Why I Just Bought e.l.f. Beauty Stock

Key Points

e.l.f. Beauty is still a low-cost leader even after making an important increase to its prices.

The stock is down more than 60% from its all-time high, providing a compelling entry point.

Smart investors debate whether it's smart to keep some cash on the sidelines, waiting to be invested opportunistically. I see merit in both perspectives. But I've kept a cash position in recent years, hoping to use it once I saw some better deals.

The S&P 500 has provided above-average returns in recent years, meaning I've used less of this cash than I originally anticipated. But thankfully, I've been finding opportunities I like in recent months, allowing me to finally invest some of this cash.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

My most recent addition is a small position in e.l.f. Beauty (NYSE: ELF). Allow me to briefly explain why I just bought this consumer discretionary stock.

A beautiful portfolio addition

As an investor, I'm prioritizing stocks where I actually like the business (as opposed to companies with good numbers but that I'm otherwise disinterested in), and members of my household are avid fans of e.l.f. Beauty's products. This alone was enough to put the stock on my watch list. But it rose in the rankings due to its growth rate.

Image source: Getty Images.

e.l.f. Beauty expects to grow its fiscal 2026 net sales by at least 22% year over year -- it's already completed three quarters of fiscal 2026, and its net sales are up 21%. The company has found a growing base of adopters attracted to the low prices of its products.

On Aug. 1, e.l.f. Beauty raised its prices by about 15%, which is a substantial increase. But the company's products are still roughly 20% cheaper than competitive mass-market brands, allowing it to remain a low-cost leader. In other words, it quickly boosted sales and margins without sacrificing its market position, which is a move I love.

To be clear, e.l.f. Beauty is a profitable business, but profits are down. Tariffs have hit the company's gross margin, considering its products are made in heavily hit China. And in May, it acquired beauty brand rhode for $1 billion, which has also impacted the financial statements for now.

Nevertheless, e.l.f. Beauty is growing its top line by double digits, navigating macro-economic volatility, and making acquisitions while still delivering profits according to generally accepted accounting principles (GAAP). I think that's commendable.

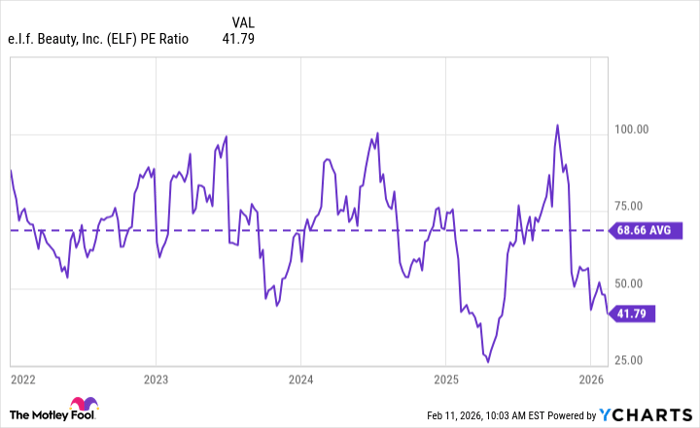

Moreover, e.l.f. Beauty stock has dropped significantly from its highs, and it now trades at a price-to-earnings (P/E) ratio of 42. While that's considered expensive, it's below its average valuation since the start of 2022, as the chart below shows.

ELF PE Ratio data by YCharts

Keep in mind that profits are down for e.l.f. Beauty, and the valuation is below average already. If profits return to more normalized levels as it works through what are (hopefully) temporary headwinds, profits should rise, further lowering the valuation.

In conclusion, e.l.f. Beauty stock provides what I'm looking for: a growing business generating profits that trades at a valuation I can support. Moreover, the company's products are used in my own house, meaning I'll likely be interested in watching the business and holding the stock for years to come.

Should you buy stock in e.l.f. Beauty right now?

Before you buy stock in e.l.f. Beauty, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and e.l.f. Beauty wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $414,554!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,120,663!*

Now, it’s worth noting Stock Advisor’s total average return is 884% — a market-crushing outperformance compared to 193% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 14, 2026.

Jon Quast has positions in e.l.f. Beauty. The Motley Fool has positions in and recommends e.l.f. Beauty. The Motley Fool has a disclosure policy.

Related Articles

SpaceX IPO with Dual-Class Shares: Will Musk Secure the 25% Voting Control Denied by Tesla?

TradingKey - SpaceX is preparing for an IPO this year. According to foreign media reports, SpaceX is considering a dual-class share structure for its IPO, which would grant specific shareholders extra voting rights. In other words, Elon Musk could maintain absolute control over the company even if h

Silver Plunges 10%, Gold Tests $4,900: Is the Bull Market Over Ahead of CPI?

TradingKey - Ahead of the release of the U.S. January CPI report, financial markets experienced a sudden broad sell-off on Thursday. Alongside a sharp decline in U.S. equities, prices for commodities such as gold (XAUUSD) also plummeted. Gold dropped nearly $200 within a 30-minute window, a decline

Bitcoin Price Prediction 2029-2035: Institutional Accumulation and the U.S. Treasury’s Strategic Reserve Pivot

Explore the 2026 Bitcoin landscape: From the U.S. Strategic Reserve and Michael Saylor’s $75B war chest to Cathie Wood’s 2030 forecast. Is BTC the new Digital Gold?

This $1 Trillion AI Stock Is Getting Ready for 2026: Is Meta a Good Buy?

When ads and commerce are factored in, Meta is building a long-term platform—in Augmented Reality and smart glasses — to get us closer to the future of AI. This device hardware business is less profitable than ads right now, but it could grow the company’s ecosystem and open up new ways for it to ma