Walt Disney Co Stock Moved Up by 3.22% on Feb 10: What Signal Does It Send?

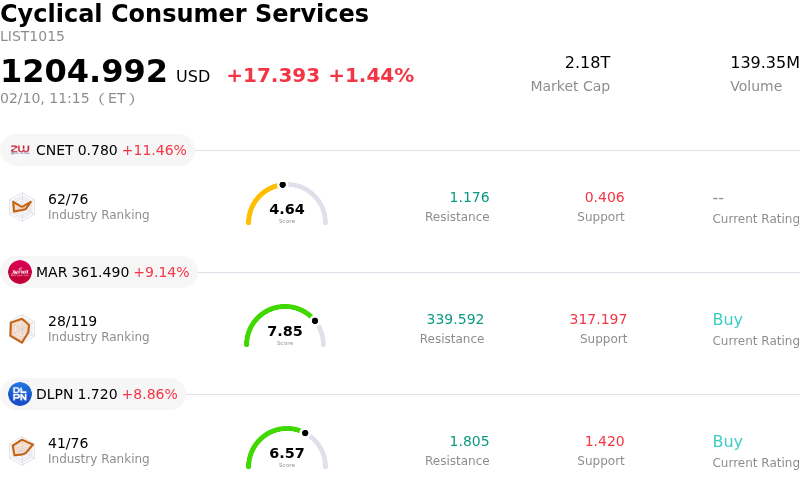

Walt Disney Co (DIS) moved up by 3.22%. The Cyclical Consumer Services industry is up by 1.44%. The company outperformed the industry. Top 3 gainers of the industry: ZW Data Action Technologies Inc (CNET) up 11.46%; Marriott International Inc (MAR) up 9.14%; Dolphin Entertainment Inc (DLPN) up 8.86%.

The Walt Disney Company (DIS) stock saw significant upward movement today, primarily influenced by positive financial news and strategic corporate developments. The company's share price appreciation follows its fiscal first-quarter 2026 earnings report, which was released on February 2nd. Despite an initial mixed reaction that saw some pre-market decline, investor sentiment appears to have turned positive as the market digested the details.

A major driver of this positive sentiment stems from Disney's strong performance in its Experiences segment, which includes theme parks and resorts. This segment delivered record quarterly revenue and healthy operating income, underscoring its importance as a consistent cash generator for the company. Management also expressed optimism for the segment's continued growth, with expansion projects underway at all theme parks, and new cruise ships launching.

Furthermore, the company's streaming segment continues to show promising progress towards profitability. While Disney did not disclose specific subscriber numbers for Disney+, Hulu, and ESPN this quarter, following a shift in reporting strategy, the streaming division reported increased revenue and a notable improvement in operating income, surpassing previous year's figures. Executives have indicated confidence in achieving a target operating margin for its streaming video-on-demand services for the full fiscal year.

Analyst forecasts also played a role in today's positive movement. Following the earnings report, several investment firms reiterated their "Buy" ratings and upwardly revised their price targets for DIS, reflecting a constructive outlook on the company's future performance. This positive analyst commentary likely contributed to increased investor confidence. Additionally, Disney's announced plan for a near-record stock buyback program for fiscal 2026, aiming to return capital to shareholders, further bolstered investor enthusiasm. This strategic move, coupled with strong free cash flow projections, suggests management believes the stock is undervalued and is committed to enhancing shareholder value.

Technically, Walt Disney Co (DIS) shows a MACD (12,26,9) value of [-0.90], indicating a sell signal. The RSI at 44.40 suggests neutral condition and the Williams %R at -59.92 suggests oversold condition. Please monitor closely.

Walt Disney Co (DIS) is in the Cyclical Consumer Services industry. Its latest annual revenue is 94.42B, ranking 1 in the industry. The net profit is 12.40B, ranking 1 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 131.05, a high of 160.00, and a low of 77.00.

Company Specific Risks:

- The Entertainment division experienced a 35% drop in operating profit for Q1 2026, primarily due to increased marketing costs for new theatrical releases and the ongoing decline in linear television networks, leading to softer-than-expected fiscal Q2 guidance.

- Theme park operations face headwinds from a decline in international visitors to U.S. parks, which is expected to result in only modest operating income growth for the segment in Q2.

- The Sports segment, including ESPN, saw a 23% reduction in operating income due to rising sports rights expenses and a $110 million impact from a temporary distribution dispute with YouTube TV.

- Several analysts, including BofA and Rosenblatt, lowered their price targets and some revised ratings to "hold" following the Q1 earnings, citing an uninspiring outlook and stalled growth across segments in the upcoming quarter.