Petrodollar System Failing? Positive Correlation Between Dollar and Crude Hits Historical Extreme Levels

AI Podcast

The US dollar and crude oil prices exhibit a rare positive correlation, driven by Middle East geopolitical conflicts and a shift towards momentum trading over traditional macro drivers. This synchronized rise, the strongest since 2005, signals global macroeconomic pressure, potentially fueling inflation and prolonging high interest rates. Net oil importers face a double whammy of expensive oil and a stronger dollar, increasing external payment and inflation risks. This trend negatively impacts bond prices and equity valuations, especially for growth sectors, indicating geopolitical disruptions to global economic order and potential tightening of global liquidity conditions.

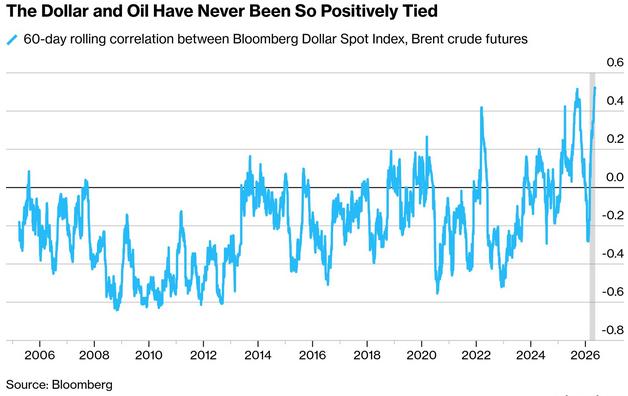

TradingKey - Against the backdrop of geopolitical conflicts in the Middle East, the positive correlation between the US dollar and crude oil prices has climbed to its highest level since the inception of the Bloomberg Dollar Spot Index in 2005, meaning the degree to which the dollar and Brent crude fluctuate in the same direction daily has reached its strongest point in over two decades.

Under the traditional logic of the "petrodollar system," global crude oil transactions are settled in US dollars; a strengthening dollar raises oil purchasing costs for non-dollar economies, thereby dampening crude demand, so the two typically exhibit a negative correlation.

However, the current US-Iran conflict has rewritten this inertia; during Thursday's New York trading session, the Bloomberg Dollar Spot Index rose by approximately 0.3%, while Brent crude futures simultaneously recorded a similar gain, with both moving in a rare synchronized fashion.

For most of the first quarter of this year, the US dollar and oil prices maintained a negative correlation, but since early March, the relationship has turned from negative to positive and has persisted to this day.

Brent Donnelly, president of Spectra Markets, noted that current market drivers have shifted from traditional macro variables to geopolitics, news events, risk appetite, and momentum trading, stating that "the core of the market narrative has been simplified to whether oil is up or down."

Global Macroeconomic Pressure Amid the Simultaneous Rise of the USD and Oil Prices

When the US dollar and crude oil prices rise in tandem, it suggests that the global macroeconomic environment is facing new pressures.

Crude oil is a key driver of global inflation. A simultaneous rise in the dollar and oil prices often indicates that rising energy costs are pushing up overall inflation expectations. Under these circumstances, the Federal Reserve may need to maintain higher interest rates for longer to curb inflation, and could even reconsider further rate hikes. Other major central banks may also become more cautious or adopt tighter policy stances to counter imported inflationary pressures.

Chris Turner, head of FX strategy at ING, said this week, "Unless there is a systemic decline in global equity markets, mild volatility in the currency market will continue to be dominated by the next major move in oil prices and the policy responses of major central banks, including the Fed, to rising inflation."

For net oil importers such as Europe, Japan, and most emerging markets, this synchronized rise creates a double whammy. In the past, a weaker dollar could partially offset the rising cost of oil imports; now, however, these countries face a situation where both "crude is more expensive" and "the dollars needed to buy it are also more expensive," causing external payment pressures and inflation risks to rise simultaneously.

As long as the positive correlation between the dollar and oil prices persists and both remain at elevated levels, market expectations will lean toward a "higher-for-longer" interest rate environment, which will continue to weigh on medium- to long-term bond prices.

The stock market is also affected, as equity valuations generally have an inverse relationship with risk-free rates (such as U.S. Treasury yields). When the dollar and oil prices jointly drive up bond yields, the discount rate for equity assets rises, and high-growth sectors like technology, which depend on future cash flows, will face greater valuation adjustment pressure.

The simultaneous rise in the dollar and crude oil is not merely market volatility, but an external manifestation of geopolitical disruptions to the global economic order. It signals that global liquidity conditions may tighten further. The end of this unconventional state may have to wait for a meaningful slowdown in global demand or significant progress in resolving geopolitical conflicts.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.