AstraZeneca PLC Stock Opened Up by 3.17% on Feb 11: A Full Analysis

AstraZeneca PLC (AZN) opened up by 3.17%. The Pharmaceuticals & Medical Research industry is down by 0.85%. The company outperformed the industry. Top 3 gainers of the industry: PainReform Ltd (PRFX) up 25.08%; Quince Therapeutics Inc (QNCX) up 25.05%; Phio Pharmaceuticals Corp (PHIO) up 13.39%.

AstraZeneca's stock has experienced notable positive movement today, primarily driven by a confluence of strong financial results, optimistic future guidance, and significant advancements in its drug pipeline.

The company recently reported robust full-year 2025 financial performance, showcasing an increase in total revenue and core earnings per share. This solid performance, particularly in its oncology portfolio, has been well-received by the market. Accompanying these results, management issued reassuring guidance for 2026, projecting continued growth in both revenue and core earnings per share, which aligns with or exceeds analyst expectations. The declaration of an increased dividend also signals strong financial health and confidence from the company's leadership.

A key catalyst for today's positive sentiment stems from pipeline developments, especially the announcement that AstraZeneca is progressing its oral GLP-1 receptor agonist, elecoglipron, into Phase III trials for obesity and type 2 diabetes. This follows positive Phase IIb study results that demonstrated efficacy in weight reduction and blood glucose control. Entering this highly competitive and rapidly expanding weight-loss market with a promising oral candidate is a significant strategic move, with the company expressing confidence in its drug's competitive profile.

Further bolstering the positive outlook are recent regulatory milestones. AstraZeneca Pharma India secured approval for an additional indication for its cancer treatment Imfinzi in India. Additionally, the company's DATROWAY, a potential treatment for metastatic triple-negative breast cancer, was granted Priority Review in the US, indicating its potential to address an unmet medical need.

The recent transition of AstraZeneca's ordinary shares to the New York Stock Exchange in early February 2026, replacing its former American Depositary Receipts, has also likely contributed to increased investor visibility and liquidity within the US market. Overall, a strong financial footing, an promising drug pipeline, and favorable regulatory news are collectively driving the positive investor sentiment.

Technically, AstraZeneca PLC (AZN) shows a MACD (12,26,9) value of [17.50], indicating a buy signal. The RSI at 86.27 suggests overbought condition and the Williams %R at -2.36 suggests oversold condition. Please monitor closely.

AstraZeneca PLC (AZN) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is 54.07B, ranking 9 in the industry. The net profit is 7.04B, ranking 12 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 120.46, a high of 242.22, and a low of 81.91.

Company Specific Risks:

- Ongoing regulatory investigations in China concerning alleged illegal drug imports, data breaches, and health insurance fraud create significant uncertainty for revenue in a key growth market and have led to a US securities class action lawsuit.

- Deutsche Bank reiterated a "Sell" rating on the stock, citing increased skepticism about AstraZeneca's pipeline outlook, particularly in the breast cancer treatment space.

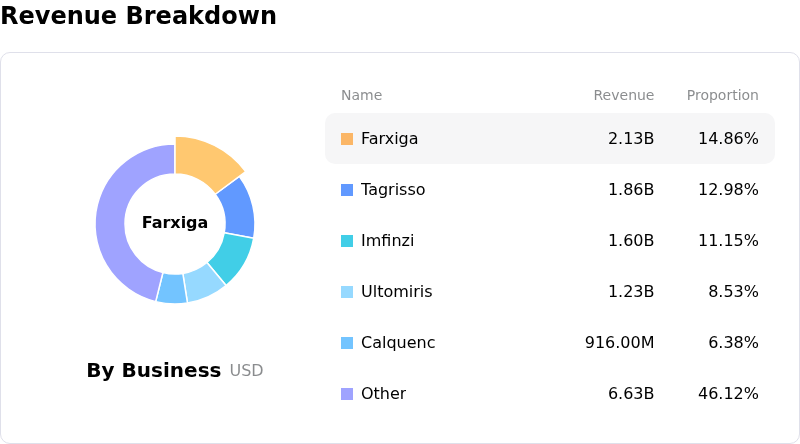

- Upcoming patent expirations for key drugs such as Farxiga and Tagrisso pose a material financial risk, requiring flawless execution and delivery from the company's development pipeline to offset potential revenue loss.

- Management's caution about potential near-term margin constraints due to ongoing cost pressures and challenging comparables following strong 2025 performance.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.