ASML Holding NV Stock Moved Down by 4.56% on Feb 26: What Investors Need To Know

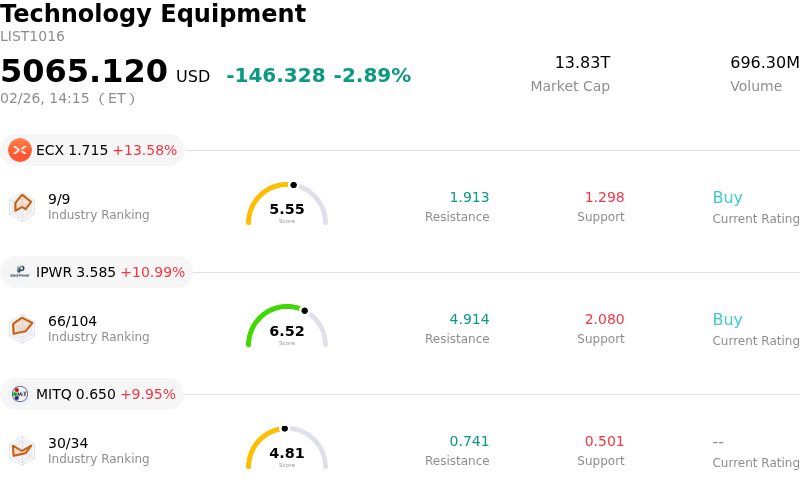

ASML Holding NV (ASML) moved down by 4.56%. The Technology Equipment industry is down by 2.89%. The company underperformed the industry. Top 3 gainers of the industry: Ecarx Holdings Inc. (ECX) up 13.58%; Ideal Power Inc (IPWR) up 10.99%; Moving Image Technologies Inc (MITQ) up 9.95%.

ASML Holding NV experienced significant intraday volatility, with its stock declining. This movement appears to be primarily driven by a reassessment of the company's 2026 outlook by investors, particularly concerning its China-related revenue and overall chip-tool demand, following a strong recent performance.

Management has indicated that China's share of sales is anticipated to decrease to approximately 20% of total revenue in 2026, a notable reduction from an unusually high contribution in 2025. This expected normalization under export-control constraints is putting pressure on near-term growth assumptions. The semiconductor industry is also experiencing broader sentiment shifts, with some investors perceiving the sector as overbought after a significant surge. This has led to profit-taking, especially given that ASML's stock had doubled over the last six months, despite not benefiting from the AI boom as directly as some other chip companies.

Analyst forecasts have also played a role. While some analysts maintain "Buy" or "Outperform" ratings, reflecting confidence in long-term growth driven by AI demand and recent technological breakthroughs in EUV lithography, there have been recent downgrades and concerns about ASML's valuation. For instance, some analysts have downgraded the stock to "Hold" due to valuation concerns after a substantial rally. Additionally, there are worries about potential declines in 2026 revenue and earnings per share, with some forecasts falling below consensus expectations. The company's average brokerage recommendation is "Outperform," but its estimated fair value by some analyses suggests a potential downside from its current trading price.

Furthermore, institutional investors have made adjustments to their portfolios. Some funds have trimmed their holdings in ASML during recent quarters. This collective movement by institutional players can contribute to short-term price fluctuations. While there are positive developments, such as SK Hynix's significant investment in semiconductor plants and Broadcom shipping advanced AI chips, these broader industry trends may not have immediately offset the specific concerns weighing on ASML's near-term revenue outlook and valuation.

Technically, ASML Holding NV (ASML) shows a MACD (12,26,9) value of [50.98], indicating a buy signal. The RSI at 69.74 suggests neutral condition and the Williams %R at -9.10 suggests oversold condition. Please monitor closely.

ASML Holding NV (ASML) is in the Technology Equipment industry. Its latest annual revenue is 36.83B, ranking 7 in the industry. The net profit is 10.83B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 1358.60, a high of 1868.00, and a low of 935.00.

Company Specific Risks:

- Reduced revenue contribution from China is anticipated in 2026 due to evolving export control regulations and the normalization of prior backlog-driven shipments, which has recently led to a significant stock price drop.

- ASML's 2026 guidance indicates potential gross margin compression to 51%-53%, reflecting a less favorable product mix, including older EUV units and lower-margin dry DUV systems, alongside the introduction of new High-NA EUV machines that will carry lower initial margins.

- The company's elevated valuation, with a trailing P/E ratio of 50.99 and a price-to-sales ratio significantly higher than the sector average, exposes the stock to amplified downside risk should growth expectations soften or market sentiment shift.

- Competitive pressure from semiconductor equipment peers is evident, with some analysts noting that Lam Research, for example, shows a stronger long-term growth profile in revenue and EPS estimates compared to ASML.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.