NVDA: Big Tech's in-house silicon squeeze—can Jensen Huang find new allies?

NVIDIA (NVDA) released FY27 Q1 results (for the quarter ended Apr 2026) after the U.S. market close on May 21 Beijing time. The details are as follows.

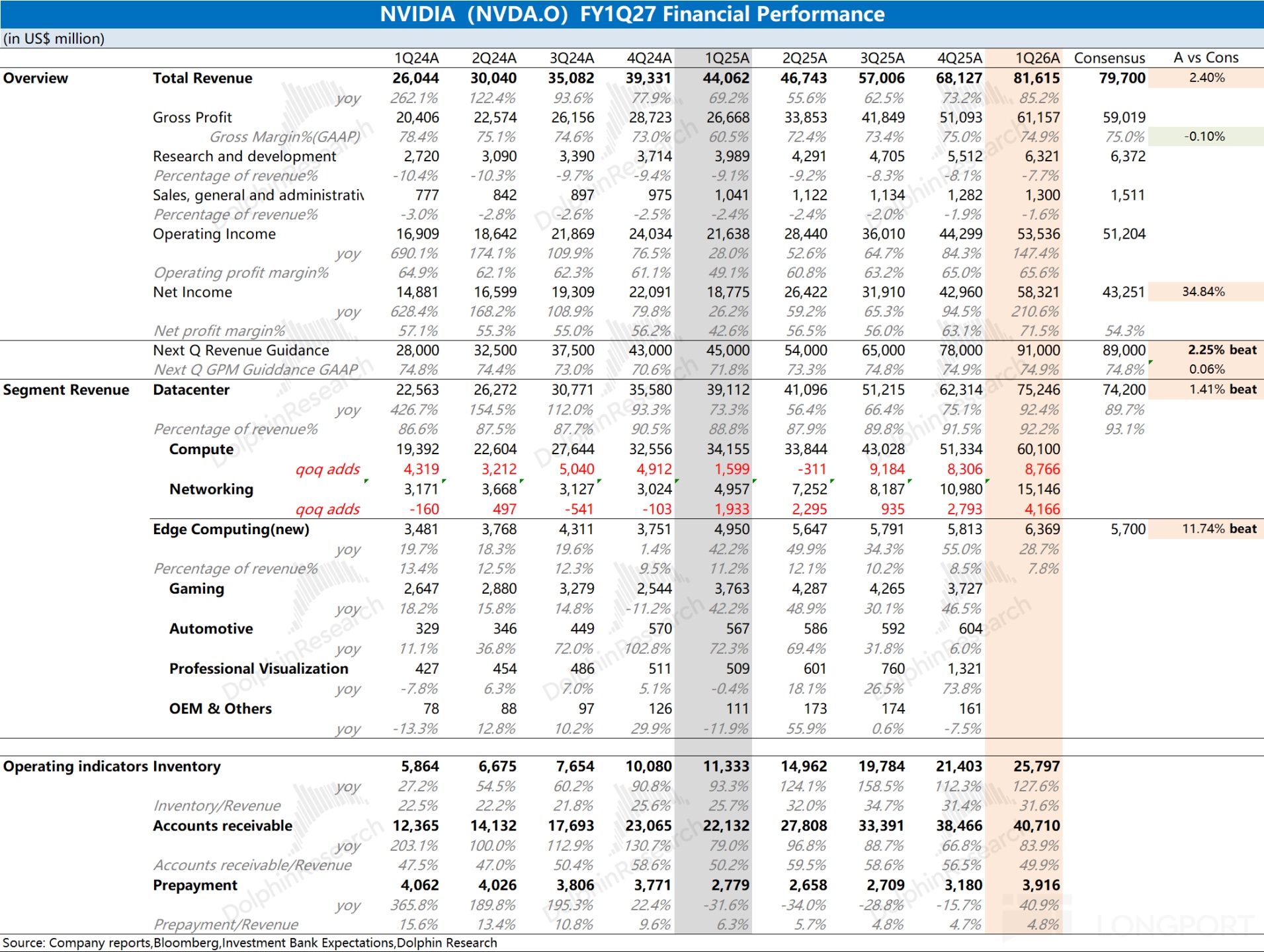

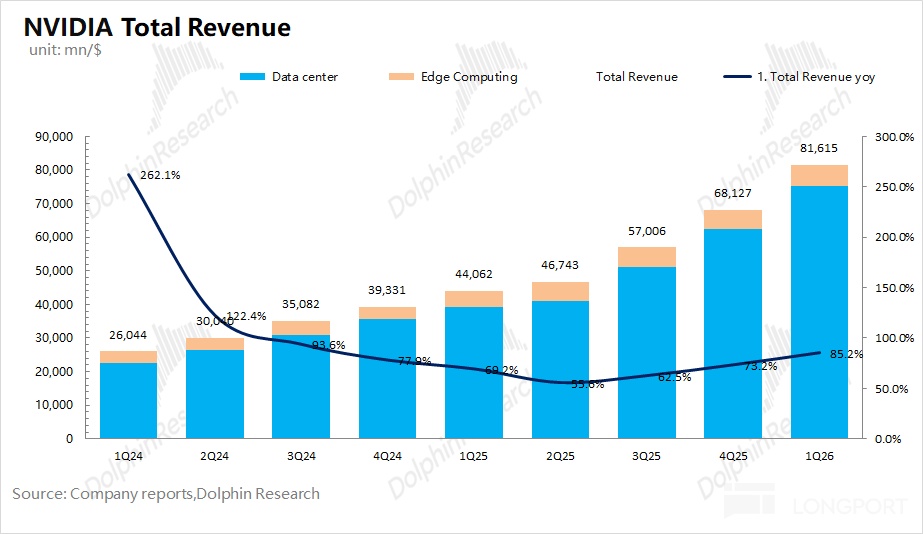

1. Key operating metrics: $NVIDIA(NVDA.US) reported revenue of $81.6bn, ahead of the raised buy-side range ($78-80bn). QoQ revenue rose by $13.5bn, driven almost entirely by higher Blackwell shipments within Data Center.

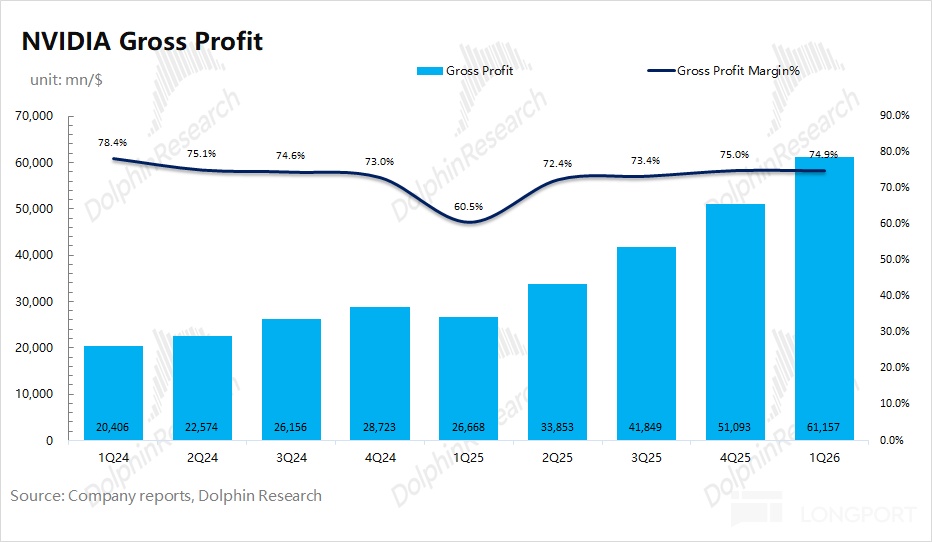

GPM was 74.9%, down 10bps QoQ and broadly in line with the ~75% street view. As B300 ramps, margins have recovered to ~75%.

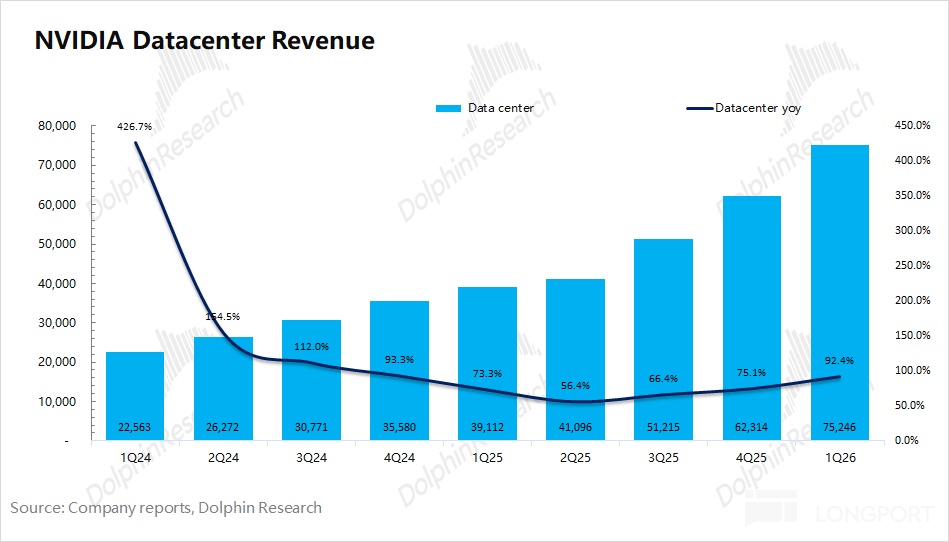

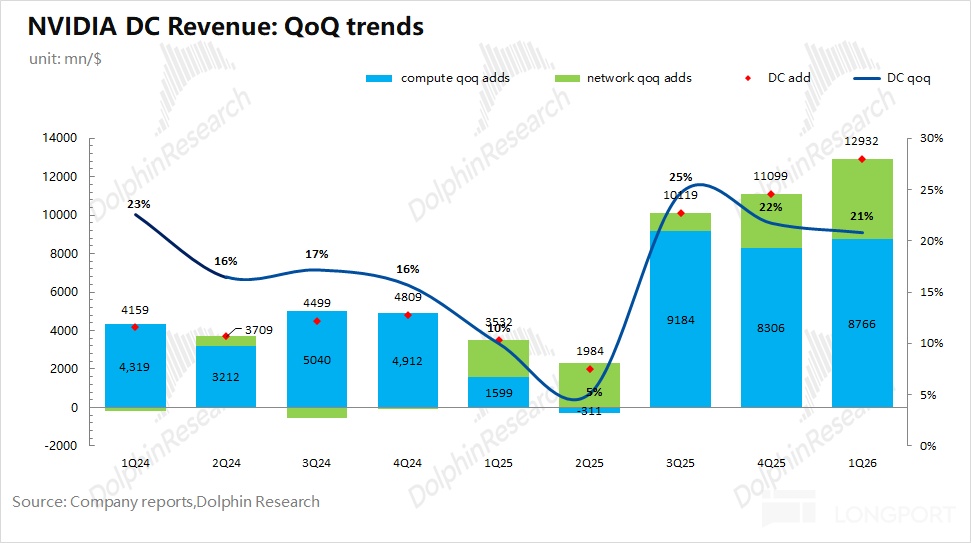

2. Data Center: Revenue was $75.2bn, with a QoQ increase of $12.9bn. Growth was led by B300-series deliveries, with the Blackwell architecture now the dominant platform across customer categories.

The company revised disclosures this quarter, moving from the prior 'Compute' and 'Networking' split to 'Hyperscalers' and 'Other cloud'. Specifically, hyperscaler revenue was $37.9bn (+$4.0bn QoQ), while other cloud revenue was $37.4bn (+$8.9bn QoQ), the biggest incremental driver.

With large cloud vendors developing in-house chips, Dolphin Research believes the customer-based split is intended to highlight NVIDIA's continued strength in industrial and enterprise cloud.

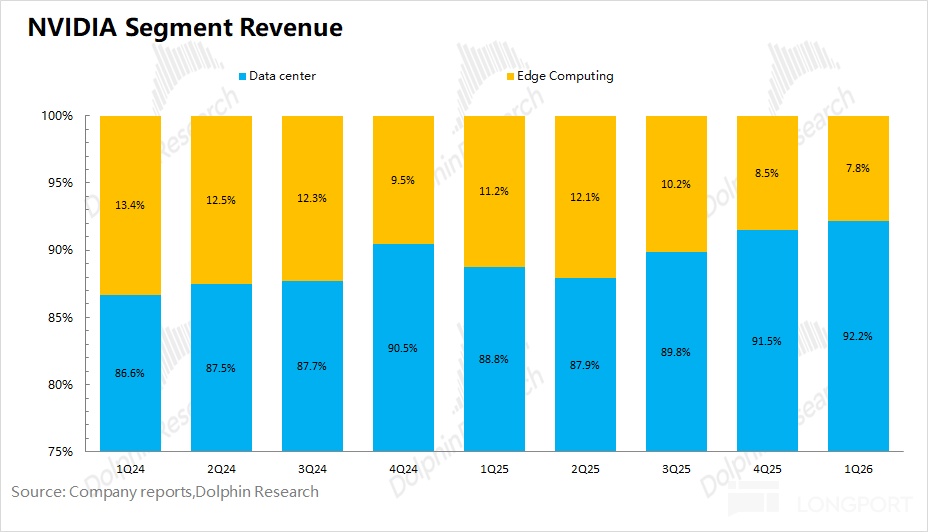

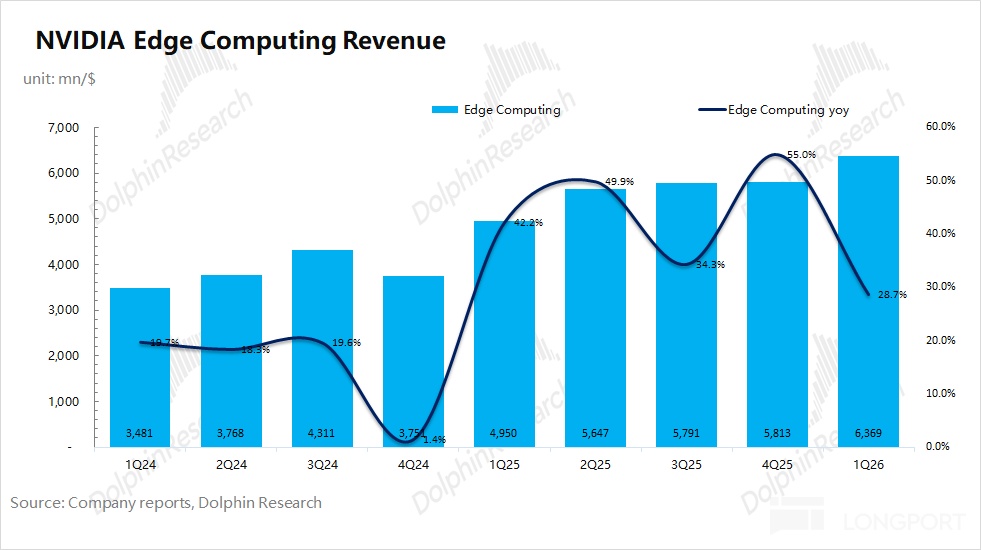

3. Edge computing: All non-Data Center businesses were consolidated into Edge this quarter, including PC, console, workstations, AI-RAN base stations, robotics and auto, with no separate line-item disclosures going forward.

Edge revenue was $6.4bn, +29% YoY. Gaming is the largest sub-segment within Edge, and the quarter's growth was primarily gaming-led.

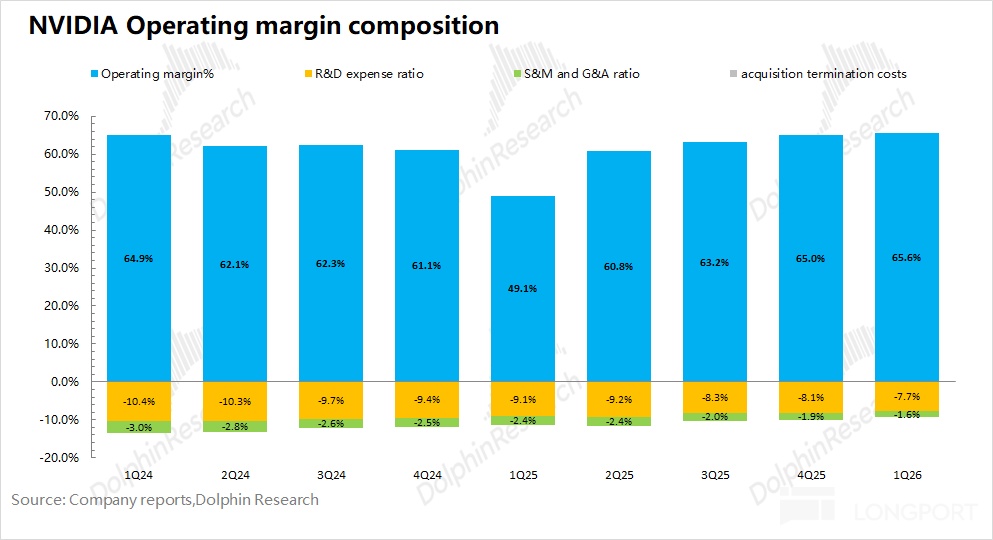

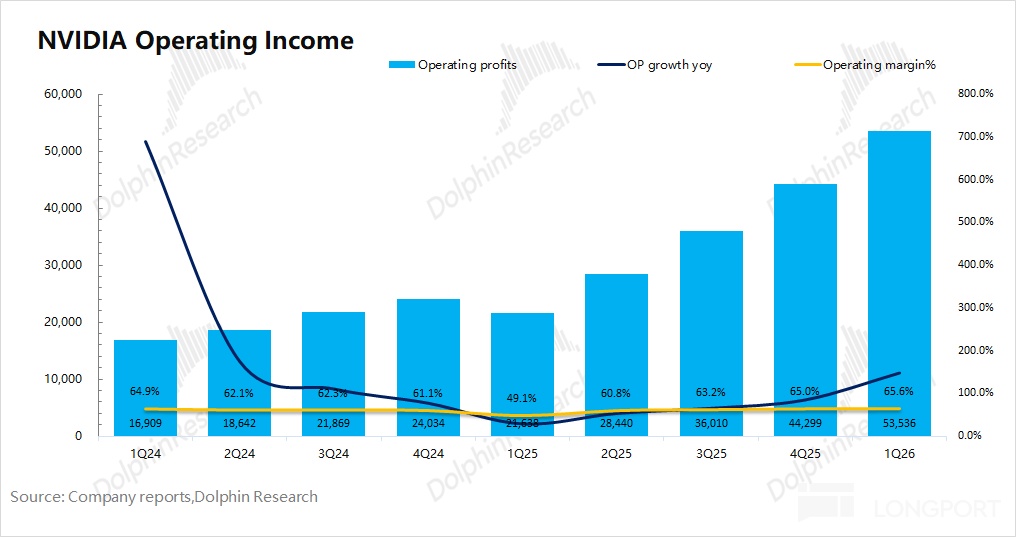

4. Profit: Core OP was $53.5bn, +147% YoY. This was driven by rapid top-line growth and GPM back near 75% (last year's GPM 'air pocket' reflected the H20 restriction), and core OPM reached 65%.

5. Guidance: For FY27 Q2 (2Q26), revenue is guided to $91.0bn, up $9.4bn QoQ, excluding China-related Data Center compute, and above the raised buy-side view (~$89.0bn). GAAP GPM is guided at 74.9%, flat QoQ, essentially in line with consensus (~74.8%).

Dolphin Research take: The compute king, now challenged on cost-performance

At GTC, Jensen Huang again raised the outlook for AI, projecting cumulative Data Center revenue of $1tn for 2025-2027 (vs. $500bn at last year's GTC). The market is therefore not overly worried about FY27-FY28 performance. As such, a modest beat this quarter is unlikely to materially lift the stock.

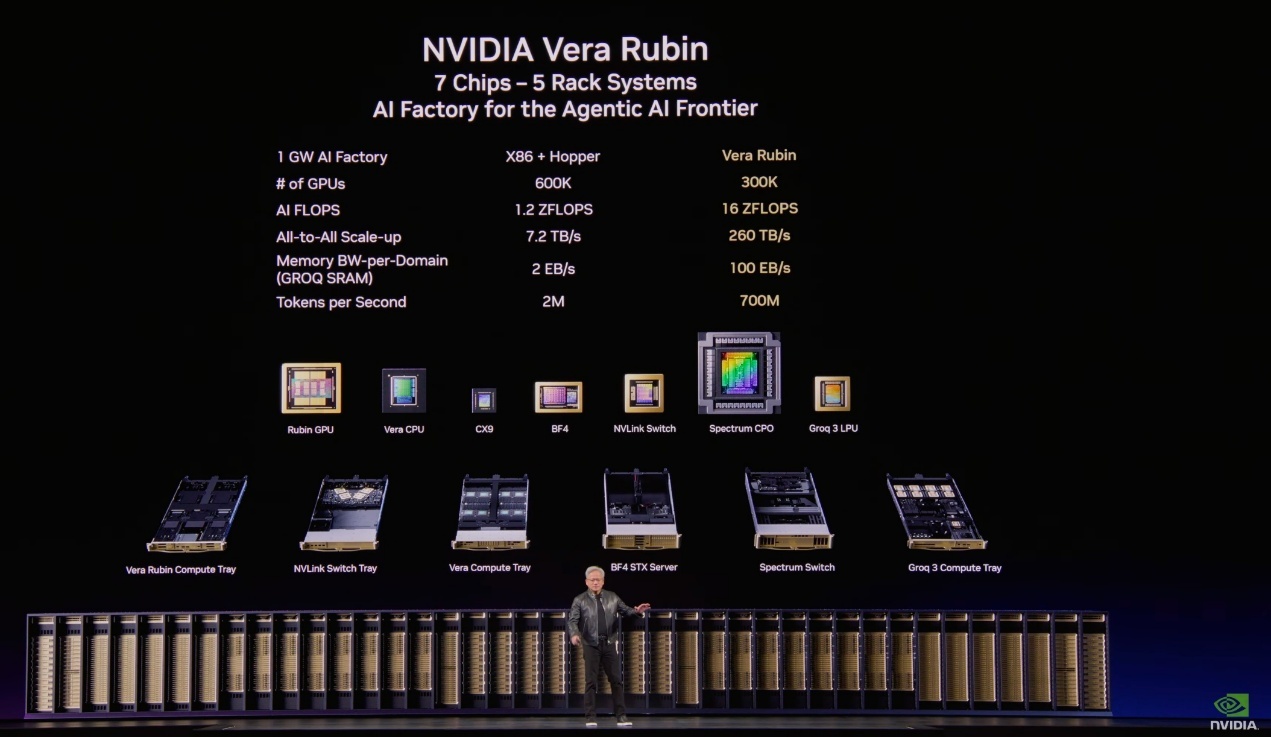

That said, hyperscaler capex keeps moving higher and NVIDIA's AI chip share is still rising. In the Vera Rubin stack, NVIDIA also outlined a more Agentic-oriented compute design:

a) An in-house Inference Context Memory System (ICMS) to mitigate the 'memory wall';

b) Introducing Groq 3 LPU to accelerate the decode stage;

c) Using the in-house Vera CPU for task orchestration to improve efficiency.

However, NVIDIA's monopoly premium is gradually fading as models split into training and inference: NVIDIA still has a clear edge in training. Post-training, inference repeatedly runs the same computations and is more sensitive to token throughput, latency and cost, making it the prime target for in-house chips.

As inference evolves from chatbots to Agentic workflows, the raw compute bottleneck eases. Memory, CPUs and related assets are becoming the more pressing constraints.

In other words, NVIDIA's products and system-level solutions remain a step function ahead, but the bottlenecks now center on memory, CPU, interconnects and cost-performance. As cloud vendors have viable 'plan B' options for inference, the moat and pricing power that were unrivaled in the training era have weakened.

Even so, with industry beta plus Blackwell volume, NVIDIA is clearly in an earnings harvest period. The stock should track Blackwell shipments and, into 2H, Vera Rubin which is more tuned for inference.

At the current market cap (~$5.4tn), the stock implies roughly 18x PE on FY28 net income, given Jensen's Data Center outlook and relatively visible high growth for FY26-28. This assumes a two-year revenue CAGR of ~60%, GPM of 74% and a 17% tax rate.

After the last print, Dolphin Research set a $175-240 target range, and the recent high near $236 is close to the top end. If Vera Rubin shipments beat, the stock could clear $250. But a repeat of the valuation-and-earnings 'double play' of the past two years looks tougher, and in 2026 EPS alone may need to carry the stock.

See below for Dolphin Research's detailed take on NVIDIA's results.

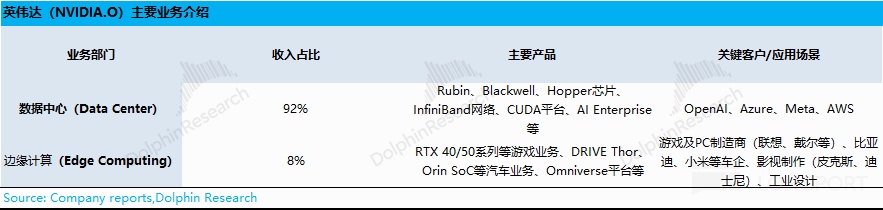

I. Business overview

With Data Center still surging, it now accounts for over 90% of revenue. The company reorganized reporting this quarter, rolling gaming, auto and other units into the new 'Edge' segment with no separate disclosures.

By business line:

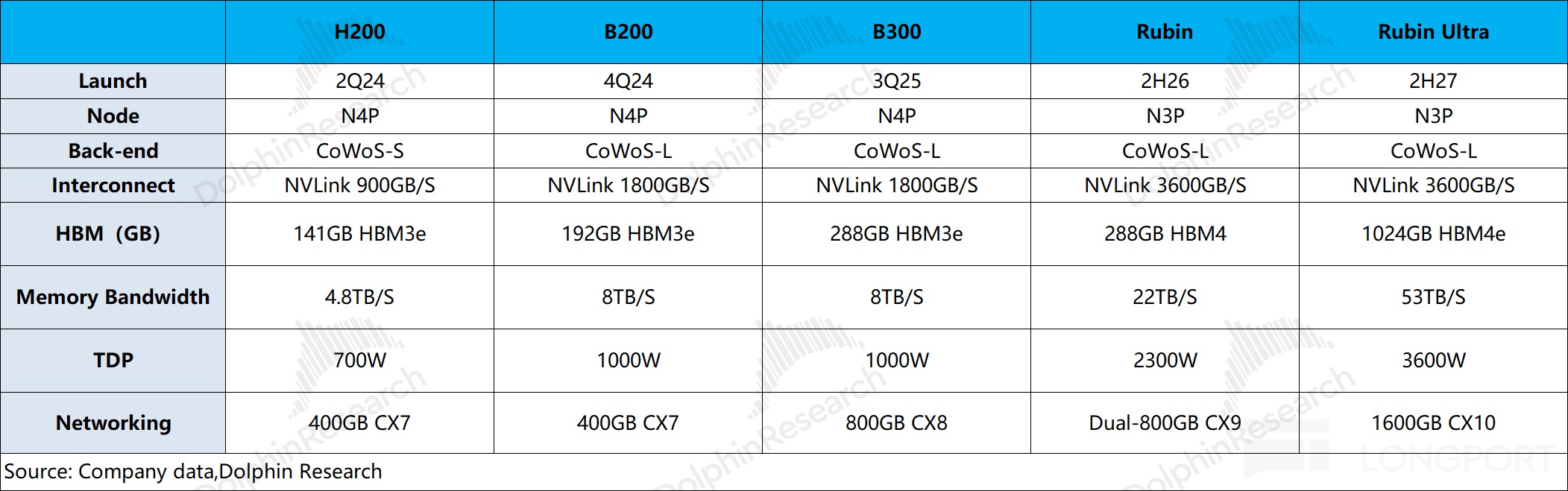

1) Data Center: This is the core focus, spanning Blackwell accelerators, InfiniBand and more, with key customers including Amazon, Microsoft and Google. The segment is in the Blackwell cycle, with B300/GB300 as workhorses, and will transition to Rubin as volume starts in 2H26.

2) Edge computing: Includes PCs, consoles, workstations, AI-RAN base stations, robotics and auto, with no further sub-segment disclosure. Within Edge, gaming is the largest sub-segment.

The current gaming portfolio centers on RTX 40 and RTX 50, with gamers and PC OEMs as primary customers.

II. Headline metrics: Modest beat vs. expectations

2.1 Revenue: FY27 Q1 (1Q26) revenue was $81.6bn, +85% YoY and above the raised buy-side range ($78-80bn). The $13.5bn QoQ uplift was almost entirely from Data Center as Blackwell scaled.

For next quarter, the company guided revenue to $91.0bn, up $9.4bn QoQ and above the raised buy-side view (~$89.0bn). Growth will still be led by B300/GB300, with Rubin entering volume in FQ3 (calendar 3Q26).

2.2 GPM (GAAP): FY27 Q1 GPM (GAAP) was 74.9%, broadly in line with the 75% market view. The sharp dip a year ago largely reflected the H20 restriction.

For next quarter, GAAP GPM is guided to 74.9%, flat QoQ and in line with the street (~74.8%). As Blackwell ramps, GPM has returned to ~75%.

Management previously indicated a 75% GPM target for FY27. That provides some confidence, but investors still worry about post-FY27 margin compression risk.

III. Business progress: Non-megacap cloud led the incremental growth

Powered by AI capex, Data Center (Compute + Networking) now exceeds 90% of total revenue. Other businesses have been compressed to below 10%, consolidated under Edge this quarter without separate disclosure.

3.1 Data Center: FY27 Q1 Data Center revenue was $75.2bn, +92% YoY. It remains the key focus, with growth driven by Blackwell volume, propelled by accelerated computing and AI demand.

By sub-line, Compute was roughly $60.0bn this quarter, up ~$8.7bn QoQ, with B300 shipments the main driver. Networking was about $15.1bn, up ~$4.2bn QoQ.

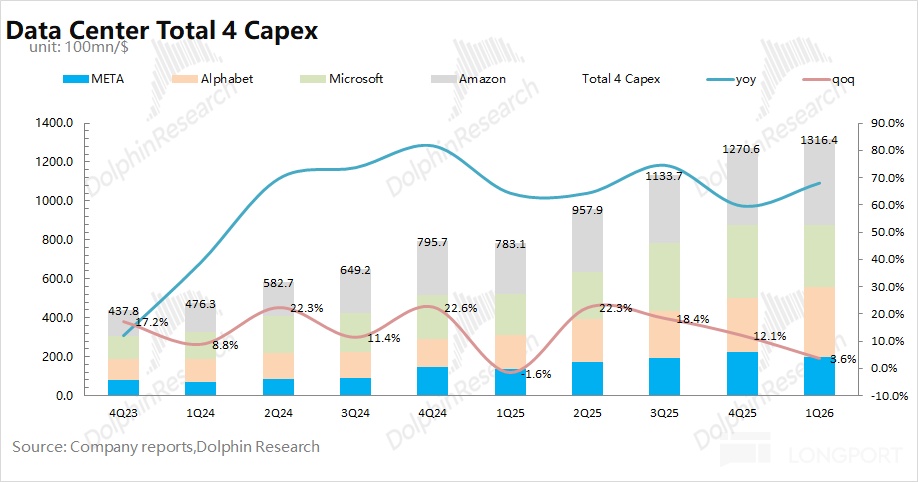

Cloud providers remain the largest buyers of AI silicon, making their capex the foundation of NVIDIA's Data Center growth. Based on commentary from Google, Meta, Microsoft and Amazon, Dolphin Research expects 2026 capex across the four to top $700bn, up nearly 80% YoY. That underpins high-growth visibility into FY27.

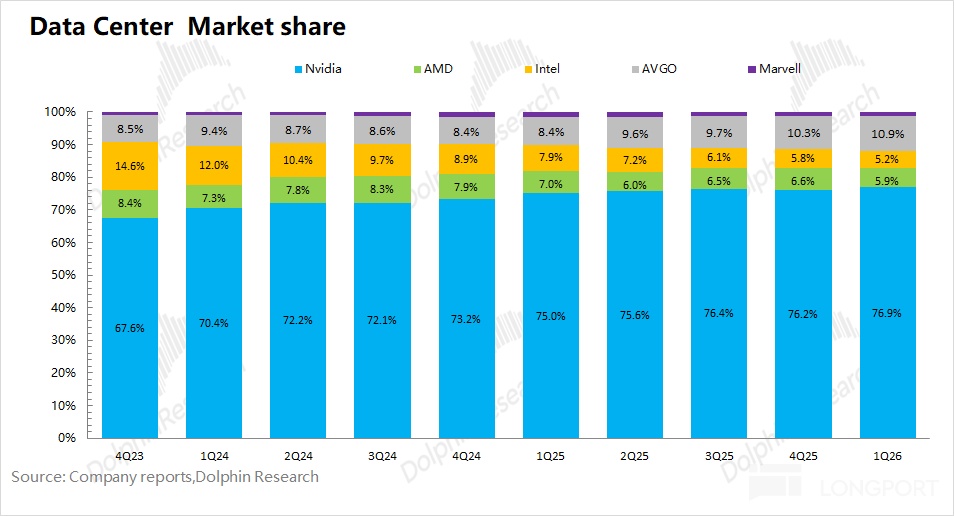

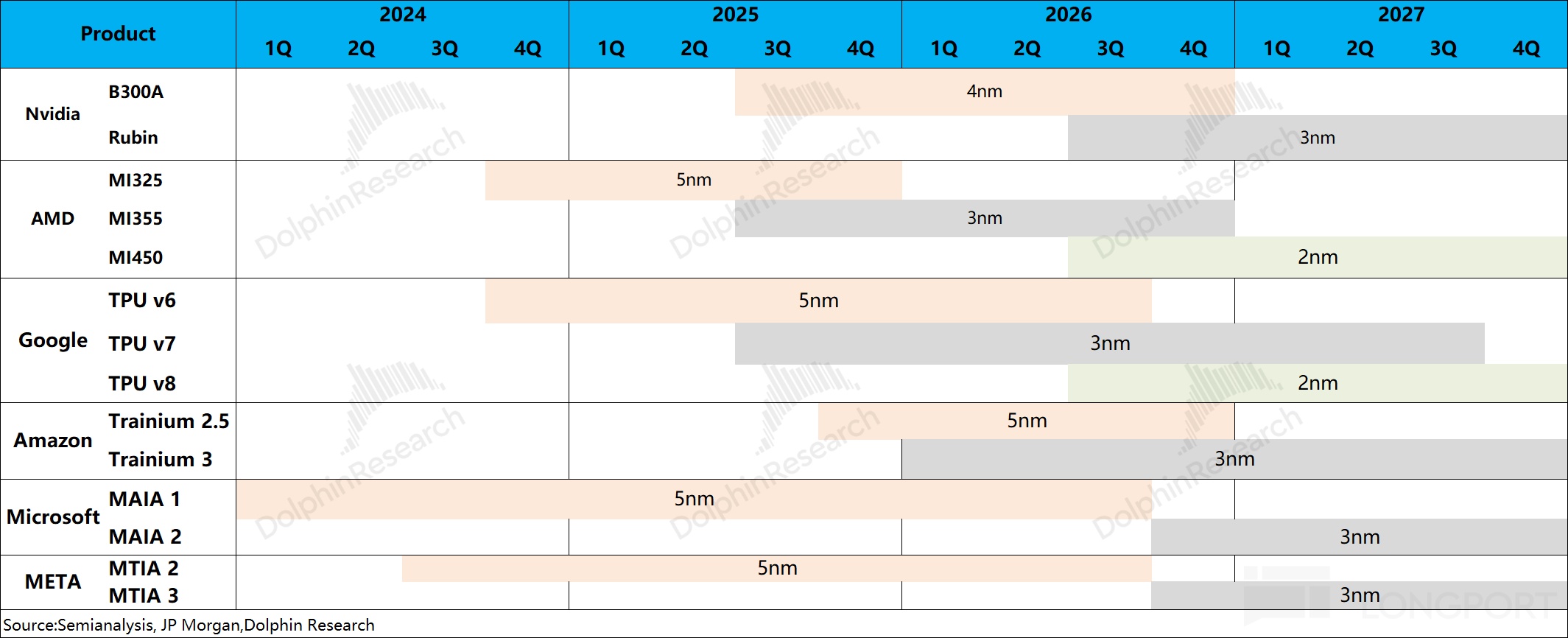

Beyond capex, competition from in-house ASICs is the bigger watch item. The core players today are NVIDIA, 'Google + Broadcom' and AMD, together holding over 90% share. Given the train-vs-infer split, NVIDIA's GPU advantage is clear in training, but inference can accept lower peak performance, making Google TPU and other in-house parts more cost-effective.

NVIDIA's high upstream margins capture a large portion of industry profits, pressuring downstream unit economics. In inference, dependence on NVIDIA drops significantly, motivating large players to develop in-house chips or adopt ASIC alternatives.

Against that backdrop, NVIDIA changed its disclosure to underscore growth in industrial and enterprise cloud.

By customer group, hyperscalers delivered $37.9bn this quarter (+$4.0bn QoQ), while other cloud was $37.4bn (+$8.9bn QoQ), representing the largest incremental contribution.

Over the past two quarters, even as megacaps push in-house silicon, growth outside the megacaps—namely enterprise and industrial cloud—has clearly accelerated. Management aims to demonstrate sustained growth capability.

GPM is back near 75%, but share loss down the road could pose a 'potential headwind' to margins. Management explicitly targeted ~75% for FY27, but mainstream models still bake in GPM declines into FY28 and beyond.

3.2 Edge computing: FY27 Q1 Edge revenue was $6.4bn, +29% YoY, mainly on higher RTX 50 series shipments in gaming. With Data Center now >90% mix, other businesses are less material.

NVIDIA has therefore grouped them as 'Edge' without separate disclosure. Within Edge, gaming is the largest, at roughly 60-70% of segment revenue.

Despite a subdued PC and console market, NVIDIA retains a clear lead in gaming GPUs vs. peers. For reference, AMD's gaming revenue was ~$720mn last quarter.

IV. Key financials: Margin expansion on rapid growth

4.1 Core OPM

FY27 Q1 core OPM was 65.6%, continuing to edge up, driven by lower opex as a percentage of revenue. Breaking down core OPM:

'Core OPM = GPM - R&D ratio - S&M and G&A ratio'

1) GPM: 74.9% this quarter, down 10bps QoQ and holding near 75%. 2) R&D ratio: 7.7% this quarter. While absolute R&D rose by ~$800mn QoQ, the ratio fell on faster revenue growth.

3) S&M and G&A ratio: In the Blackwell cycle, S&M and G&A remained relatively stable. The ratio fell to 1.6% this quarter.

Management guided next-quarter opex to $8.5bn. On the revenue guide, the opex ratio should hold around ~9.3%.

4.2 Core OP

FY27 Q1 net income was $58.3bn, up 71% YoY. Given the impact of non-operating items, we focus on core OP (GP - R&D - S&M/G&A), which was $53.5bn, +147% YoY.

Core OPM rose to 65.6%, driven by revenue growth and margin recovery (vs. last year's H20-related dip). Current growth is powered by the Blackwell cycle.

With the previously outlined Data Center outlook and Rubin entering volume from FQ3, we expect high growth to persist through FY27-28.

Historical Dolphin Research notes on NVIDIA:

Hot topics

Mar 18, 2026 post-GTC small-meeting recap: NVIDIA (Analyst small meeting): IT will become a token distributor, 50% of FCF for shareholder returns

Mar 17, 2026 GTC minutes: NVIDIA (GTC minutes): LPU reshapes AI inference, compute factories head to space

Mar 17, 2026 GTC conference: NVIDIA GTC: AI's Spring Gala, high hopes and mixed feelings?

Jan 7, 2026 CES keynote: Jensen unveils Rubin, stoking the AI storage fire

Dec 7, 2025 trade controls: H200 cleared: the 'arrow through the clouds' for NVIDIA's $6tn path?

Oct 29, 2025 GTC: GTC: 'Bomb' shipment next year, is the sky the limit for NVIDIA?

Sep 10, 2025 CPX launch: NVIDIA: Rubin CPX debuts, squaring off with Broadcom ASICs

Sep 1, 2025 small meeting: NVIDIA (small meeting): Cautious on 2026 targets, $3-4tn market by 2030

Earnings season

Feb 26, 2026 call minutes: NVIDIA (minutes): Compute spend ties directly to revenue, supply chain security first

Feb 26, 2026 earnings take: NVIDIA: Earnings frenzy vs. a cold stock, is the No.1 stock losing its shine?

Nov 20, 2025 call minutes: NVIDIA (minutes): Targeting 75% GPM next year, OpenAI partnership not blind

Nov 20, 2025 earnings take: More important than NFP? Can NVIDIA save U.S. stocks again?

Aug 28, 2025 call minutes: NVIDIA (minutes): GB300 already shipping, Rubin on track for mass production next year

Aug 28, 2025 earnings take: NVIDIA: The No.1 stock in the universe, is 'not explosive' a sin?

May 29, 2025 call minutes: NVIDIA (minutes): China shipment mix unchanged

May 29, 2025 earnings take: NVIDIA: Don't doubt it, still the No.1 stock in the universe!

Feb 27, 2025 call minutes: NVIDIA (minutes): China shipment mix unchanged

Feb 27, 2025 earnings take: NVIDIA: Did DeepSeek pierce Jensen's 'leather jacket'?

Risk disclosure and statement: Dolphin Research disclaimer and general disclosure

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.