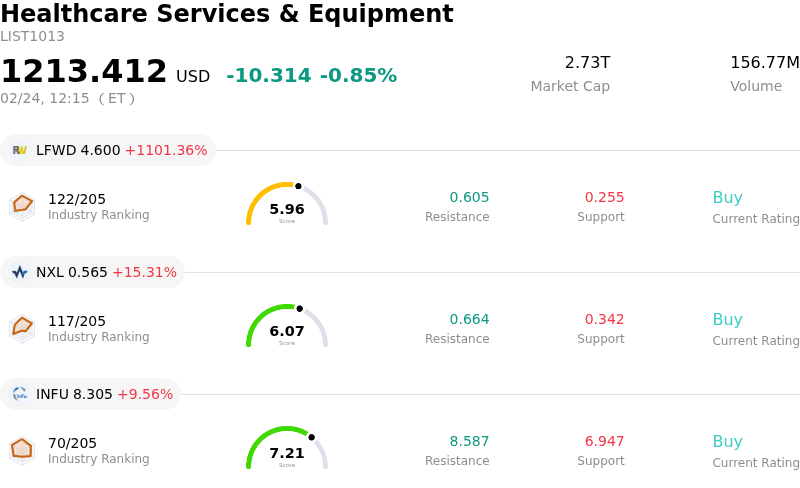

Elevance Health Inc Stock Moved Down by 3.53% on Feb 24: A Full Analysis

Elevance Health Inc (ELV) moved down by 3.53%. The Healthcare Services & Equipment industry is down by 0.85%. The company underperformed the industry. Top 3 gainers of the industry: Lifeward Ltd (LFWD) up 1101.36%; Nexalin Technology Inc (NXL) up 15.31%; InfuSystem Holdings Inc (INFU) up 9.56%.

Elevance Health (ELV) experienced a downward movement today, reflecting continued market digestion of its challenging financial outlook for 2026 and prevailing industry headwinds. The company's fourth-quarter 2025 earnings call on January 28, 2026, outlined a projected decline in both GAAP and adjusted diluted earnings per share for fiscal year 2026 compared to 2025. This guidance also indicated an expected decrease in total operating revenue for 2026.

A primary factor contributing to this cautious outlook is the anticipated reduction in risk-based membership, particularly within the Medicaid and Medicare Advantage segments. Elevance Health expects a low double-digit percentage decline in risk-based membership, including a significant decrease in Medicare Advantage enrollment and a fall in Medicaid membership due to ongoing eligibility reverification processes. Furthermore, the company foresees a negative Medicaid operating margin for 2026 as rate trends lag behind elevated utilization.

The broader healthcare insurance industry is also grappling with financial pressures, including rising costs and shrinking reimbursements, which contribute to a deteriorating outlook for the sector as noted by credit ratings agencies. The deceleration of Medicare Advantage growth industry-wide, with many large insurers shedding members, reinforces the challenges faced by companies like Elevance. Concerns regarding medical cost trends, particularly in Affordable Care Act plans and Medicare Part D seasonality, continue to weigh on the sector. Regulatory uncertainty surrounding healthcare affordability and potential changes to federal subsidies further adds to the complex operating environment for health insurers.

While some analyst ratings remain positive with "Buy" or "Moderate Buy" recommendations, their forecasts have been influenced by the revised 2026 earnings per share estimates, which factor in lower Medicaid margins and overall pressures from medical cost control. The current intraday volatility likely represents the market's ongoing recalibration of Elevance Health's valuation in light of these persistent operational challenges and revised financial expectations.

Technically, Elevance Health Inc (ELV) shows a MACD (12,26,9) value of [-4.12], indicating a neutral signal. The RSI at 44.13 suggests neutral condition and the Williams %R at -56.20 suggests oversold condition. Please monitor closely.

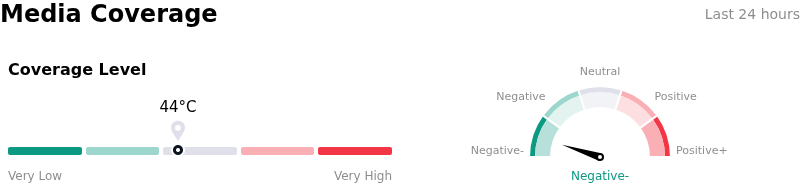

In terms of media coverage, Elevance Health Inc (ELV) shows a coverage score of 44.36, indicating a moderate level of media attention, with extremely bearish sentiment.

Elevance Health Inc (ELV) is in the Healthcare Services & Equipment industry. Its latest annual revenue is 199.12B, ranking 4 in the industry. The net profit is 5.66B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 391.59, a high of 491.45, and a low of 332.00.

Company Specific Risks:

- Elevance Health's reported Q4 2025 revenue of $49.31 billion slightly missed analyst expectations of $49.82 billion, indicating recent top-line underperformance.

- RBC Capital downgraded Elevance Health on February 3, 2026, from Outperform to Sector Perform, citing a "softer than expected 2026 guide and go-forward margin outlook" that presents incremental risk to the company's long-term earnings per share targets.

- A federal judge's rejection of Elevance Health's challenge to U.S. Medicare star ratings in August 2025, which the company stated could cost at least $375 million in bonus payments, highlights ongoing regulatory and financial vulnerability within its Medicare Advantage plans.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.