American International Group Inc Stock Moved Down by 3.02% on Mar 3: Drivers Behind the Movement

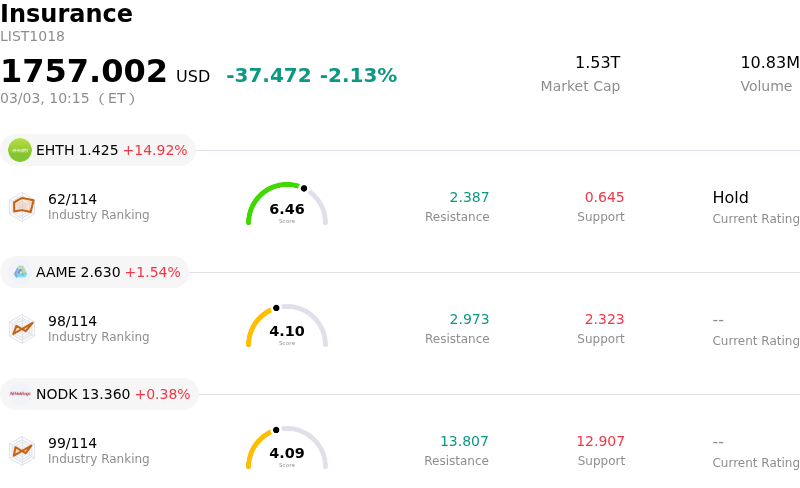

American International Group Inc (AIG) moved down by 3.02%. The Insurance industry is down by 2.13%. The company underperformed the industry. Top 3 gainers of the industry: eHealth Inc (EHTH) up 14.92%; Atlantic American Corp (AAME) up 1.54%; NI Holdings Inc (NODK) up 0.38%.

AIG’s stock performance today, reflecting a downward movement, can be attributed to a combination of company-specific financial results, prevailing industry dynamics, and broader macroeconomic factors.

While American International Group recently reported a strong increase in its fourth-quarter 2025 adjusted after-tax income per diluted share, surpassing analyst estimates, the company also reported a miss on its revenue expectations for the quarter. This divergence, where earnings beat but revenue fell short, can sometimes lead to investor concern regarding the underlying growth trajectory, particularly when paired with a noted contraction in North American retail property and personal net premiums due to reduced market appetite and higher reinsurance costs.

Further contributing to a cautious sentiment are significant pressures facing the broader insurance sector. Reports released today highlight the industry’s struggles with increasing climate risks and shrinking margins. The challenges for insurers are also compounded by global financial pressures and the evolving demands of risk management in areas such as climate change. Geopolitical tensions, specifically the widening conflict in the Middle East, have led to insurance companies canceling war risk coverage for vessels, indicating heightened operational risks for the sector.

Macroeconomic conditions also play a role, as US Treasury yields have been rising on the back of inflation concerns. This increase in yields is partly fueled by escalating geopolitical conflicts pushing energy prices higher, which in turn has prompted markets to temper expectations for Federal Reserve rate cuts. A general environment of rising interest rates and inflation worries can weigh on equity valuations across various sectors, including financials like AIG.

Additionally, recent institutional investor activity shows some firms reducing their positions in AIG during the previous quarter, which can signal shifting sentiment among large holders. Analyst ratings currently reflect a "Hold" consensus for AIG, suggesting that while the company has positive aspects such as improved underwriting and share repurchase plans, there are also areas of concern, including a forecast for earnings growth that is slower than the broader US market.

Technically, American International Group Inc (AIG) shows a MACD (12,26,9) value of [0.78], indicating a buy signal. The RSI at 65.12 suggests neutral condition and the Williams %R at -7.08 suggests oversold condition. Please monitor closely.

American International Group Inc (AIG) is in the Insurance industry. Its latest annual revenue is 26.77B, ranking 11 in the industry. The net profit is 3.10B, ranking 14 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as HOLD, with an average price target of 87.53, a high of 101.00, and a low of 79.00.

Company Specific Risks:

- AIG unit Lexington Insurance Co. is facing a lawsuit filed March 3, 2026, seeking over $55 million for alleged failure to reimburse abuse claims, potentially impacting legal expenses and claim reserves.

- Institutional analysts express concerns regarding anticipated slower premium growth and higher core loss and expense ratios within AIG's Global Personal Lines business, alongside expected poor underwriting results in its Convex and recently acquired EG business segments.

- AIG's absorption of renewal rights for 30-40% of Everest Group's insurance business, announced March 2, 2026, introduces potential operational and underwriting challenges, especially if it includes previously less-profitable lines.

- The ongoing CEO transition, with Eric Andersen having joined as CEO-elect in mid-February 2026, presents execution risk, as any deviation from established underwriting standards could negatively impact the company's valuation.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.