Everyone Thinks AI Will Destroy Adobe's Business. Here's Why It Could Flourish Instead.

Key Points

Since ChatGPT kicked off the Age of AI, Adobe shares are down 21% on fears that AI could make its services obsolete.

The sell-off has accelerated in recent months, while short interest mounts as investors bet against the stock.

Throughout the sell-off, Adobe has increased revenue, net income, and earnings per share in each fiscal year.

Since OpenAI's ChatGPT made its debut in November 2022 and ushered in the Age of AI, the S&P 500 has risen 68%. While mostly powered by gains from big tech stocks, plenty of other companies like McDonald's and Starbucks have rallied on expectations that AI-driven technologies will supercharge productivity and increase margins.

Yet in this time frame, Adobe (NASDAQ: ADBE) has suffered. Shares of the $112 billion company, which offers creative products for photographers, video editors, graphic and experience designers, game developers, content creators, marketers, and more, trade down 21% on fears that AI content-creating technologies will make its services obsolete.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

This year, the sell-off has intensified, with shares down 23.5% year to date. The mainstream media is piling on, with Forbes wondering whether Adobe is a "falling knife," while Wall Street firms dumped a net 4.8 million shares last quarter.

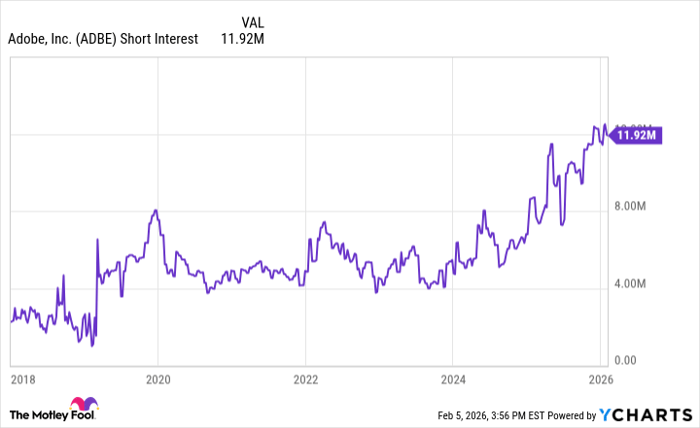

The mounting pessimism about Adobe is reflected in rising short interest, or the percentage of the company's stock that has been sold short. As you can see, it's easily at an eight-year high.

Data by YCharts.

The short sellers may be right. But with bearish sentiment abounding, I'm reminded of something the legendary investor Jim Rogers once said: "When there's something about markets that everyone 'knows' to be true, it's time to look at the other side of the trade."

On this advice, I've asked myself what the bears may be missing -- and why Adobe could be a compelling buy today.

If Adobe is doomed, why do earnings keep rising?

In its first earnings conference held after ChatGPT took the world by storm, Adobe reported record revenue of $19.41 billion for the just-completed fiscal year, and 17% earnings growth year over year, with strong numbers in its Creative Cloud, Document Cloud, and Experience Cloud segments.

Image source: Getty Images.

Fast-forward three years, and Adobe again reported record results for the 2025 fiscal year. Revenue jumped to $23.77 billion, up 11% year over year. Net income jumped to $7.13 billion, up from $5.56 billion in fiscal 2024.

In the first three fiscal years that have been reported since the Age of AI kicked off, here's how Adobe's revenue, net income, and earnings per share have fared.

| Fiscal Year | Revenue | Net Income | EPS | Share Buybacks |

|---|---|---|---|---|

| 2022 | $17.61 billion | $4.76 billion | $10.10 | 15.7 million shares |

| 2023 | $19.41 billion | $5.43 billion | $11.82 | 11.5 million shares |

| 2024 | $21.51 billion | $5.56 billion | $12.36 | 17.5 million shares |

| 2025 | $23.77 billion | $7.13 billion | $16.70 | 30.8 million shares |

Data source: Adobe.com.

Looking down each column, it's striking how the numbers keep climbing, unless you count a slight slowdown in share buybacks in 2023. Adobe doesn't pay a dividend, so share buybacks are how management returns value to shareholders. Its repurchasing of over 70 million shares since 2022 is very significant for a stock with just 410.5 million shares outstanding.

Meanwhile, as Wall Street speculates that the $15.7 trillion AI revolution will bulldoze Adobe, the company is hugging the technology tight.

"The biggest opportunity for Adobe in decades"

In the company's Q3 earnings call last September, CEO Shantanu Narayen called the AI revolution "the biggest opportunity for Adobe in decades." He pointed to the popularity of the Adobe Experience Platform (AEP) AI Assistant, with 70% of eligible AEP customers using it, and the company's success in introducing innovative new AI-first products, with AI already heavily integrated into Adobe's flagship applications in Creative Cloud.

Since that call, the company has released its Q4 earnings report, which expanded on Adobe's adoption of AI across its platforms. One statistic stood out to me: In Q4, Adobe achieved record bookings of deals valued at over $1 million, while the number of clients paying Adobe $10 million or more in annual recurring revenue grew by 25% year over year.

This is a sign that Adobe's AI embrace is paying off, and that clients are thrilled with the fantastical-seeming abilities of its new services. Anything can happen, but as Mark Twain might say, rumors of this company's death are greatly exaggerated. For investors with moderate risk tolerance, Adobe is a worthy speculation.

Should you buy stock in Adobe right now?

Before you buy stock in Adobe, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Adobe wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $439,362!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,164,984!*

Now, it’s worth noting Stock Advisor’s total average return is 918% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 10, 2026.

William Dahl has positions in Starbucks. The Motley Fool has positions in and recommends Adobe and Starbucks. The Motley Fool recommends the following options: long January 2028 $330 calls on Adobe and short January 2028 $340 calls on Adobe. The Motley Fool has a disclosure policy.

Related Articles

After $20B Debt Sale, Google’s Rare 100-Year Bond Sparks Scrutiny: Has AI Drained the Tech Giant’s Coffers?

TradingKey - According to a Financial Times report, Google parent Alphabet (GOOG)(GOOGL) is planning to issue bonds denominated in British pounds and Swiss francs, which may include the first 100-year GBP bond of this century.

Netflix After the Warner Deal: What Investors Should Know

TradingKey - For quite some time now, Netflix (NFLX) has been regarded as the premier subscription-based streaming service in the world, with a well-established history of growth through creative use of pricing power, developing hit programming, and relying very little on outside sources for licensi

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.