U.S. September Inflation: Prices Out of Control? Under Control? Gold's Sharp Drop—Will It Surge Again?

1. Introduction

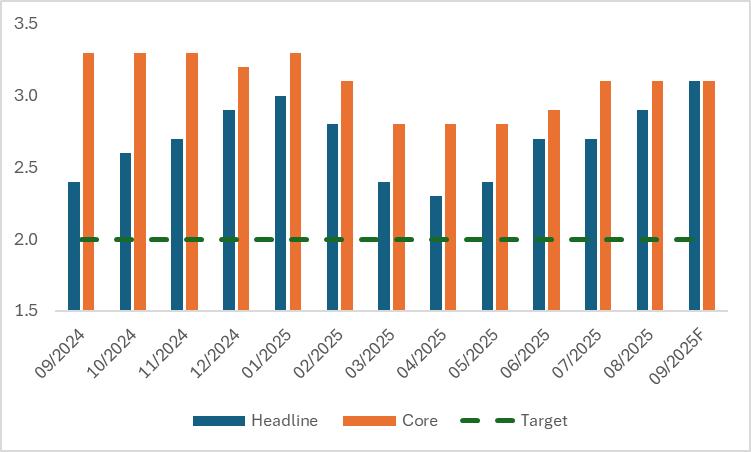

TradingKey - Gold prices have surged this year, with the latest rally primarily driven by the collapse of U.S. regional banks and the "No Kings" protest movement. However, on 21 October, gold prices experienced a sharp pullback amid rising expectations of an imminent end to the Russia-Ukraine war, marking a maximum decline of over 8%. Looking ahead, the U.S. September inflation data—due for release on 24 October—will be the pivotal event shaping gold's near-term trajectory. During the period of a U.S. government shutdown, this long-awaited report will arrive just ahead of the Federal Reserve's October interest rate meeting and stand as its most critical input. Market consensus currently projects both headline and core CPI at 3.1% for September (Figure 1).

For this critical data release, we conduct a scenario analysis: Scenario 1—September inflation far exceeds market expectations, signalling uncontrolled U.S. prices; Scenario 2—CPI meets or falls below the 3.1% consensus, indicating inflation remains under control. Our analysis concludes: In either case, gold will continue to rise and hit new highs. This underscores that, despite its substantial gains, gold remains the most reliable investment from a risk-reward perspective.

Figure 1: U.S. CPI (%, y-o-y)

Source: Refinitiv, TradingKey

2. Scenario 1: Inflation Out of Control

The risk of runaway U.S. inflation arises from several interconnected factors: persistent impacts from Trump's tariff policies, such as escalating U.S.-China trade tensions, could drive up imported goods prices; ongoing fiscal deficits and debt accumulation leading to excess money supply, with large-scale federal spending to stimulate a slowing economy supercharging demand and triggering price surges; supply chain bottlenecks and geopolitical risks, such as a delayed ceasefire in the Russia-Ukraine war or the potential resurgence of the Israeli–Palestinian conflict, spiking energy costs and importing inflationary pressures; and an eroding U.S. dollar as the global reserve currency, causing imported goods prices to soar. These forces could collectively propel inflation higher, particularly amid intensifying global economic uncertainty.

Gold prices typically rise when U.S. inflation spirals out of control, driven by four key factors: first, its inflation-hedging attribute strengthens—uncontrolled inflation rapidly erodes currency purchasing power, weakens investors' confidence in the U.S. dollar, and prompts them to shift funds to gold, a traditional safe-haven asset; as a store of value, gold offsets wealth erosion from inflation, boosting its demand and price. Second, real interest rates (calculated as nominal interest rates minus inflation rates) fall, reducing the opportunity cost of holding non-interest-bearing assets like gold and making investors more willing to hold gold instead of cash in bonds or savings accounts, further pushing up prices. Third, the U.S. dollar weakens—uncontrolled inflation may undermine its status as the world's reserve currency and cause depreciation; since gold is priced in U.S. dollars, a weaker dollar makes it cheaper for holders of other currencies, increasing international market demand and lifting gold prices. Fourth, geopolitical and economic uncertainty grows—out-of-control inflation often brings economic turmoil and policy uncertainty, exacerbating market volatility, and gold, as a "safe-haven asset," becomes more favoured amid rising uncertainty.

To sum up, runaway inflation tends to boost gold prices through multiple mechanisms, including lowering real interest rates, weakening the U.S. dollar, and increasing safe-haven demand. Historical data show that during the period of high inflation in the United States in the 1970s, gold prices rose significantly, and a similar scenario may recur in the future.

3. Scenario 2: Inflation Under Control

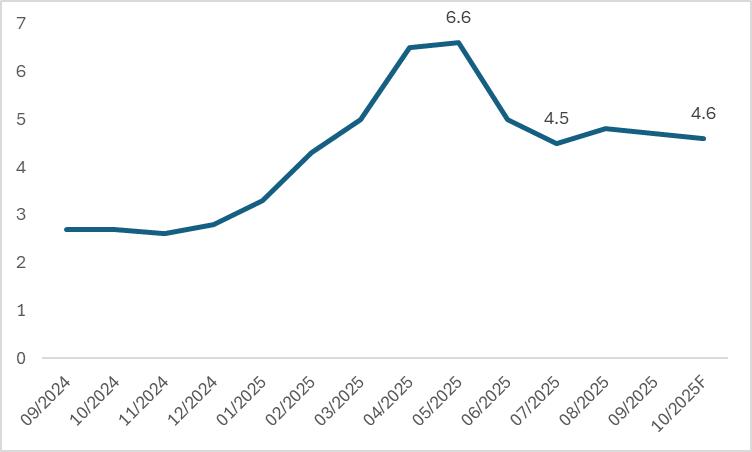

While there is a potential risk of inflation spiralling out of control in the U.S., the market generally believes the probability of inflation remaining manageable is higher. The University of Michigan's Inflation Expectations Index—an indicator measuring consumers' expectations for price changes of goods and services over the next 12 months—peaked at 6.6% in May and has since gradually declined (Figure 3). This trend suggests that U.S. inflationary pressures will be contained over the medium term.

The decline in U.S. inflation will be driven by a combination of factors. Firstly, a weakening labour market will lead to a slowdown in wage growth indicators and simultaneously reduce consumers' spending power, which may trigger a wage-consumption-price downward spiral. Secondly, while the U.S. economy remains resilient for now, the general trend of slowdown in growth has become hard to reverse, and this slowdown will curb inflation from the demand side. Finally, energy prices are expected to remain stable, which will effectively mitigate the impact of imported inflation.

The decline in inflation is one of the core drivers for the Federal Reserve to continue cutting interest rates, which is directly linked to its dual mandate of "stabilising prices and promoting full employment." High interest rates are a key tool to curb high inflation, but maintaining them at elevated levels can dampen economic vitality. After inflation falls, keeping interest rates high may increase the financing cost burden for enterprises, suppress consumption and investment, and even cool down the job market. When inflation moderates, interest rate cuts can revitalise the economy by reducing borrowing costs while avoiding the risk of an economic hard landing. In short, the easing of inflation creates room for accommodative monetary policy.

The Federal Reserve's continued interest rate cuts and other accommodative monetary policies are expected to significantly boost the rise in gold prices. As a non-yielding asset, gold generates no interest or dividends. Interest rate cuts lower the returns of interest-bearing assets such as government bonds and savings accounts, thereby narrowing the yield gap between these assets and gold. Taking the period from September to December 2024 as an example, the federal funds rate reduced from 5% to 4.5%. Short-term Treasury yields declined accordingly, prompting investors to allocate more to gold, which in turn drove up gold demand and prices. During this period, the price of gold rose from approximately $2,493 per ounce to $2,718 per ounce, representing an increase of over 9%.

Figure 3: U.S. Michigan 1-Year Inflation Expectations (%, y-o-y)

Source: Refinitiv, TradingKey

4. Conclusion

All in all, the U.S. inflation data released on 24 October are expected to be positive for gold prices regardless of whether the final result is higher or lower than the widely expected 3.1%. It can be seen that although gold prices have risen significantly so far this year, investors still need to continue monitoring the future trend of gold from a risk-return perspective. Our recommended investment strategy is that any short-term pullback should be regarded as a buying opportunity, and adopting a buy-and-hold strategy may bring high returns to investors.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.