Got $3,000? 2 AI Stocks Wall Street Analysts Say Could Double From Here.

Key Points

SentinelOne designed its security platform around artificial intelligence (AI) from the beginning.

The deep uncertainties about Adobe are more than priced into the stock.

Artificial intelligence (AI) stocks have sold off in recent months. Elevated valuations and staggering capital expenditures (capex) spending have spooked some investors.

Fortunately, that means many of these stocks trade at a significant discount from their highs. Since AI growth is on track to continue, rising revenues and lower valuations could put these AI stocks on track to double.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

1. SentinelOne

At first glance, SentinelOne (NYSE: S) does not look like a stock headed higher. It cratered in 2022 after a massive run-up during the pandemic and has traded in a range since that time. Moreover, the company continues to report net losses, and other names in the industry, such as CrowdStrike and Palo Alto Networks, overshadow it.

Still, despite the competition, SentinelOne should stand out for many reasons. For one, it built its platform around AI from inception. That allows it to detect threats and respond on a local device. Additionally, it also has the advantage of working when offline and can revert systems, registry keys, and files to a pre-infection state with one click.

SentinelOne also continues to grow despite these concerns. In fiscal 2026 (ended Jan. 31), revenue of $1 billion rose by 22% yearly, and it is on track for another 20% increase in fiscal 2027.

Still, the company generated around $52 million in free cash flow, meaning it will not have to dilute shareholders to raise cash.

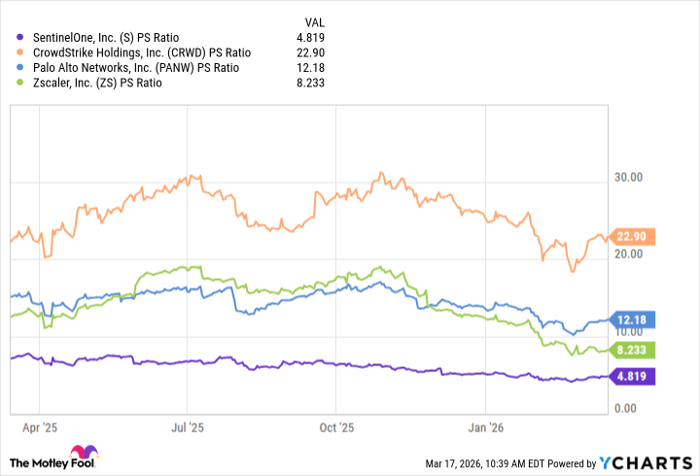

Furthermore, while the lack of profits leaves it without a P/E ratio, the price-to-sales (P/S) ratio of 5 is far below competitors like CrowdStrike, Palo Alto, and Zscaler.

S PS Ratio data by YCharts

As of this writing, investors can buy 99 shares for around $1,450, and if those shares doubled in value, it would be a cheaper stock than most of its competitors.

2. Adobe

The first half of the 2020s could be described as lost years for Adobe (NASDAQ: ADBE). The stock sold off in 2022 along with most tech stocks. While a run-up in 2023 offered hope, the stock again sold off in 2024 amid rising competition and an increased perception that AI would disrupt its business. With that, CEO Shantanu Narayen stepped down without naming a replacement.

With all of that uncertainty, a sell-off is understandable. Nonetheless, investors seem to have also ignored the stock's solid financial metrics.

Adobe's revenue for the first quarter of fiscal 2026 (ended Feb. 27) was $6.4 billion. That was a 12% yearly increase and close to the 11% growth rate for fiscal 2025. Also, the only reason its $1.9 billion in net income grew by 4% was a massive spike in income tax expenses.

Indeed, the 9% revenue growth forecast for fiscal 2027 may be a slight disappointment. However, the relentless selling in the stock has taken its P/E ratio to 15 and forward P/E to 11.

That is arguably too low given its growth, and as conditions stand now, one can buy six shares for around $1,550. Under current conditions, that amount could double on any good news or simply if the beaten-down software stock stays the course for the foreseeable future.

Should you buy stock in SentinelOne right now?

Before you buy stock in SentinelOne, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SentinelOne wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $510,710!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,105,949!*

Now, it’s worth noting Stock Advisor’s total average return is 927% — a market-crushing outperformance compared to 186% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of March 20, 2026.

Will Healy has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe, CrowdStrike, SentinelOne, and Zscaler. The Motley Fool recommends Palo Alto Networks and recommends the following options: long January 2028 $330 calls on Adobe and short January 2028 $340 calls on Adobe. The Motley Fool has a disclosure policy.