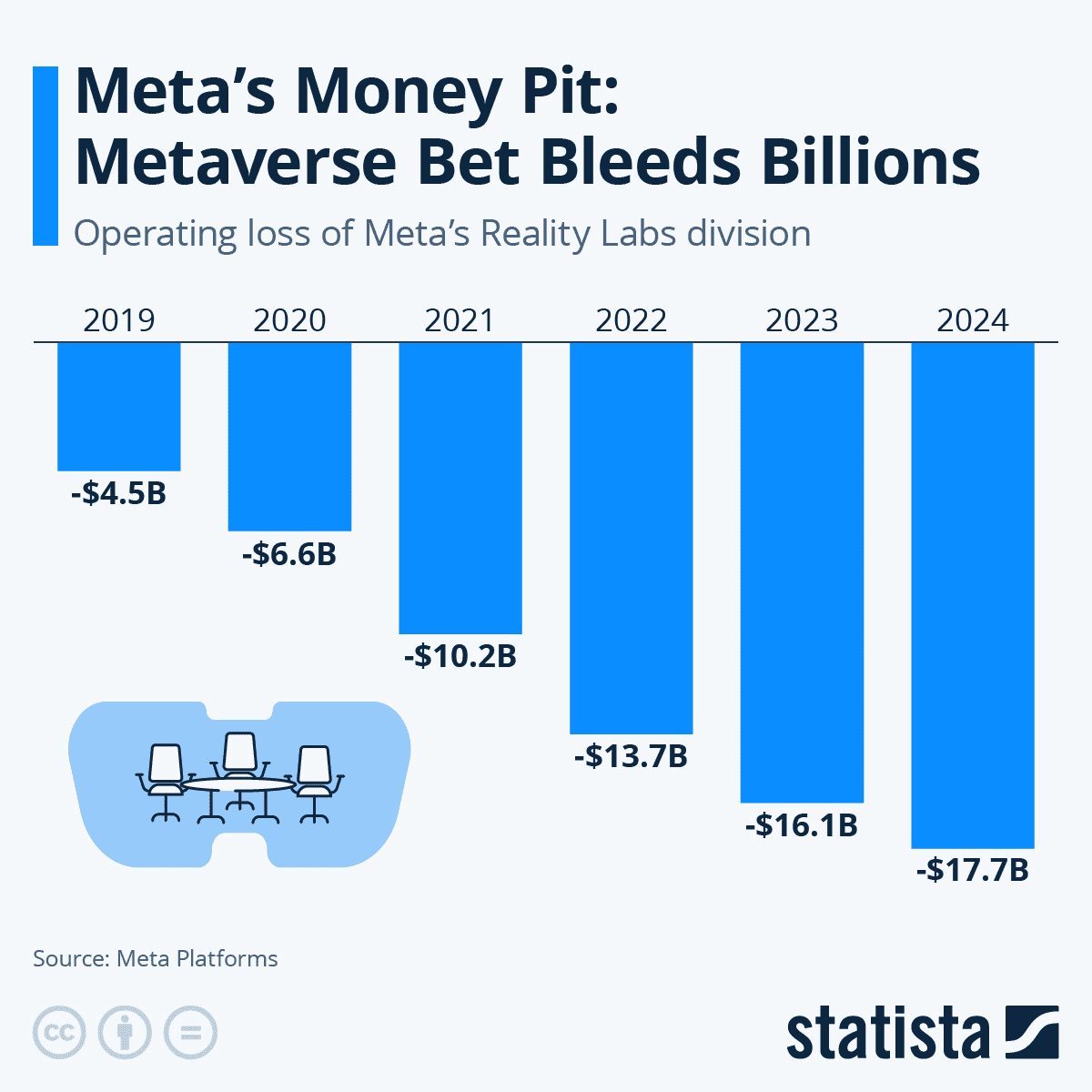

- Reality Labs continues to lose over $4.2B quarterly on $412M revenue, down YoY, with no tangible monetization despite Meta AI glasses development claims.

- Stock trades at ~23x forward earnings and 7.9x forward P/S, a ~600% sector premium, making it highly sensitive to AI execution risks and regulatory threats in Europe.

TradingKey - Meta's (META) Q1 2025 earnings come in with the world watching in scrutiny. The company has established itself as a platform that exists at the intersection of AI infrastructure, hardware innovation, and next-wave advertising. The headline figures are bullish: 16% year-over-year revenue growth to $42.31 billion, a 35% increase in net income, and an operating margin of 41%, up from 38% last year. These figures are merely the tip of the iceberg. Beneath the growth is an intensified focus on AI monetization, evidenced by its aggressive $13.69 billion in CapEx and the scaling of Meta AI to nearly one billion users.

This inflection point is what investors need to decipher. Is Meta investing in advance of the curve in a winner-takes-all AI platform game, or do we witness unsustainable capital expenditures with unproven monetization? While ad pricing increased by 10% and volumes merely by 5%, the disconnect from decelerating impression growth and flattish ARPP (average revenue per person) hints that Meta’s monetization runway is in danger of becoming front-loaded. And while all this is transpiring, Zuckerberg’s aggressive bets on AI glasses and LLM-based user interfaces suggest a strategic shift that is not adequately de-risked. With Reality Labs continuing to report quarterly losses of more than $4.2 billion, investors are rightfully skeptical whether Meta’s current operating leverage will survive execution risks in unproven hardware segments.

Meta's path is, in the end, a big-bet strategy: that it will be able to capture value from an AI platform environment before regulators, competition, and users' trust cause its margins to decline. The figures are dazzling, but the question is whether or not Meta will be able to ride this wave without risking overextension.

Source: Meta AI app

Platform Gravity: The New Meta Engine

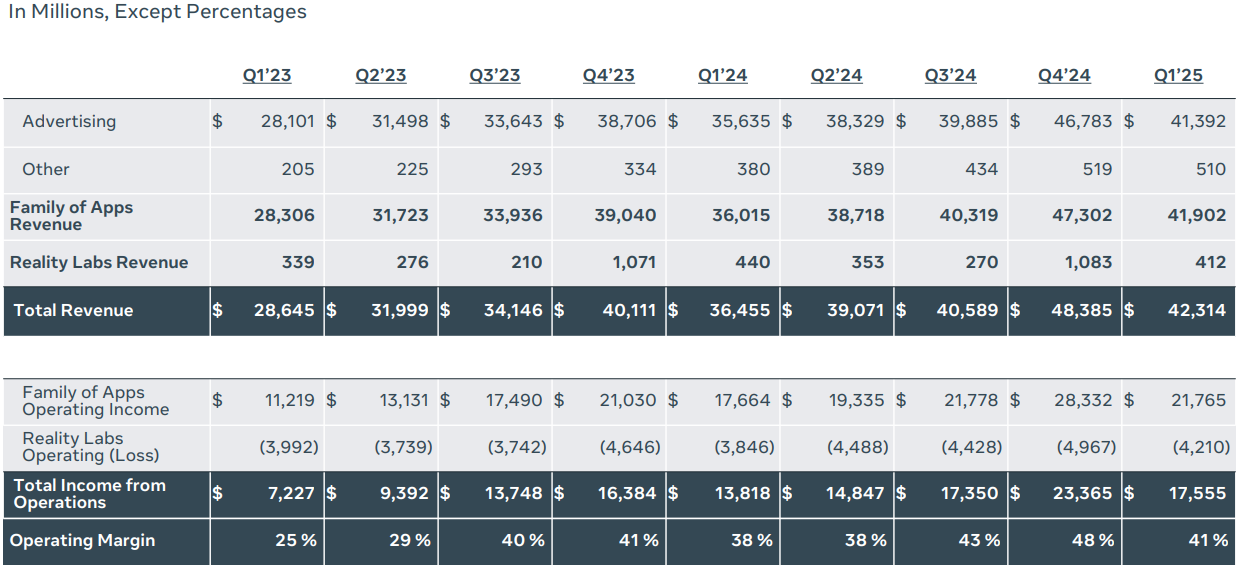

The foundation of Meta's financial performance is the Family of Apps (FoA) segment, driving $41.9 billion in Q1 revenue, up by 16% year-over-year, and producing $21.77 billion in operating income, representing a strong 52% segment margin. FoA is the undisputed cash engine, with Facebook, Instagram, Messenger, and WhatsApp all holding strong on global users' engagement. Meta has 3.43 billion daily active people (DAP) and continues to have unmatched reach, up 6% YoY. Engagement is no longer the narrative, though, monetization efficiency per user is what counts.

While average ad pricing YoY growth (+10%) balanced off what was otherwise a sluggish 5% impression growth, geographic segmentation shows cracks. Europe, accounting for ~22% of revenues, is under threat from the EU's DMA ruling, risking Q3 monetization with the potential for "materially worse" user experiences and ad opt-outs. Subscription-for-no-ads is not likely to replace these lost revenues. Meanwhile, North America, including the saturation that exists there, continues to deliver double-digit ARPP and price-per-ad expansion, demonstrating that Meta's pricing power is unbroken in its most valuable market.

Reality Labs (RL) continues bleeding with a loss of $4.2 billion on revenue of only $412 million, down from last year's $440 million. Even though Mark Zuckerberg stated that Meta AI glasses are advancing, the business thesis is still speculative. The overall thesis is that RL will be the AI-interaction interface layer, but no tangible monetizing has materialized. We will not reduce its earnings drag as long as it fails to break even or show commercial adoption by anyone other than early adopters.

Ultimately, Meta's growth driver remains FoA, with the compounding impact of personalized delivery of ads, audience size, and continuous AI refinement of ad ranking driving monetization resilience. Investors need to be careful not to over-lean on RL's optionality without evidence of real monetization.

Source: Meta Q1 2025

A Changing Battlefield: Infrastructure, AI, and Competitive Tensions

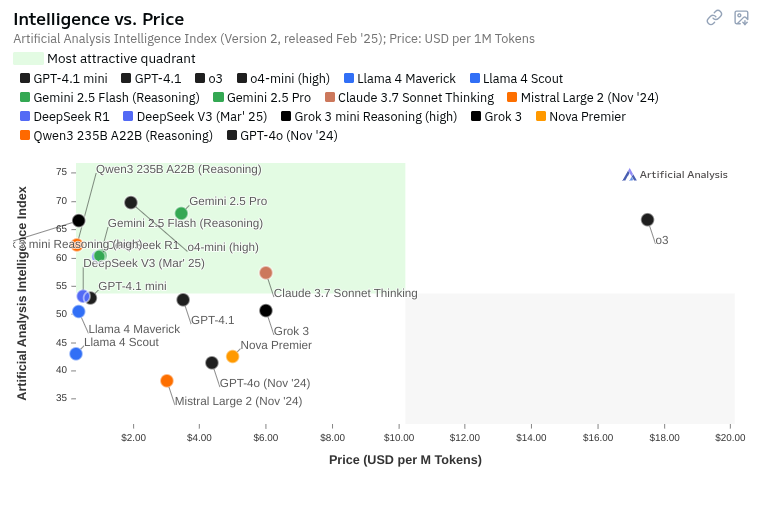

Meta's most impactful pivot is not a product, it's the infrastructure. With total-year CapEx now predicted to hit $64–72 billion, up from earlier guidance of $60–65 billion, the firm is doubling down on developing its hyperscale AI data centers. The thesis is straightforward: owning the end-to-end AI stack from LLMs (Meta AI) to inference endpoints (glasses, Ray-Ban Meta, Portal) to underlying computers (custom silicon, Meta Training & Inference Accelerator) allows control and efficiency. But the size is astounding, Q1 CapEx alone hit $13.69 billion, almost 32% of revenue.

The reason behind it? Meta AI, with almost 1 billion active users every month, is increasingly integrated into WhatsApp, Messenger, Instagram, and Ray-Ban products. It is not yet another assistant, it’s Meta's attempt at a pervasive agent-based interface to all digital engagement. CEO remarks indicate Llama 3 is getting training across Meta's platform and will be rolled out in open-weight mode, probably to control the ecosystem through de facto standards.

This puts Meta squarely in competition with OpenAI, Google DeepMind, and Anthropic, all of whom enjoy more robust institutional pipelines of deployment. Meta's open-source orientation is also two-sided. While driving adoption and visibility, it lowers price power. Meta's ad-centric monetization of AI is so far, whereas Microsoft Azure integrations or Google Search integrations have more ROI visibility.

On the consumer side, Meta's vertical integration has a longer-term margin upside. Custom silicon and self-hosted infrastructure will lower dependence on Amazon and Nvidia, particularly as inference price keeps coming down. But in the short term, it inflates fixed expenses and squeezes free cash flow. Q1 free cash flow dipped to $10.3 billion from $12.5 billion YoY, even as operating income hit record heights. That is the trade: speed and control vs. short-term cash restraint.

Meta is certainly laying the tracks for the digital economy of the future, but it is uncertain if its infrastructure goals are commercially viable, particularly if customer lock-in is not as defined as in AWS or Azure's B2B cases

Source: Artificial Analysis

Valuation Checkpoint: Is Premium Justified or AI Inflation?

At ~$597 per share, Meta is now trading at a premium compared with the rest of the tech industry, and the valuation picture has significantly changed in Q1 2025. Even with strong earnings and sustained operating leverage, the forward valuation of the stock shows elevated investor expectations that are susceptible to even slight slippage in execution.

Meta is trading at around 22.88x forward GAAP earnings and ~23x forward non-GAAP earnings, a ~28% and ~84% premium to respective sector medians, respectively. These multiples are marginally lower than Meta’s 5-year averages of ~23.5x–25.9x, indicating that the market has not yet completely normalized off the back of AI excitement. On a PEG basis, the view is more neutral: the forward PEG is around 1.32x by sector conventions but down ~15% from Meta’s average (1.55x), indicating that near-term growth is increasingly baked in.

Yet, valuation pressures are compounded if one looks through the lens of revenue. Meta’s ~7.8x forward EV/sales is more than 4x the sector median and significantly above its 5-year history. Likewise, its ~7.9x forward price/sales multiple is a 600%+ premium to the sector. This may be partially explained by Meta’s high-margin, ad-driven business, but it also leaves the stock vulnerable to downside if growth slows or if regulatory resistance becomes more of a problem, especially in Europe.

EV/EBITDA forward is ~13.1x, and EV/EBIT is ~19.9x, both significantly above industry means, though in line with Meta’s historical standards. The premium in value comes across most dramatically in measures of capital efficiency: Price-to-Book is approximately 6.5x, nearly three times the industry median, and Price-to-Cash Flow is ~14.7x, once more almost twice that of peer companies.

In short, Meta is no longer the misjudged compounder trading at a discount. The market is already giving it nearly monopoly AI value, with most monetizable vectors, particularly AI infrastructure and intelligent devices, yet untested. With perfect execution of AI platform unification and LLM interface monetization, the value may hold. A mistake, though, in Europe or Reality Labs, with so much growth already priced in, will compress multiples aggressively.

Source: Precedence Research

The Risk Architecture: Regulatory Icebergs and CapEx Gravity

Despite the euphoria, there are several structural threats to Meta's path. Most immediate is the one of regulation: the EU's Digital Markets Act judgment against Meta's ad-subscription model will provoke alterations that can materially blunt European ARPU beginning in Q3. Management is cautioning of a "material" downgrade in the user experience that will cause both user attrition and ad revenue loss. Unlike Apple's privacy modifications, which Meta weathered in the long run, the DMA may structurally reset its monetization model in Europe, its high-margin region.

Second, CapEx discipline is under question. While long-term AI superiority may warrant infrastructure spending, the magnitude and up-front spending create operating leverage vulnerability. Without AI monetization, particularly through Meta AI and smart glasses, keeping pace with expectations, Meta's fixed cost foundation could be a drag instead of a moat.

Third, the Reality Labs narrative is not compelling. With revenue falling and quarterly losses tallying more than $4 billion, the segment is increasingly looking like a costly experiment instead of a growth driver. Investors need to remain cautious until there is proof of unit economics or mass consumer uptake. Finally, macro sensitivity, particularly to advertising spend of consumers, is still a structural risk. Meta’s ad business, algorithmic sophistication notwithstanding, is subject to cyclical economic trends. Q1 resilience notwithstanding, it is possible that if global ad spending declines, Meta’s single-source revenue sensitivity will be revealed.

Meta's Q1 2025 results confirm its supremacy but show the price of its ambition. The firm is shifting from the pure ad monetization machine to a vertically integrated platform of AI, making aggressive bets on infrastructure, hardware, and user interfaces. The early returns are impressive but not definitive. For institutional investors, the potential is in asymmetric optionality: if Meta successfully capitalizes on its AI stack, the rerating of the valuation will be significant. But if execution fails, the premium in the stock may turn out to be unsustainable.

Source: Statista

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.