China Apr retail sales: Q2 under pressure?

As Dolphin Research cautioned earlier, consumption will be under pressure in Q2. April retail sales confirmed the slowdown, with total retail up just 0.2% YoY and online physical goods growth also at 0.2% by our estimate, the weakest month since 2022.

That said, this weak print was not a bomb out of the blue. After the Feb peak season, March momentum had already faded, last Mar–Jun saw the most pronounced tailwind from state subsidies, and leading platforms such as JD have guided that Q2 e-commerce growth will deteriorate noticeably vs. Q1.

The main drags remain electrified durables and autos. There are signs of spillover to other product categories and consumption types.

1) Apr Retail Tanked — Not a Surprise, But Where Is the Problem?

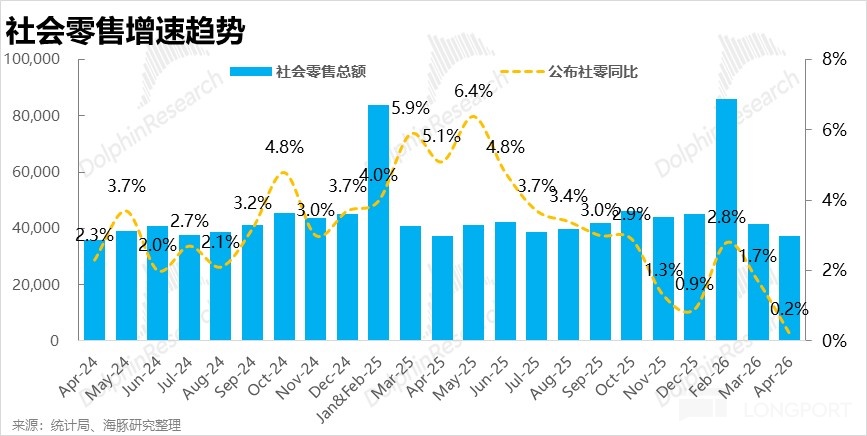

According to the National Bureau of Statistics, total retail sales in Apr rose 0.2% YoY. This marked a step-down from 2.8% in Feb and 1.7% in Mar, while history shows last Mar–May was a growth peak aligned with the height of state-subsidy support.

Hence, YoY pressure on consumption and online shopping is likely to stay heavy in Q2. The base eases meaningfully in H2, when retail and consumption growth should bottom and start to recover.

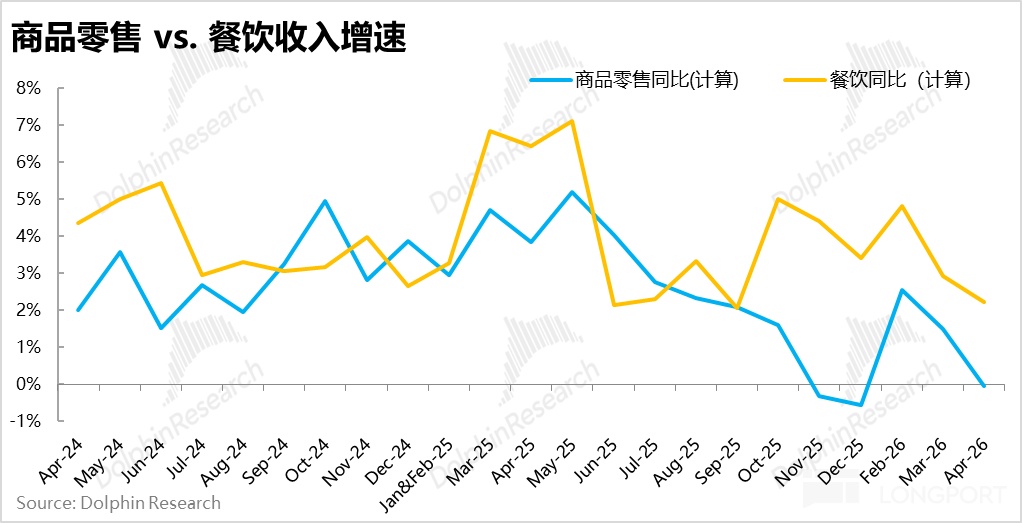

By consumption type, both goods retail and F&B growth slowed MoM in Apr, with goods weaker. Specifically, goods retail growth was just 0.2% vs. 1.5% in Mar, while F&B revenue growth eased from 2.9% to 2.2%.

On this divergence, we think F&B is less affected by the fade of state subsidies and broad electronics price hikes, thus better reflecting underlying demand. This implies overall consumption in Apr did soften vs. Mar. Goods retail, however, was more structurally dragged by home appliances, furniture, and autos.

2) Online Spending Under Greater Pressure

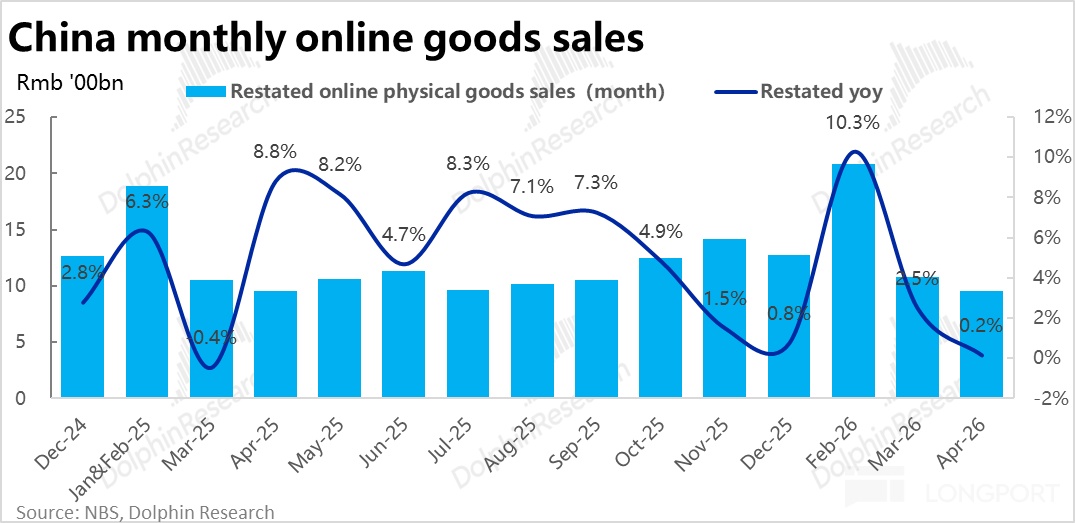

Since 2026, the NBS has revised the scope for online retail, shifting from online retail sales to online goods & services retail and significantly expanding coverage of services sold online. That said, the methodology for online physical goods remains largely unchanged and is comparable with history.

In Apr, online physical goods retail rose only 0.2% YoY, plunging from the weighted avg. growth of 6.5% in Dec–Feb and well below Mar’s 2.5%. This shows online spending is taking a bigger hit than overall retail.

Similarly, JD guided next-quarter e-commerce revenue growth to worsen from nearly +5% this quarter to about -5% in Q2. Leading platforms thus also see heavy pressure on online consumption in Q2.

By contrast, online services sales were more resilient, with Apr YoY growth at ~6.8%. Although MoM growth also slowed, the absolute pace remained solid.

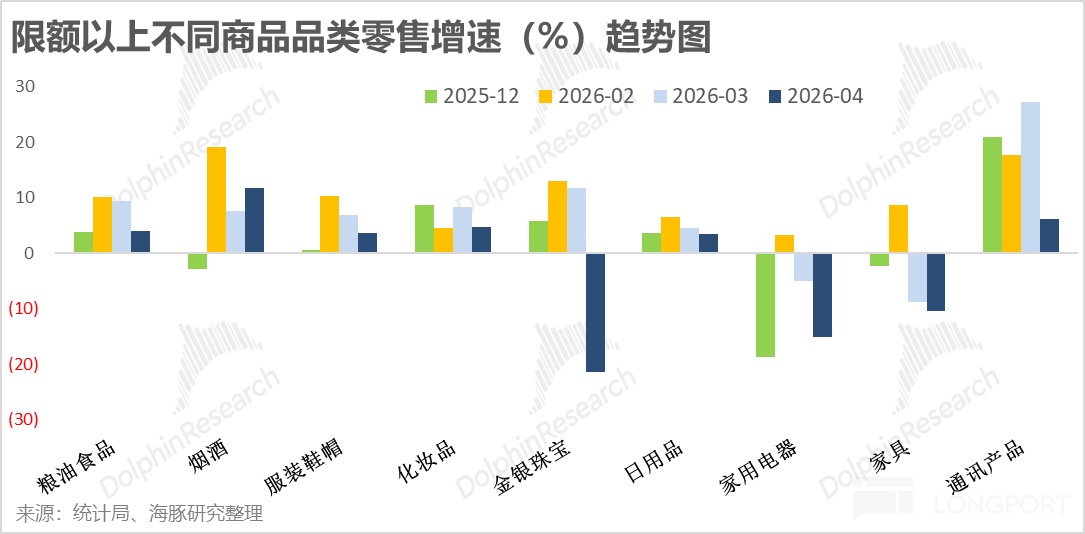

3) Autos and Subsidy-Linked Categories Still the Biggest Drags, With Spillover Signs

By category, autos remained a major drag, with Apr auto retail down nearly 20% YoY. Ex-autos, retail sales growth was 2.2%, much stronger than the headline 0.2%.

Among other goods, home appliances and furniture—earlier beneficiaries of subsidies—were among the worst performers, with above-scale sales down ~15% and ~10% in Apr, respectively. Two more points stand out: as gold prices peaked and pulled back, jewelry sales plunged about 20% YoY; and telecom equipment (e.g., smartphones) is increasingly pressured, likely as memory price hikes begin to curb demand.

In addition, categories less directly affected by subsidies—apparel & footwear, cosmetics, and daily necessities—also weakened MoM this month. Discretionary saw a larger pullback, with apparel and cosmetics growth down roughly 3–4 ppts MoM. This suggests weakness is spreading beyond subsidy-linked categories.

Risk disclosure and statement: Dolphin Research Disclaimer and General Disclosure

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.