JGB Yields Break 4%. Sanae Takaichi’s Political Gamble Is Setting Off a Massive Wave of Global Capital

AI Podcast

Japanese 40-year bond yields surged to 4% for the first time in 30 years, coinciding with Prime Minister Takaichi's election pledge for fiscal expansion and tax cuts. This policy mix of "Tight Money + Loose Fiscal" is eroding market confidence, particularly as the Bank of Japan raises rates amidst persistent inflation. The narrowing US-Japan interest rate differential is forcing the unwinding of the $1 trillion yen carry trade, leading to potential significant declines in global risky assets, including US stocks and cryptocurrencies. Emerging markets with high external debt are particularly vulnerable. The Japanese stock market's rally, driven by capital migration and yen weakness, faces fragility from further bond yield increases.

TradingKey - Tuesday, A "depth charge" was dropped into global financial markets on Tuesday as the yield on Japan's 40-year government bond returned to the 4% threshold for the first time in 30 years, hitting a historical peak since the security's issuance in 2007. Furthermore, this bond market storm coincided with Prime Minister Sanae Takaichi's general election announcement. At a press conference on Monday, Takaichi officially confirmed that the House of Representatives will be dissolved this Friday (the 23rd), with a snap election to be held on February 8, while also making a major pledge to "reduce the food consumption tax from 8% to 0%."

A global financial storm is brewing in Japanese financial markets, where a political gamble on Japan's sovereign credit is sending shockwaves through the capillaries of capital flows into the global financial system. The arbitrage logic built over three decades of low interest rates is collapsing, and the "shifting tide" of global capital is quietly opening a Pandora's box.

"Tight Money + Loose Fiscal" Policies are Piercing Market Trust

JGB yields breaking above 4% and the rapid fall in bond prices indicate that investors are voting with their feet, puncturing the Japanese economy's false equilibrium. Japan's debt-to-GDP ratio has soared to 240%, the highest among major global economies, kept alive for years by the Bank of Japan's "unlimited backstop" and a low-interest-rate environment. However, for the sake of votes, Sanae Takaichi has added a heavy burden to this fragile debt chain.

Takaichi's core motive for calling a snap election is to consolidate her governing base, while the expansionary fiscal promises in her platform have become the direct catalyst for bond market volatility. To win over voters, Takaichi promised that if re-elected, she would cut the food consumption tax from 8% to 0%, a move mirrored by the opposition coalition. While this policy could stimulate short-term consumption, the market is broadly concerned it will exacerbate the fiscal deficit.

With inflation continuing to rise, the Bank of Japan is being forced to hike rates. Japan's core CPI has exceeded the 2% target for 44 consecutive months and is nearing the 3% mark, forcing the central bank to raise the policy rate to 0.75%, the highest since 1995.

Since the Takaichi cabinet took office, it has introduced an economic stimulus package worth 21.3 trillion yen, with the fiscal year 2026 budget climbing to 122.3 trillion yen, including 29.6 trillion yen in new bond issuance—a significant expansion from the previous year.

Government bonds are essentially financing tools; fiscal expansion inevitably leads to a surge in bond issuance. Meanwhile, the Japanese bond market faces a contraction in demand: the Bank of Japan has been tapering purchases since starting quantitative tightening, domestic life insurers and banks are paring holdings due to unrealized losses on long-dated bonds, and risk-sensitive overseas investors remain on the sidelines. This supply-demand gap has pressured bond prices downward and passively driven yields higher.

This contradictory operation of "the central bank raising rates to control inflation while the government spends to buy votes" has completely shattered market confidence in the sustainability of Japanese debt.

Barclays strategists noted that the competition among political parties for fiscal expansion has brought concerns about JGB supply-demand imbalances to a fever pitch, as the shadow of bond sell-offs seen before previous Upper House elections looms over the market once again.

The US-Japan Yield Spread Reverses, Shifting Global Capital Flow Trends

The core logic of global capital flow has always been "profit-seeking." With the Federal Reserve's continued rate cuts and the Bank of Japan's rate hikes, the US-Japan interest rate differential is changing rapidly, and JGB yields breaking 4% are becoming a primary driver for global capital movements.

For the past thirty years, the yen carry trade has supported a huge portion of global risk assets—investors borrowed yen at near-zero cost to invest in high-yield assets like US Treasuries and stocks, profiting from both interest rate differentials and asset appreciation. Today, however, this arbitrage logic has completely broken down.

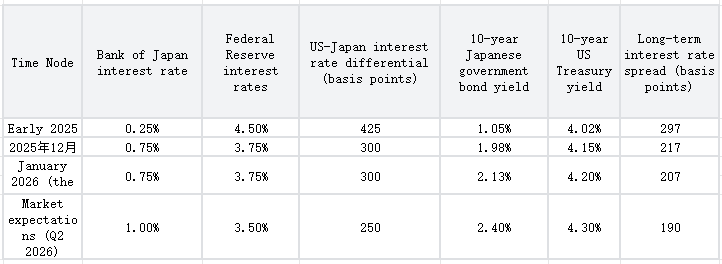

The following table shows the changes in the US-Japan yield spread since 2025, clearly illustrating a trend of narrowing or even reversal, which has triggered a chain reaction in capital flows:

Changes in US-Japan Yield Spread

Data shows the US-Japan spread has plunged from 525 basis points at the start of 2025 to 300 basis points, with the narrowing trend continuing. More crucially, long-end spreads continue to tighten, with the 30-year JGB yield now exceeding that of German Bunds, significantly boosting the yield appeal of Japanese bonds. This has directly triggered two major capital flow phenomena: the unwinding of carry trades and the repatriation of Japanese overseas assets, both of which will stir global capital volatility.

How Will the JGB Storm Impact Global Capital?

The global yen carry trade, valued at as much as $1 trillion, was once the "liquidity engine" for global risk assets. Now, with yen financing costs soaring alongside JGB yields, the strategy of "borrowing yen to buy high-yield assets" is no longer viable. The August 2024 slump in global tech stocks due to carry trade unwinding was merely a preview; the unwinding wave triggered by JGB yields breaking 4% could be far more violent.

Arbitrageurs are being forced to sell assets such as US stocks, cryptocurrencies, and emerging market equities and bonds to buy back yen and repay debt, directly triggering volatility in global risk assets. Goldman Sachs estimates that the unwinding of carry trades alone could exert over 5% of downward pressure on US stocks, while leveraged assets like cryptocurrencies could see even steeper declines.

The unwinding of the yen carry trade will be a "nightmare" for emerging markets. Economies with high external debt, such as Turkey and Argentina, will be the first to suffer. International investors, forced to sell these countries' assets to repay yen-denominated debt, will trigger capital flight and currency devaluation.

Li Qingru, a researcher at the Chinese Academy of Social Sciences, warns that the reduction of overseas asset holdings by Japanese financial institutions will further tighten global liquidity. This contraction, transmitted through international investor networks, will push up global risk premiums, worsening the financing environment for developing countries and potentially triggering localized debt crises.

The most peculiar phenomenon in the JGB storm is the "contrarian move" of the Japanese stock market—the Nikkei 225 has strengthened against the trend, reaching historical highs and creating a spectacle of "equity-bond divergence." Behind this is not an improvement in economic fundamentals, but rather a "cross-market rotation" of domestic funds.

On one hand, investors are pulling capital from the crashing bond market and pouring it into stocks in search of safety and returns. On the other hand, the yen's depreciation favors the earnings of export-oriented companies, while the food retail sector has risen on expectations of a consumption tax cut (Seven & i Holdings up 5%, Ajinomoto up 6.07%), collectively buoying the market. However, this prosperity is extremely fragile; if JGB yields rise further, capital flight will follow, and Japanese stocks will face a double blow to valuations and liquidity.

Takaichi’s Election Could Exacerbate Global Financial Market Volatility

The outcome of Sanae Takaichi's election will serve as a "watershed" for global capital flows. A LDP victory would likely mean increased fiscal expansion, pushing JGB yields further above 4.5%, accelerating capital repatriation and carry trade unwinding, and intensifying global market volatility. An election upset would trigger short-term risk-aversion due to policy uncertainty, but the yen's long-term weakness would remain difficult to reverse.

For global investors, the asset valuation framework reliant on low-interest yen leverage has completely collapsed, making high-dividend, low-volatility assets the new safe havens. For central banks, managing the capital shocks triggered by JGB volatility while balancing growth and risk prevention will be an unprecedented challenge.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.