Japan’s ‘Truss Moment’ Is Here. Bond Market Slumps, Japan’s Second-Largest Bank to Double Down?

AI Podcast

Japan's Prime Minister Takaichi announced an end to fiscal austerity and a snap election, triggering a significant sell-off in Japanese Government Bonds (JGBs). JGB yields surged to multi-year highs, with 40-year yields exceeding 4% for the first time. This volatility, exacerbated by weak auction results, has drawn comparisons to the 2022 UK gilt crisis. The Bank of Japan faces a dilemma balancing inflation control and market stabilization. Despite potential risks and global spillovers, Sumitomo Mitsui Financial Group plans to significantly increase its JGB holdings once market volatility subsides.

TradingKey - Japan faced its own "Truss moment" at the start of 2026.

On January 19, Japan's new Prime Minister Sanae Takaichi announced the end of long-standing fiscal austerity policies and plans to dissolve the House of Representatives this week, calling for a snap election on February 8. This combination of political and macroeconomic policy shifts, coupled with weak JGB auction results, instantly triggered a wave of selling in the Japanese government bond market.

The following day, JGB yields spiked to 2.35%, hitting their highest level since February 1999. Yields on 30-year and 40-year bonds broke through 3.875% and 4.215%, respectively, with the latter entering the "4% era" for the first time in history. The JGB market experienced its most intense volatility since 2007, with multiple traders describing it as the "most chaotic trading day in years."

At the same time, weak 20-year JGB auction results exacerbated concerns over Takaichi's fiscal policies, creating a vicious cycle of "selling, heightened anxiety, and more selling."

A repeat of the UK gilt crisis in Japan?

Pooja Kumra, European and UK rates strategist at TD Securities, noted that the "shock" stemming from sustained pressure on ultra-long JGBs is transmitting to global rates markets. De-risking and margin calls remain realistic risks that could trigger a broader market reaction, drawing comparisons to the 2022 UK gilt crisis.

The so-called "Truss moment" refers to the collapse of market confidence and the plunge in government bonds triggered by former UK Prime Minister Liz Truss's proposal for unfunded tax cuts in 2022, which led to her swift resignation. Today, similar scenes are playing out in Japan.

Sanae Takaichi vowed to end excessive fiscal austerity and implement large-scale investment and tax-cut plans. She stated that Japan needs to boldly break free from old fiscal constraints, asserting that it "must enhance risk-response capabilities to drive long-term growth where taxes sustain taxes." Her team plans to implement loose fiscal policies, such as a consumption tax cut, but the lack of clarity regarding funding sources has sparked deep market concern.

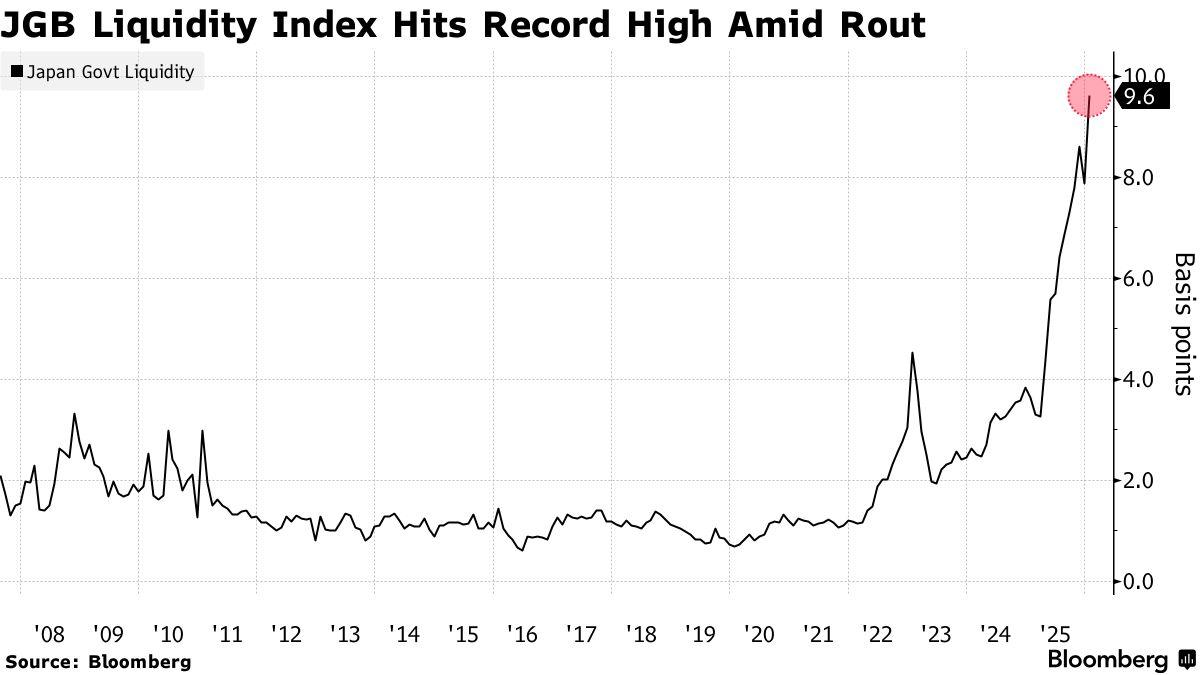

Meanwhile, consecutive failed 20-year JGB auctions indicate a sharp drop in demand, with market liquidity deteriorating rapidly. Bloomberg data shows the JGB liquidity index has soared to a record high, reflecting a severe imbalance between supply and demand.

U.S. Treasury Secretary Scott Bessent remarked: "The volatility in the Japanese bond market has reached 'six sigma.' If this happened in the U.S. Treasury market, the 10-year yield could skyrocket by 50 basis points."

The Bank of Japan's dilemma

During this politically sensitive period with an upcoming snap election and high fiscal uncertainty, the Bank of Japan is caught in a dual bind between "fighting inflation" and "stabilizing the market," facing a difficult dilemma.

Tim Sun, a senior researcher at HashKey Financial Services Group, pointed out that if Japan uses interest rate hikes to curb the bond sell-off, global liquidity will be rapidly squeezed. However, if the status quo is maintained without intervention, JGB yields and the exchange rate could spiral out of control simultaneously, creating a chain reaction.

In his view, the central bank is unlikely to tighten policy abruptly in the short term, preferring to "buy time" to manage the current crisis. Key measures would include strengthening market communication, stabilizing expectations, and, if necessary, taking unconventional steps such as currency intervention or targeted bond purchases to keep yield volatility within a manageable range.

Tim Sun emphasized that as one of the world's largest sovereign creditors, Japan's bond market is massive and deeply embedded in the global financial system. If long-term JGB yields continue to climb, it would prompt domestic capital to withdraw from overseas assets like U.S. Treasuries or European bonds and return home, thereby raising global borrowing costs and compressing the valuation of risk assets. Such spillover effects pose a substantial shock to global capital markets.

UBS traders also noted that Japan's current predicament is somewhat similar to the 2022 UK gilt crisis. The issue lies not just in the fiscal easing measures themselves, but more critically in the lack of coordination with central bank objectives. On one hand, the new government is making high-profile promises of fiscal expansion; on the other, the central bank is caught between inflationary pressures and bond market turmoil.

To make matters worse, the loose fiscal path promoted by Takaichi has left the market increasingly uneasy about the future of the yen and the bond market. If the policy logic lacks internal consistency, market confidence in the coordination between the government and the central bank will quickly erode, and the "imagined dividends" will vanish.

Regarding market expectations that the Bank of Japan might intervene, many analysts believe there are indeed feasible policy tools available.

For instance, resuming unlimited fixed-rate bond purchases to cap long-term rates is one option for curbing further yield increases in the short term. However, such an operation could be interpreted as fiscal monetization—where the central bank finances the government by printing money to buy bonds—thereby fueling concerns over Japan's fiscal sustainability and intensifying the sell-off of the yen.

Furthermore, policymakers might choose to postpone the balance sheet reduction (QT) originally scheduled to begin in 2026, maintaining the current pace of JGB purchases to stabilize market liquidity. Regarding communication, the central bank might attempt to guide market sentiment toward a soft landing through more dovish or ambiguous language at upcoming monetary policy meetings.

Although these moves might ease market pressure in the short term, core issues remain unresolved. If the new government fails to send a clear signal regarding fiscal discipline, the trend of investors reassessing Japan's long-term risk will continue. Even with frequent intervention by monetary authorities, it may only serve to delay rather than reverse the repricing of risk.

Regarding whether the "ultimate weapon" of unlimited bond purchases will eventually be used, Gareth Berry stated that there are currently no signs the Bank of Japan intends to deploy the mechanism immediately. He noted that this policy tool, introduced by former Governor Haruhiko Kuroda, remains a "backup option." While current Governor Kazuo Ueda has consistently maintained a more restrained monetary policy stance, he may be left with no choice if market instability persists.

Japan's second-largest bank preparing to "buy the dip"?

Sumitomo Mitsui Financial Group (SMFG), Japan's second-largest commercial bank, has stated plans to significantly increase its holdings of domestic sovereign bonds once the market stabilizes, rebuilding its allocation to Japanese Government Bonds (JGBs). Arihiro Nagata, the bank's head of global markets, revealed that the goal is to double the current JGB portfolio of approximately 10.6 trillion yen (around $67 billion) once yield volatility settles.

This move signals that the major financial institution is shifting its focus from its previous emphasis on overseas bond investments back to the Japanese domestic market.

In an interview, Nagata admitted that while the market is still in a period of turbulence, the bank will make a "strong return" to the JGB market once the spike in yields eases. He disclosed that Sumitomo Mitsui has already begun making small-scale purchases as 30-year JGB prices gradually approach fair value.

Currently, the securities portfolio of the group's banking unit, Sumitomo Mitsui Banking Corp., is dominated by overseas bonds, with holdings of approximately 12 trillion yen.

Although SMFG's current JGB holdings are primarily short-term with an average duration of just 1.7 years, and its peak holdings reached 15.8 trillion yen in March 2022, Nagata stated that the planned rebuilding of its position could "far exceed" that historical high.

While concerns remain regarding the rapid surge in long-term yields, Nagata noted that at the start of the week, the 30-year yield had begun returning toward fair value, after soaring more than 25 basis points in a single day.

However, he also emphasized that the bond market is currently being influenced by Sanae Takaichi's fiscal policies and the risk of the main opposition party driving up inflation. As a result, yields could still climb further, and Sumitomo Mitsui has not yet opted for a "full entry."

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.