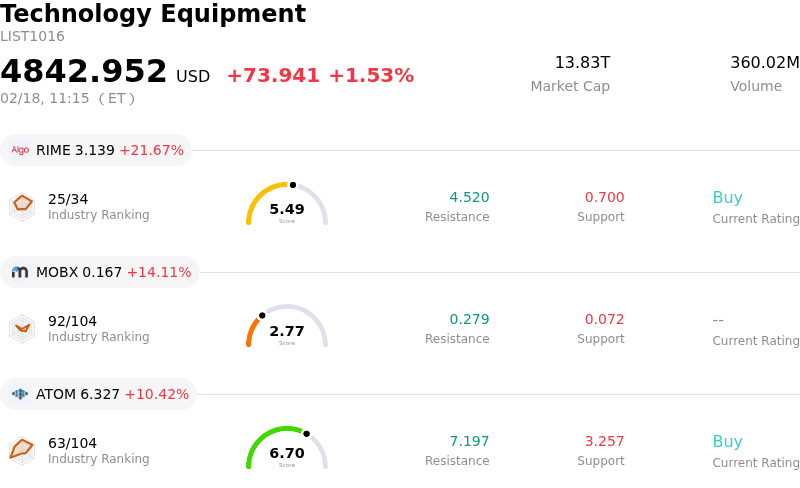

ASML Holding NV Stock Moved Up by 3.40% on Feb 18: Facts Behind the Movement

ASML Holding NV (ASML) moved up by 3.40%. The Technology Equipment industry is up by 1.53%. The company outperformed the industry. Top 3 gainers of the industry: Algorhythm Holdings Inc (RIME) up 21.67%; MOBIX LABS, INC. (MOBX) up 14.11%; Atomera Inc (ATOM) up 10.42%.

ASML's stock experienced significant upward movement today, driven primarily by continued positive sentiment surrounding its crucial role in the artificial intelligence (AI) infrastructure buildout and strong analyst conviction. Several reports published today and in the preceding days highlight the company's unassailable monopoly in extreme ultraviolet (EUV) lithography systems, which are essential for producing the most advanced semiconductors that power AI, data centers, and smartphones. This technological leadership positions ASML as a systemic bottleneck in the global semiconductor industry, making its equipment indispensable for chip manufacturing.

A key factor contributing to the positive momentum is the robust demand for ASML's machines, particularly from AI-focused data center projects. Management has indicated a notable increase and acceleration of capacity expansion planning across a significant portion of its customer base. This strong order momentum is expected to translate into sustained growth through 2026 and beyond.

Recent financial results have further fueled investor confidence. ASML reported strong fiscal Q4 2025 earnings on January 28, exceeding revenue estimates and showing significant growth in net bookings. The quarterly bookings reached 13.2 billion Euros in Q4, almost doubling Wall Street's expectations, with a substantial portion coming from EUV bookings. The company also provided an optimistic outlook for 2026, forecasting total net sales between 34 billion Euros and 39 billion Euros, alongside healthy gross margins. This guidance suggests double-digit sales growth for the year, with margin expansion driven by increased EUV and High-NA shipments. The company also announced a new share buyback program, indicating financial strength and a commitment to shareholder returns.

Analyst forecasts have largely reflected this positive outlook. Several analysts have recently reiterated or upgraded their ratings and price targets for ASML, with a consensus "Moderate Buy" rating and an average price target that suggests further upside. Wells Fargo, for instance, recently increased its price target, and Bernstein raised its price target significantly while maintaining a Buy rating. This strong analyst conviction, coupled with positive institutional activity where several firms have increased their stakes in ASML, underscores the market's belief in the company's long-term growth prospects. Investors are increasingly viewing semiconductor spending as an AI infrastructure buildout that could extend through the end of the decade, making ASML a critical component of this trend.

Technically, ASML Holding NV (ASML) shows a MACD (12,26,9) value of [55.28], indicating a neutral signal. The RSI at 59.47 suggests neutral condition and the Williams %R at -41.54 suggests oversold condition. Please monitor closely.

ASML Holding NV (ASML) is in the Technology Equipment industry. Its latest annual revenue is 36.83B, ranking 7 in the industry. The net profit is 10.83B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 1358.60, a high of 1868.00, and a low of 935.00.

Company Specific Risks:

- Intensifying geopolitical tensions and potential tightening of export controls on advanced lithography equipment to China pose a significant threat, potentially limiting ASML's addressable market and reducing near-term revenue.

- The company's current premium valuation, with shares trading significantly above estimated fair value and a high P/E ratio, leaves little margin for error and increases susceptibility to adverse market reactions from any future operational or guidance disappointments.

- Despite current tailwinds from AI-driven demand, ASML remains exposed to the inherent cyclicality of the semiconductor industry, and any future slowdown or shift in artificial intelligence investments could negatively impact order intake and revenue growth.