China July Money Supply Commentary: M2 Growth Rises More Than Expected

China July Money Supply Commentary

TradingKey - On 13 August 2025, the People's Bank of China released the statistical data on broad money supply (M2) for July. The data showed that M2 increased by 8.8% year-on-year, a growth rate that not only exceeded the market's previous general expectation of 8.2% but also was higher than the previous period's 8.3%. The relatively large increase in M2 mainly stems from two factors: first, the impact of a low base formed by the relatively low growth rate of M2 in the same period last year; second, the resolution of debts has promoted the improvement of corporate capital flows.

Looking forward, the primary objective of monetary policy is projected to remain centred on economic growth and full employment. Moreover, domestically, China's inflation rate continues to stay in a low range; internationally, the U.S. dollar index is lingering at a low level, and the depreciation pressure on the RMB exchange rate has been somewhat eased. These internal and external conditions offer favourable support for the People's Bank of China to further adopt reserve requirement ratio cuts and interest rate reductions. Under the overall environment of loose monetary policy, we expect the growth rate of money supply to remain relatively high in the upcoming months.

Main Body

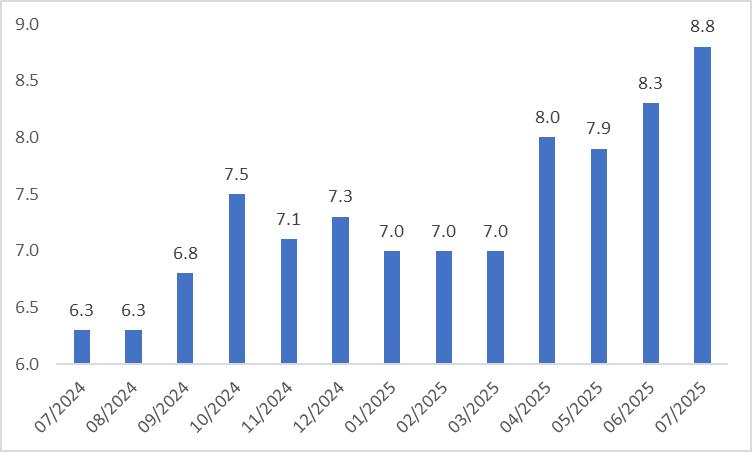

On 13 August 2025, the People's Bank of China (PBOC) released the statistical data on broad money supply (M2) for July. The data showed that M2 grew by 8.8% year-on-year, a growth rate that not only exceeded the market's previous consensus forecast of 8.2% but also surpassed the prior period's 8.3% (Figure 1). Meanwhile, the stock of social financing scale rose by 9% year-on-year, and the outstanding balance of RMB loans increased by 6.9% year-on-year. Excluding the impact of debt restructuring factors, the growth rate of outstanding RMB loans was close to 8%—a trend that continues to reflect the orientation of maintaining a moderately accommodative monetary policy.

The 0.5 percentage point increase in M2 in July from the previous value (Figure 1) stems mainly from two factors. First, it is influenced by the low-base effect resulting from the relatively low growth rate of M2 in the same period last year. Second, the resolution of debts has improved the cash flow of enterprises. It is worth noting that the growth gap between narrow money supply (M1) and broad money supply (M2) stood at 3.2% in July, which has narrowed significantly from the peak in September last year. This change reflects the rising level of capital activation and improved circulation efficiency in the current market, indicating that various policies aimed at stabilising the market and expectations have effectively boosted market confidence.

Figure 1: China M2 Money Supply (%, y-o-y)

Source: Refinitiv, TradingKey

Looking to the future, the primary objective of monetary policy is projected to stay centred on economic growth and full employment. Moreover, domestically, China's inflation remains within a low range (Figure 2); externally, the U.S. dollar index is trading at low levels, easing the depreciation pressure on the RMB exchange rate to a certain degree. These internal and external conditions offer favourable support for the People's Bank of China to further roll out reserve requirement ratio and interest rate cuts. In the overall environment of loose monetary policy, we expect the growth rate of money supply to stay relatively high in the months ahead.

Figure 2: China CPI (%, y-o-y)

Source: Refinitiv, TradingKey

China July Money Supply Preview

TradingKey - On 15 August 2025, the People's Bank of China will release the July data on broad money supply (M2). The market generally expects that the year-on-year growth rate of M2 in that month will be 8.2%. Although the projected year-on-year growth rate of M2 in July is expected to decrease by 0.1 percentage points compared with June, this forecast figure still remains at a high level within the year.

There are mainly three reasons for this prediction: First, it is affected by the low base effect; Second, the advancement of enterprises' capital expenditure plans and the recovery of residents' consumption confidence; Third, the year-on-year increase in loans and the accelerated pace of government bond issuance have led to an expansion in the corresponding scale of money creation and an increase in derived deposits.

Looking ahead, the primary goal of monetary policy is expected to remain focused on economic growth and full employment. Furthermore, the downward pressure on the RMB exchange rate has eased, while inflation remains at a low level—both of which provide support for the People's Bank of China to further implement reserve requirement ratio cuts and interest rate reductions. Against the backdrop of an overall accommodative monetary policy environment, the growth rate of money supply is projected to stay at a relatively high level in the coming months.

Main Body

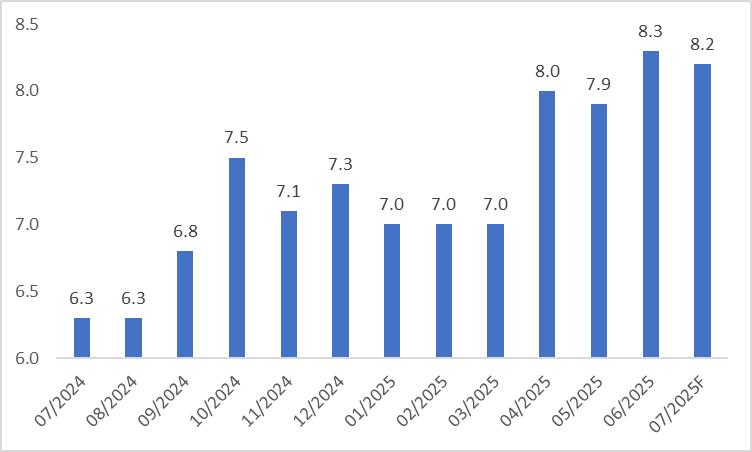

The People's Bank of China will release the data on broad money supply (M2) for July on 15 August 2025. Market forecasts generally indicate that the year-on-year growth rate of M2 for that month will be 8.2%, slightly lower than the 8.3% in June (Figure 1).

Figure 1: Consensus Forecasts

Source: Refinitiv, TradingKey

Although the year-on-year growth rate of M2 in July is expected to drop by 0.1 percentage points compared with that in June, the figure still remains at a high level within the year (Figure 2). This prediction can be mainly attributed to the following three factors:

First, the high growth rate of the money supply is largely related to the low base effect in the same period last year. Affected by factors such as the rectification of irregular "manual interest supplements" and the shift of residents' deposits to wealth management products driven by the bond "bull market", the year-on-year growth rate of M2 in July last year was only 6.3%, staying in a historically low range. This has also provided base-level support for the rebound in the growth rate in July this year.

Second, the growth rate of M1 is expected to accelerate upward in July, mainly due to the advancement of corporate capital expenditure plans and the recovery of residents' consumption confidence. Specifically, the ongoing effectiveness of the consumer goods trade-in policy will drive the implementation of corporate capital expenditure plans and a rebound in residents' consumption confidence, thereby increasing the degree of capital activation.

Third, the acceleration of M2 growth may mainly stem from two aspects: On one hand, there has been a year-on-year increase in new loans, which has led to a corresponding year-on-year rise in deposits. On the other hand, the issuance of government bonds has been front-loaded, and financial institutions have increased their investments in government bonds, with the scale of corresponding monetary creation expanding accordingly.

Figure 2: China M2 Money Supply (%, y-o-y)

Source: Refinitiv, TradingKey

There is an inseparable connection between the money supply and the monetary policy of the People's Bank of China. The introduction of the "507 Plan" of monetary policies can be regarded as a declaration that monetary policy has entered a phase of substantive easing.

Looking ahead, the primary goals of monetary policy are expected to remain focused on economic growth and full employment. Additionally, from an external perspective, the US dollar index has stayed at a low level, alleviating the depreciation pressure on the RMB exchange rate. Internally, China's inflation level remains low (Figure 3). These internal and external conditions provide support for the central bank to further implement reserve requirement ratio cuts and interest rate reductions. Against the backdrop of an accommodative monetary policy environment, we anticipate that the growth rate of the money supply will remain at a relatively high level in the coming months.

Figure 3: China CPI (%, y-o-y)

Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.