U.S. April Nonfarm Commentary: With Robust Employment, How Could U.S. Equities Not Rise?

The April non-farm payrolls data exceeded expectations. Should the labour market continue to demonstrate resilience, it could prevent a technical recession in the U.S. The persistent downward trend in inflation is likely to spur the Federal Reserve to restart its rate-cutting cycle. Bolstered by these two forces, we are optimistic about U.S. equities in the short term (0-3 months).

Source: Refinitiv, Tradingkey.com

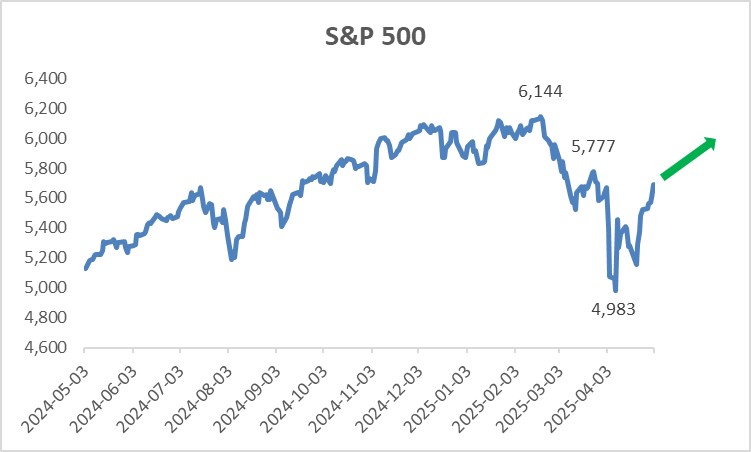

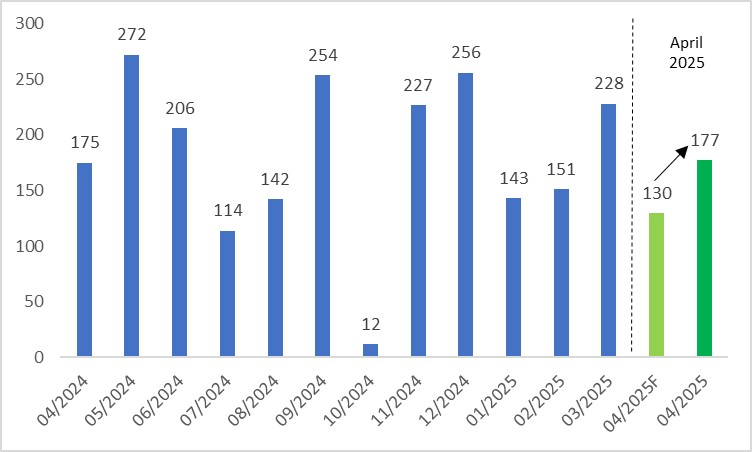

On 2 May 2025, the U.S. released its April Non-Farm Payrolls (NFP) data, reporting 177,000 new jobs (Figure 1). While lower than the prior month’s 228,000, this figure significantly surpassed market expectations of 130,000 (Figure 2), underscoring ongoing labour market strength. Following the release, U.S. major stock indices surged.

Figure 1: Consensus Forecasts and Actual Data

Source: Refinitiv, Tradingkey.com

Figure 2: Nonfarm Payrolls (000)

Source: Refinitiv, Tradingkey.com

Two factors drove the stronger-than-expected NFP figures. First, government layoffs slowed. Second, tariff-induced pre-emptive importing boosted employment in the transportation and warehousing sector. Across industries, construction also saw a notable increase of 11,000 jobs, driven by a surge in goods production.

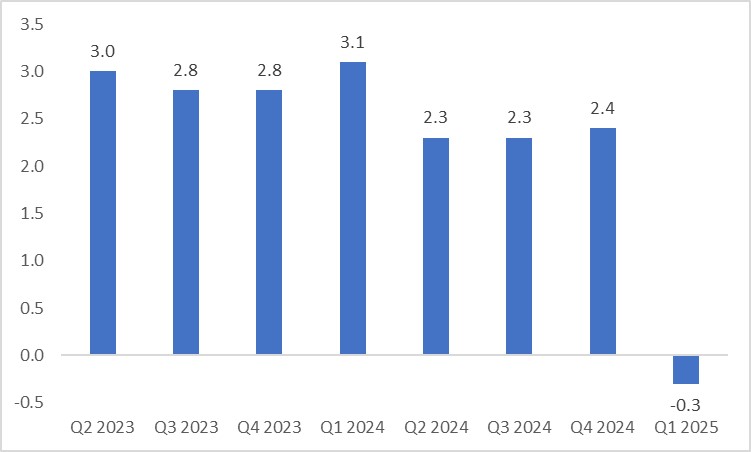

Despite negative annualized real GDP growth in Q1 2025 (Figure 3), continued labour market resilience in the coming months is likely to turn Q2 GDP positive, averting a technical recession.

Figure 3: Annualized Real GDP (q-o-q, %)

Source: Refinitiv, Tradingkey.com

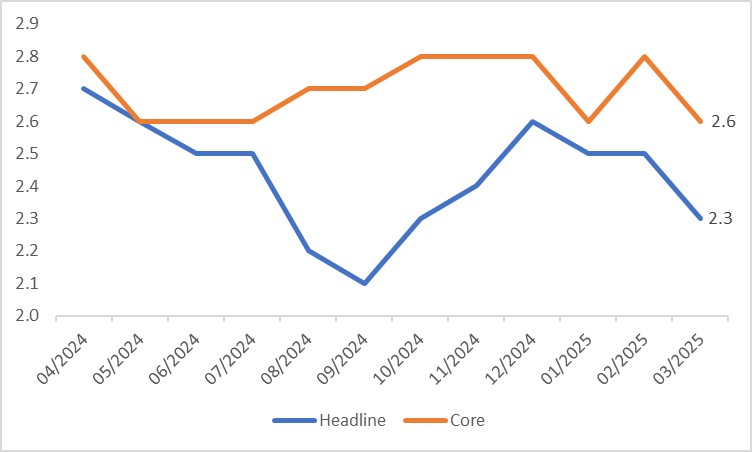

While some economists argue that a robust labour market may delay Federal Reserve rate cuts, we disagree. The Fed’s rate decisions consider not only growth and employment but also inflation. The Fed’s preferred inflation gauge, PCE, has been gradually declining since the end of last year (Figure 4). Although tariffs may temporarily push inflation higher, we believe the broader trend toward the Fed’s 2% target remains intact. Consequently, we expect the Fed to resume rate cuts as early as June. Supported by a strong labour market and anticipated Fed rate cuts, we are bullish on the outlook for US equities.

Figure 4: PCE (y-o-y, %)

Source: Refinitiv, Tradingkey.com

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.