ECB July Rate Decision Commentary: Euro Bulls Should Exercise Caution Amid Potential Mid-Term Reversal

TradingKey - On 24 July 2025, the European Central Bank (ECB) released its decision on policy interest rates, maintaining all three key rates as anticipated, with the deposit facility rate steady at 2%. The decision to hold rates steady stems from two main factors. First, regarding inflation: ongoing wage growth persistence raises the risk of renewed inflationary pressures in the Eurozone in the near term, with core CPI still exceeding the ECB’s 2% target. Second, on the growth front: July’s manufacturing and services PMI figures improved compared to previous readings, reflecting a recovery in the Eurozone economy. These conditions suggest the ECB is not yet compelled to pursue rate reductions this month. Moving forward, potential tariffs from a Trump administration could hinder Eurozone economic growth, which may alleviate inflationary pressures. Consequently, the ECB is likely to lean toward a looser monetary policy. In the short term (0-3 months), the global push for de-dollarisation continues to shape forex markets, putting downward pressure on the U.S. dollar index and offering temporary support for the euro. This creates potential gains for euro-dollar bullish trades. However, in the medium term (3-12 months), continued ECB rate cuts could suppress the euro’s value. As the EUR/USD pair is likely to experience an initial uptrend followed by a downturn, euro bulls should remain cautious of a possible mid-term trend reversal.

Source: TradingKey

Main Body

On 24 July 2025, the European Central Bank (ECB) released its policy interest rate decision, aligning with widespread market expectations by maintaining all three key rates unchanged, with the deposit facility rate steady at 2% (Figure 1).

Figure 1: Market Consensus Forecasts vs. Actual Data

%20(2).jpg)

Source: Refinitiv, TradingKey

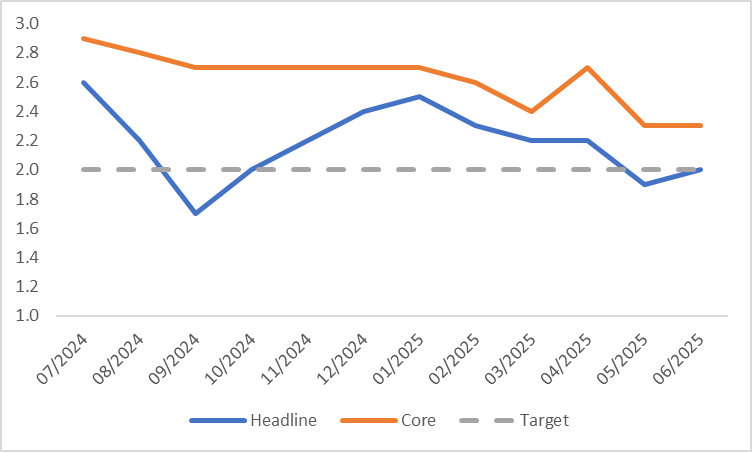

The choice to keep interest rates steady in July was based on two key considerations. First, on the inflation front: while headline CPI inflation fell sharply from 2.5% in January to 2% in June, wage growth continues to remain strong. If this persistent wage pressure continues, the Eurozone may face the risk of renewed inflation in the short term. The ECB closely monitors core CPI, which is currently at 2.3%, above the 2% target set by the ECB (Figure 2). With sustained high wage growth and elevated core inflation levels, the ECB found it difficult to pursue additional rate reductions in July.

The second consideration pertains to economic growth: bolstered by synchronised monetary and fiscal measures, the Eurozone economy has demonstrated significant progress. According to high-frequency data, the preliminary composite Purchasing Managers’ Index (PMI) for July advanced to 51 from 50.6 in June. In detail, the services PMI rose from 50.5 to 51.2, and the manufacturing PMI increased from 49.5 to 49.8, reaching its highest level in 36 months. In light of this economic upturn, the ECB sees no immediate need to implement ongoing rate reductions.

Figure 2: Eurozone CPI (%, y-o-y)

.jpg)

Source: Refinitiv, TradingKey

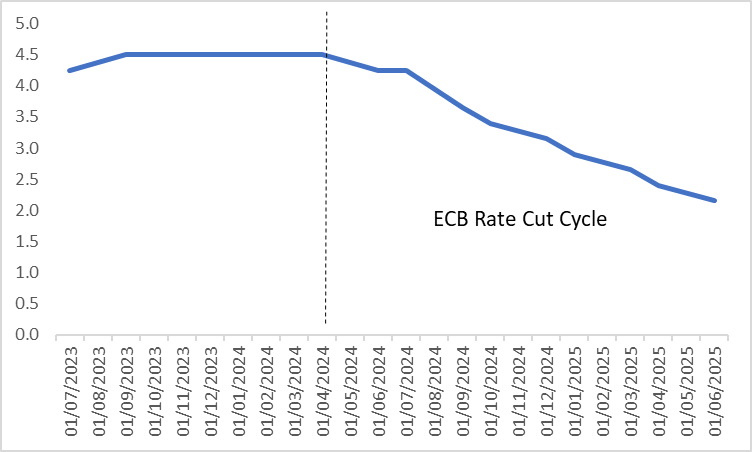

Following the start of rate reductions in June 2024, the European Central Bank (ECB) has lowered policy rates by a total of 235 basis points (Figure 3). We project that the ECB will resume cutting rates in September, likely leading the Eurozone into a low-rate environment by mid-2026. This expectation is again based on two primary considerations: economic growth and inflation dynamics. From a growth perspective, the Eurozone faces significant risks from U.S. foreign policy, notably Trump’s recent hints at imposing 30% tariffs. If such measures slow Eurozone or global economic growth, the ECB is poised to implement a more dovish monetary policy. On the inflation front, reduced economic growth could dampen demand-side inflationary pressures. According to the ECB’s June forecasts, inflation is expected to stabilise at 2% in 2025 and drop to an average of 1.6% in 2026. With inflation trending lower, the ECB can pursue further rate cuts without heightened concerns about resurgent inflation.

The ongoing global shift toward de-dollarisation will continue to be a pivotal driver of foreign exchange market trends over the short term (0-3 months). This movement is expected to weaken the U.S. dollar index, offering temporary support to the euro’s exchange rate. Consequently, investors with bullish EUR/USD positions may still see profit potential. However, in the medium term (3-12 months), persistent ECB rate cuts are likely to suppress the euro’s value. As the EUR/USD pair is anticipated to rise initially before declining, those trading long on the euro should remain cautious of a potential mid-term trend reversal in their strategies.

Figure 3: ECB Policy Rate (%)

%20(1).jpg)

Source: Refinitiv, TradingKey

TradingKey - On 24 July 2025, the European Central Bank (ECB) will announce its policy interest rate decision. The prevailing market consensus is that the ECB will maintain its policy rates unchanged, with the deposit facility rate remaining at 2%. We concur with this assessment. The decision to keep rates steady is driven by two key considerations: first, persistent inflationary pressures, with core inflation still exceeding the ECB’s 2% target; second, the Eurozone economy has entered a recovery phase since early 2025, with growth rates significantly surpassing the averages of 2023 and 2024. These factors support the rationale for maintaining policy rates in July.

Looking ahead, the tariff policies proposed by the Trump administration are expected to hinder Eurozone economic growth, potentially reducing reflation risks. Against this backdrop, the ECB is likely to adopt a more accommodative monetary policy stance in the future. Over the next 0-3 months, the global shift away from the US dollar will continue to be a key driver of foreign exchange market dynamics. This trend is likely to weaken the US dollar index, offering temporary support to the euro’s exchange rate. As a result, euro-dollar bullish trades still present profit potential. However, in the medium term (3-12 months), ongoing rate reductions by the European Central Bank are expected to exert downward pressure on the euro’s value.

Source: TradingKey

Main Body

On 24 July 2025, the European Central Bank (ECB) will release its policy interest rate decision. The prevailing market view is that the ECB will maintain its policy rates unchanged, with the deposit facility rate staying at 2% (Figure 1). We agree with this expectation.

Figure 1: Consensus Forecasts

Source: Refinitiv, TradingKey

The decision to keep interest rates steady in July is driven by two primary factors, with the first relating to inflation dynamics. Although headline CPI inflation has significantly declined from 2.5% year-on-year in January to 2% in June, disaggregated data reveals divergent trends. The recent slowdown in inflation is largely attributed to falling energy prices, while service prices continue to exhibit strong stickiness. Notably, the core CPI, which the ECB closely monitors, remains elevated at 2.3%, above the ECB’s 2% policy target (Figure 2). Given the persistent nature of headline inflation and the elevated core inflation level, these factors constrain the ECB’s ability to pursue further rate cuts.

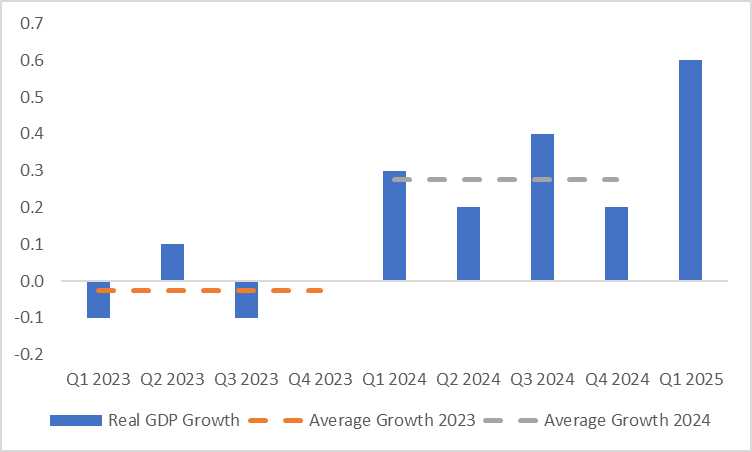

The second factor pertains to economic growth. Supported by coordinated monetary and fiscal policies, real GDP growth in the Eurozone reached 0.6% quarter-on-quarter in Q1 2025, markedly surpassing the average growth rates of 2023 and 2024 (Figure 3). Consequently, the ECB faces no immediate pressure to pursue aggressive rate cuts.

Figure 2: Eurozone CPI (%, y-o-y)

Source: Refinitiv, TradingKey

Figure 3: Eurozone Real GDP (%, q-o-q)

Source: Refinitiv, TradingKey

The European Central Bank (ECB) initiated its rate-cutting cycle in June 2024, reducing policy rates by a cumulative 235 basis points to date (Figure 4). Looking ahead, we anticipate the ECB will resume rate cuts in September, with the Eurozone likely transitioning to a low-interest-rate environment by mid-2026. This expectation is grounded in two key factors: growth and inflation dynamics. On the growth front, U.S. foreign policy poses the most significant risk to the EU economy, exemplified by recent threats from the Trump administration to impose 30% tariffs. Should such measures slow Eurozone and global economic growth, the ECB is highly likely to adopt a more accommodative monetary policy stance. On the inflation front, an economic slowdown could suppress inflationary pressures from the demand side. The ECB’s June projections indicate that inflation will stabilise at 2% in 2025, with an average of 1.6% in 2026. Against this backdrop of declining inflation, the ECB can implement further rate cuts without significant concerns about reflation risks.

Over the next 0-3 months, the global shift away from the US dollar will continue to be a key driver of foreign exchange market dynamics. This trend is likely to weaken the US dollar index, offering temporary support to the euro’s exchange rate. As a result, euro-dollar bullish trades still present profit potential. However, in the medium term (3-12 months), ongoing rate reductions by the European Central Bank are expected to exert downward pressure on the euro’s value.

Figure 4: ECB Policy Rate (%)

Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.