What Markets Are Missing About JPMorgan

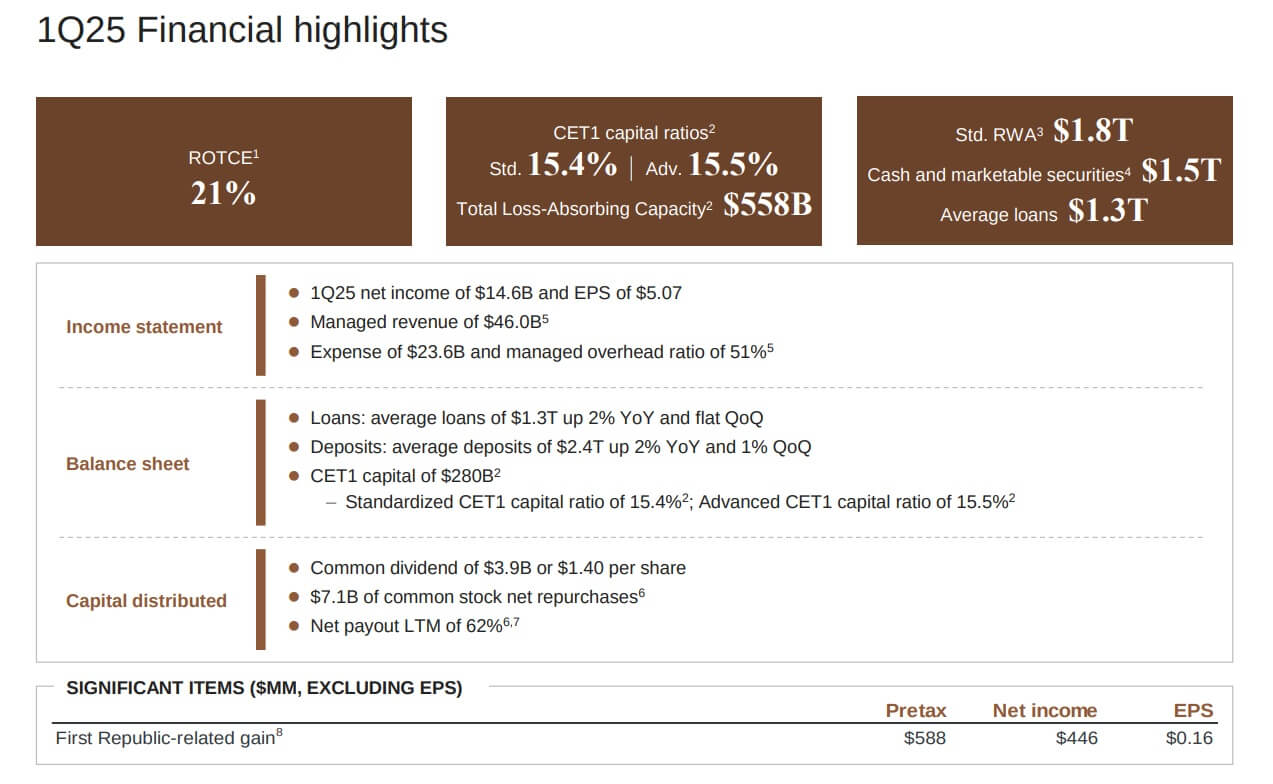

- JPMorgan reported Q1 2025 net income of $14.6 billion with a 21% ROTCE, supported by strong fee growth.

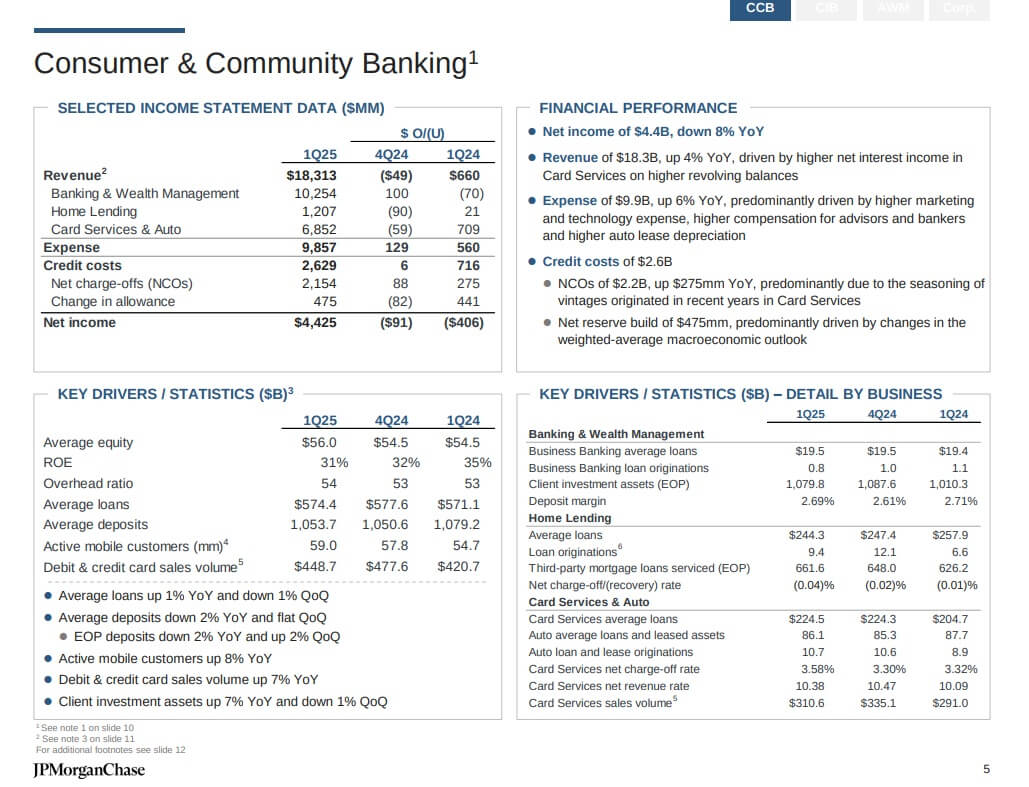

- Consumer banking showed resilience with $4.4 billion net income, but card net charge-offs rose to 3.58%.

- CIB delivered $6.9 billion net income with 12% revenue growth, while Markets revenue surged 21% to $9.7 billion.

- Tangible book value grew 13% YoY to $100.36, with CET1 capital ratio stable at 15.4% and $1.5 trillion liquidity.

TradingKey - Amidst an age of increasing geopolitical uncertainty, inflationary frictions, and regulatory change, JPMorgan Chase (JPM) is notable not for size alone but for the choreography of scope, balance sheet strength, and diversified revenues. Even in market turmoil, the bank reported Q1 2025 net income of $14.6 billion with a return on tangible common equity of 21% supported by high quality of earnings, good cost discipline, and healthy client traction across segments.

However, below the radar lies nascent cracks in deposit growth, cycle credit pressures, and margin squeeze that suggest a more complex investment thesis. Even as consensus views JPMorgan as a bellwether of stability, a more detailed dissection yields an asymmetric composition of reliable earnings and hidden vulnerability, particularly with the existing "wait-and-see" macro environment spilling over in a stagflationary scenario.

With markets too reactive to sentiment and interest rate whiplash, JPMorgan's present valuation at ~1.7x tangible book and ~9.5x forward earnings seems to be based upon a lasting premium story. But in our view, such premium is increasingly dependent upon high-quality capital-light fee earnings and the bank's ability to navigate through a change in credit cycle. The investment case is less about accelerating growth and more about being strategically insulated. The test for JPMorgan is to take its fortress model to greater heights through digitization, AI infrastructure, and operational leverage without sacrificing its margin of safety.

Source: Q1 Deck

Integrated Scale, Diverse Engines: A Fortified Business Model

Three pillars form the business model of JPMorgan: their breadth in consumer and commercial banking, investment and trading supremacy, and fast-growing asset and wealth management franchise. They all add to their strategically diversified earnings base, it insulates the company from cyclical risks in one segment and allows for adaptive deployment of capital.

In Q1 of 2025, Consumer & Community Banking (CCB) registered net income of $4.4 billion, with solid card revenue (+12% YoY) compensating for deposit NII softness from margin compression. Card Services net interest income improved with 10% YoY revolving balance growth and healthy volume sales, with Auto originations growing 20% YoY. The net charge-off ratio did, however, increase to 3.58%, which points to growing evidence of credit deterioration in newer vintages, a cyclical risk that needs to be tracked closely.

Commercial & Investment Banking (CIB), JPM's crown jewel, had net income of $6.9 billion with revenue rising by 12% YoY to $19.7 billion. The bank sustained its #1 ranking in investment banking fees globally (9% wallet share), with Advisory increasing by 16% and Debt Underwriting by 16%, covering part of the thaw in corporates’ deal-making. Markets revenue increased by 21% to $9.7 billion, with record Equities performance of +48% fueled by derivatives activity in a volatile environment. Most significantly, average client deposits in CIB increased by 11% YoY, supporting JPM's defensive funding position in an environment of private credit disintermediation.

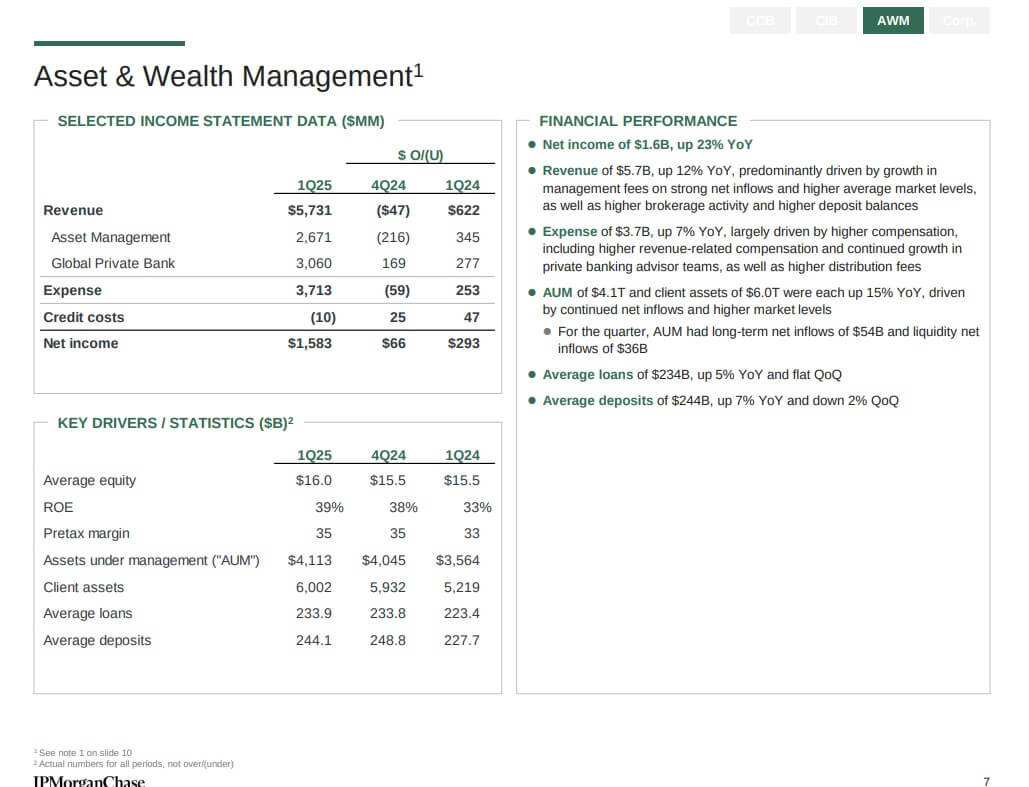

The Asset & Wealth Management (AWM) segment maintained its under-the-radar climb, generating $1.6 billion in net income on $5.7 billion of revenue (+12% YoY). Assets under management increased to $4.1 trillion (+15% YoY) based upon $54 billion in long-term net inflows. Highlighting AWM's long-term shift to scalable, capital-light growth drivers, the segment registered record-high segmental ROE (39%) and pretax margin of 35%.

Its ability to capitalize on technology spend, client insight, and platform integration is common among all three divisions. Through embedded wealth onboarding in Consumer & Community Banking, through to AI-driven analytics in Equities and Foreign Exchange trading, the bank's ecosystem strategy multiplies advantage over time.

Source: Q1 Deck

Getting Ahead in the Crowd: Managing in an Ever-Changing Competitive Marketplace

Its leadership position is also taken for granted, but is both qualitatively and quantitatively ahead of competitors. Its ~15.4% CET1, $1.5 trillion of liquidity, and $280 billion of capital offer powerful downside protection. But there is also formidable competitive moat embedded in its operational DNA: real-time treasury infrastructure, superior distribution, and investment banking/trading pricing power.

Meanwhile, disintermediation risks are building. Private equity players, along with non-bank lenders, continue to push inroads in structured credit and middle-market lending, particularly in the context of regulatory tightening since Basel III. JPMorgan's dedication to "product agnosticism", either syndicating standard loans or arranging private placement, is timely in the face of changing credit environments. Nevertheless, the firm's book of wholesale loans diminished marginally QoQ, with lending revenue increasingly resting upon hedging gains rather than organic loan expansion, indicative of competition.

In asset and wealth management, JPMorgan is challenged by fee-compressing passive platforms and digital-first competitors. But it holds an advantage in advisor size, cross-channel connectivity, and capacity to capture lifetime value through multi-generational wealth strategies. The fact that AWM deposits increased by 7% YoY in the face of rate headwinds supports client stickiness, a differentiator in turbulent markets.

In investment banking, JPMorgan still maintains market share leadership, but there is higher execution risk. Market uncertainty has pushed pipeline conversion to later, and equity underwriting is soft (-9% YoY) due to investor caution. Debt markets, however, are rebounding more quickly to the advantage of JPMorgan's leveraged finance business. Fee growth in the subsequent two quarters will depend on macro certainty and confidence in corporations, both of which are still in flux.

Source: Q1 Deck

Resilience Engineered: Drivers of Growth and Financial Structure

JPMorgan Q1 2025 earnings reflect a fine balance of secular tails versus cyclical prudence. Firm-wide revenues increased by 8% YoY to $46.0 billion, with noninterest revenue (+17%) growing more than net interest income (+1%). NII less Markets was $22.6 billion, down by 2% YoY, due to deposit compression in CCB which was partially offset by healthy growth in cards and wholesale deposits. Markets revenue of $9.7 billion, notably Equities, was the swing factor behind revenue beats.

On the expense front, costs increased by 4% to $23.6 billion, fueled by increased compensation (attributed to front-office recruitment and incentive compensation), technology expenditure, and legal/brokerage charges. The adjusted overhead ratio increased marginally to 51%, and the company restated FY25 adjusted expense guidance at ~$95 billion, with no sign of structural cost blowout. Notably, technology spend is not being cut-back, implying a long-game strategy for AI infrastructure and cybersecurity, even in periods of volatility.

Credit expenses amounted to $3.3 billion, with net charge-offs of $2.3 billion and a net build in reserves of $973 million-principally as a result of an increased assumption of 5.8% unemployment in JPM's CECL models. Most significantly, there was no sign of material credit deterioration, which would indicate defensive provisioning in place of reactive tightening.

Capital return was robust: $7.1 billion in share repurchases and an increased dividend of 12% to $1.40 per share, equating to a 62% net payout in the previous 12 months. Tangible book value increased to $100.36 (+13% YoY) supporting JPM's shareholder wealth compounding engine. CET1 was also in good shape at 15.4%, with $558 billion of total loss-absorbing capacity as well as $1.5 trillion of HQLA, plenty to ride out liquidity shocks.

JPMorgan's guidance for 2025 is also intact: NII of ~$94.5 billion (unchanged YoY), NII ex-Markets of ~$90 billion, and an estimated Card charge-off rate of ~3.6%. The former two are indicative of moderate topline growth with a defensive earnings composition in keeping with its fortress culture.

An Anchored Valuation Based on Quality, Not Yield Alone

On initial view, JPMorgan’s valuation appears reasonable for a bank of its stature, but scratch a little deeper, and fissures appear. Trading at a forward P/E of 13.32, JPM trades 29% above the sector median, and its 2.05 price-to-book multiple is an alarming 76% above. Investors are obviously paying a premium for fortress-balance-sheet security and a robust ROTCE, but relative to that of its five-year historical norm, the premium is more contained, forward P/E stands only 8.5% above its historical anchor. In short, the market is paying for consistency, not explosive expansion, and expecting that JPM’s earnings engine will continue firing even in rougher seas.

But valuation risks are gathering below the surface. JPM’s PEG ratio for the future is now 3.70, more than triple the sector median, indicating an increasing disconnect between realistic growth and price. Forward and trailing price-to-sales multiples (3.86 and 4.13, respectively) are also higher than peers by nearly 50%, and since fee growth moderates, these multiples can compress easily.

The dividend yield of 2.06% also lingers well below the 3.24% sector median, which doesn’t leave much cushion if sentiment turns. Plainly speaking, JPMorgan’s premium valuation is riding on perfect execution and a benign macro environment. Any misstep, be it creeping credit losses, margin compression, or regulatory drag, can precipitate a sharp re-rating. It’s an excellent name, to be sure, but at these prices, you’re not being offered much margin of safety.

Risk Radar: Macro, Regulation, and Rate Sensitivity

Although JPMorgan's fundamentals are good, various risks justify investor caution: First, macro turbulence is an increasing wild card. CEO Jamie Dimon described a 50/50 recession risk, and front-loading consumer expenditure before tariffs might conceal weakness in demand. Delinquencies in cards are increasing, though from very low bases, and deposit margin compression might continue if rate reductions are delayed.

Second, regulation is still an unknown variable. Capital reform, SLR adjustments, and CCAR results might change capital return flexibility. JPM's excess capital of $30–60 billion is strategic in nature, but subsequent buffers might be pushed higher based upon regulatory recalibration.

Third, valuation premium depends on perceived quality. Breaks in credit or conversion in M&A would reset expectations. The firm's investments in AI are promising but unquantifiable in near-term earnings, so they are a longer-run optionality bet rather than a catalyst.

Conclusion

JPMorgan's Q1 2025 results solidify its status as structurally strongest U.S. bank. With diversified profitability, risk discipline, and liquidity fortress, it is well-placed to be resilient. However, under calm exterior are frictions between fee-driven growth and margin compression, reinvestment in technology and macro uncertainty, premium valuation and cyclical vulnerability. In a world where markets are bifurcating, JPMorgan's is an unusual mix of quality with size, but investors need to set expectations for compounding over time, and not explosive upside.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.