Booking Holdings Inc Stock (BKNG) Moved Up by 6.46% on Mar 5: What Investors Need To Know

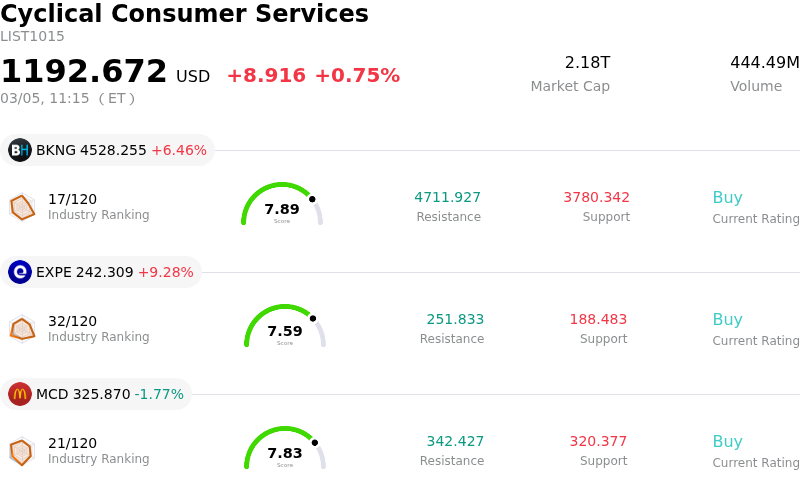

Booking Holdings Inc (BKNG) moved up by 6.46%. The Cyclical Consumer Services sector is up by 0.75%. The company outperformed the industry. Top 3 stocks by trading volume in the sector: Booking Holdings Inc (BKNG) up 6.46%; Expedia Group Inc (EXPE) up 9.28%; McDonald's Corp (MCD) down 1.77%.

What is driving Booking Holdings Inc (BKNG)’s stock price up today?

Booking Holdings (BKNG) experienced significant upward movement, demonstrating notable intraday volatility. This positive performance appears to be driven by a confluence of strong financial results, strategic corporate actions, and an optimistic outlook on both the company's future and the broader travel industry.

The company's fourth quarter and full year 2025 financial results, released on February 18, 2026, exceeded analyst expectations for both earnings per share and revenue. Booking Holdings reported an increase in quarterly revenue year-over-year and surpassed consensus estimates. Furthermore, the company provided positive guidance, projecting continued top-line and earnings per share growth for 2026, a forecast reinforced during its presentation at the Morgan Stanley Technology, Media & Telecom Conference 2026.

Adding to the positive sentiment, Booking Holdings announced an increase in its quarterly dividend, signaling robust financial health and a commitment to returning value to shareholders. The company also approved a substantial stock split, effective in early April 2026. While a stock split is primarily a structural adjustment, it often acts as a psychological catalyst, potentially increasing market liquidity and attracting a broader base of investors.

Analyst sentiment remains largely positive, with multiple brokerage firms, including BTIG Research, reiterating "Buy" ratings and providing price targets that suggest further potential upside. The consensus among analysts is a "Moderate Buy" for the stock. Moreover, the company's recent collaboration with OpenAI to enhance travel planning through ChatGPT has been viewed favorably, with industry experts noting that online travel agencies like Booking Holdings are well-positioned to leverage artificial intelligence for future growth rather than be disrupted by it.

The overall outlook for the travel industry also contributes to investor confidence. Recent data for early 2026 indicated an increase in total air passenger demand, with a particularly strong rise in international travel. Projections for falling average airfares are anticipated to further encourage travel throughout the year, suggesting a robust environment for Booking Holdings.

Technical Analysis of Booking Holdings Inc (BKNG)

Technically, Booking Holdings Inc (BKNG) shows a MACD (12,26,9) value of [-229.39], indicating a neutral signal. The RSI at 43.66 suggests neutral condition and the Williams %R at -21.21 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Booking Holdings Inc (BKNG)

Booking Holdings Inc (BKNG) is in the Cyclical Consumer Services industry. Its latest annual revenue is $26.92B, ranking 2 in the industry. The net profit is $5.40B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $5842.76, a high of $7746.00, and a low of $4495.00.

More details about Booking Holdings Inc (BKNG)

Company Specific Risks:

- A proposed €530 million fine from the Spanish competition authority poses a significant legal and financial liability, having already contributed to a $276 million loss in 2023 and reduced Q4 net income.

- Ongoing analyst and investor concerns persist regarding the potential for Artificial Intelligence to disintermediate online travel agencies, which could lead to consumers bypassing traditional booking platforms and subsequently squeezing profit margins.

- Investor apprehension stems from decelerating room night growth projections for Q1 and a significant planned reinvestment for 2026, indicating a potential slowdown in core business expansion and more modest future margin expansion.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.