Asian Equity Opportunities in 2026: Comparing Korea, Taiwan and Japan

AI Podcast

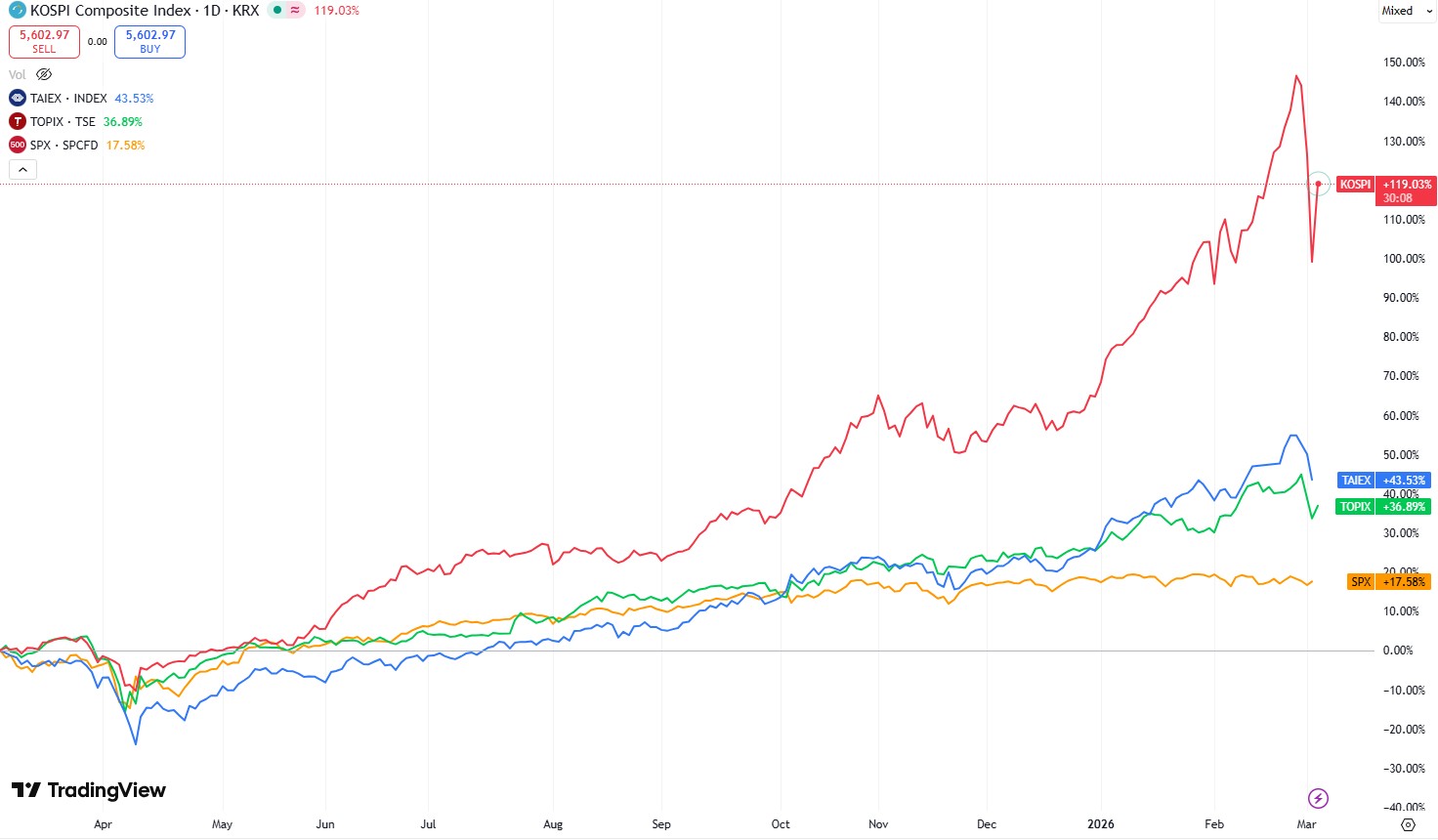

The KOSPI has surged 118% in 12 months, driven by capital market reforms and the AI boom, not economic growth. Reforms address chaebol governance, boosting minority shareholder rights and dividends. AI demand fuels significant gains in chipmakers Samsung and SK Hynix, which dominate the index, creating high concentration risk. MSCI reclassification and tax reforms are potential future catalysts. Taiwan's TAIEX, up 50%, is heavily reliant on TSMC, offering limited diversification. Japan's TOPIX, up 42%, benefits from governance improvements and household cash flowing into equities, with less concentration risk and attractive valuations.

Korea

Source: TradingView

Up until the Iran-related shock, the Korea Composite Stock Price Index (KOSPI), the primary benchmark for South Korea's stock market, has experienced one of the most remarkable rallies in recent financial history.

Over the past 12 months, the index has surged by an impressive 118%, marking a historic bull run that surpasses even the substantial 80% increase seen in gold prices during the same period. This extraordinary performance stands out because it has not been fueled by traditional monetary easing, such as significant interest rate cuts—the most recent reduction occurred in May 2025—nor by robust economic growth, as South Korea's economy expanded by only about 1% throughout 2025.

The rally's primary drivers stem from two key factors: sweeping capital market reforms introduced by the government and the global boom in artificial intelligence (AI). Historically, Korean stocks carried a poor reputation among international investors due to structural issues tied to the dominance of chaebols—massive, family-controlled conglomerates like Samsung, Hyundai, and LG that span multiple industries. These entities often prioritized the interests of controlling families over minority shareholders, leading to governance concerns, suppressed valuations, and limited upside for outside investors.

To address these longstanding problems, the Korean government implemented several transformative measures. Companies are now required to mandatorily cancel treasury shares within one year of repurchase, a practice that boosts earnings per share and enhances voting power for minority shareholders by reducing outstanding shares.

The dividend tax rate was reduced from 50% to 30%, making payouts more attractive. Stronger legal protections now allow minority investors to sue controlling families if their rights are violated.

Additionally, listed companies must disclose detailed "Value-Up Plans" outlining strategies to improve shareholder returns. These reforms have fundamentally shifted perceptions, encouraging greater capital allocation to equities and unlocking hidden value in the market.

Complementing these policy changes has been the explosive AI-driven demand for advanced semiconductors.

South Korea's economy is heavily oriented toward high-tech industries, and the KOSPI reflects this with significant weightings in memory chip producers. Samsung Electronics (KRX: 005930) has risen 285% over the past year, while SK Hynix (KRX: 000660) has skyrocketed 439%. Both companies dominate the memory chip market, which is critical for AI data centers, where supply remains constrained amid surging demand.

Despite these tailwinds, the KOSPI's structure introduces notable risks. Samsung and SK Hynix together account for nearly 40% of the index's total weight, creating extreme concentration—far higher than the roughly 32-35% represented by the Magnificent Seven stocks in the S&P 500. This heavy reliance on just two companies amplifies vulnerability to sector-specific downturns.

Looking ahead, several catalysts could sustain or extend the rally. A potential reclassification of South Korea from an emerging to a developed market by MSCI could trigger $20–$40 billion in passive inflows from global funds. Mandatory English-language disclosures for KOSPI companies would improve accessibility for international investors, while planned reductions in inheritance taxes could discourage controlling families from artificially suppressing share prices to minimize tax liabilities.

Valuation metrics remain deeply attractive compared to global peers:

Metric | KOSPI (South Korea) | S&P 500 (USA) | The Gap |

Forward P/E (12M) | ~9.5x | 21.5x | 12.0x (Massive Gap) |

P/B Ratio | 1.35x | 5.47x | 4.12x |

However, challenges persist. The index remains closely tied to the AI cycle, and any slowdown or "AI winter" could trigger sharp corrections. Chaebol families, though under pressure, retain significant influence and may resist further reforms. Broader structural economic issues, including sluggish domestic growth, also linger.

Taiwan

In comparison, Taiwan's TAIEX index has delivered a solid +44% return over the past 12 months—strong but less explosive than the KOSPI and well above the S&P 500's +18%. The TAIEX is overwhelmingly driven by Taiwan Semiconductor Manufacturing Company (TSMC), which comprises about 40% of the index's market capitalization.

TSMC's recent launch of mass production for 2nm chips, boasting gross margins exceeding 60%, underscores its pricing power in advanced foundry services. Other constituents, such as Hon Hai (Foxconn) as a key assembler for Nvidia's AI infrastructure and MediaTek advancing edge AI in consumer devices, provide additional AI exposure.

Yet TAIEX offers limited diversification benefits, as buying a broad index ETF essentially replicates heavy TSMC concentration while incurring management fees.

Its forward P/E of 17-20x appears less compelling than the KOSPI's deep value. Positive factors include accommodative monetary policy with 2% interest rates and low inflation, potential for further easing to support tech lending, and emerging trends like consumer hardware refreshes driven by AI or shifts toward custom silicon by major tech firms.

Japan

Japan's TOPIX index has advanced 37% in the past year, reaching all-time highs. Unlike KOSPI's blend of reforms and AI or the TAIEX's pure AI narrative, the TOPIX story centers squarely on governance improvements and stimulus.

Japanese households hold enormous cash reserves—approximately 78% of the TOPIX market cap in deposits—while corporate cash stands at around 9%. With rising wages and persistently low interest rates, these funds are increasingly flowing into equities. Regulators continue to push companies toward aggressive share buybacks and higher dividends.

Category | Amount (USD Trillion) | Amount (JPY Quadrillion) | % of TOPIX Market Cap |

Household Financial Assets | $14.70 T | ¥2.286 Q | ~160% |

— of which is Cash/Deposits | $7.20 T | ¥1.122 Q | ~78% |

Corporate Cash Reserves | $0.84 T | ¥130.0 T | ~9% |

TOPIX Total Market Cap | $9.20 T | ¥1.430 Q | 100% |

The TOPIX benefits from far lower concentration, with the top three constituents (Toyota, Sony, and MUFG) comprising only about 12% of the index. It appeals to institutional investors seeking value, low correlation to U.S. tech, and structural tailwinds.

Potential future catalysts include government stimulus packages targeting semiconductors, equivalent to 3-4% of GDP.

Comparison

From a valuation standpoint, the KOSPI appears most undervalued but carries the highest drawdown risk due to concentration and AI dependency. The TOPIX offers a superior risk-reward profile with fair valuations around 15-16x forward P/E, strong institutional interest, incoming retail flows, and policy support. The TAIEX, while benefiting from AI momentum and supportive conditions, functions largely as an AI proxy with limited diversification appeal.

For exposure, investors might consider the iShares MSCI South Korea ETF (most liquid but not a perfect KOSPI match) or the low-cost Franklin FTSE South Korea ETF (0.09% expense ratio) for Korea. For Japan, the iShares MSCI Japan ETF provides high correlation to the TOPIX. Taiwan exposure is available via the iShares MSCI Taiwan ETF, though with heavy TSMC weighting.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.