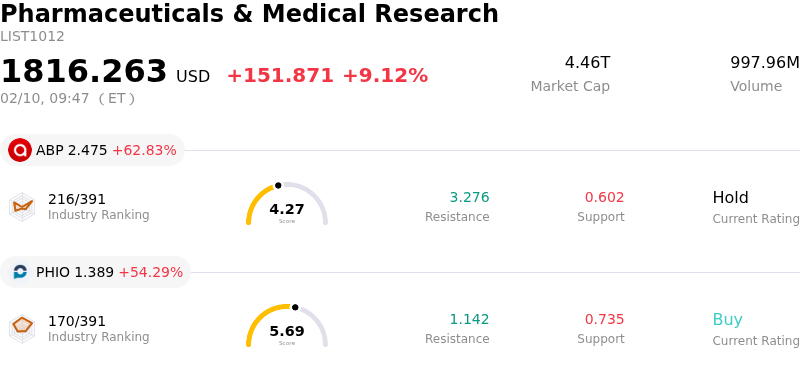

AstraZeneca PLC Stock Opened Up by 3.29% on Feb 10: Key Drivers Unveiled

AstraZeneca PLC (AZN) opened up by 3.29%. The Pharmaceuticals & Medical Research industry is up by 9.12%. The company underperformed the industry. Top 3 gainers of the industry: Quince Therapeutics Inc (QNCX) up 108.77%; ABPRO Holdings Inc (ABP) up 62.83%; Phio Pharmaceuticals Corp (PHIO) up 54.29%.

AZN experienced an upward movement due to a combination of strong financial results, positive earnings guidance, a dividend increase, and promising pipeline developments.

The company reported better-than-expected fourth-quarter 2025 financial results, with both revenue and earnings per share surpassing analyst forecasts. AstraZeneca’s Q4 2025 revenue reached $15.5 billion, marking a 4% year-over-year growth, while core earnings per share (EPS) improved to $2.12, exceeding analyst projections of $2.11 EPS on $15.46 billion in revenue. This strong performance was significantly driven by its oncology portfolio, which saw a 22% year-over-year revenue increase to $7.0 billion, fueled by key cancer drugs like Tagrisso and Imfinzi.

AstraZeneca also provided an optimistic outlook for 2026, forecasting continued growth in both total revenue and core EPS. The company projects total revenue to grow by a mid-to-high single-digit percentage at constant exchange rates, and core profit to increase by a low double-digit percentage. This positive guidance, which implies a modest upgrade to Street revenue estimates, signaled confidence in its future performance and strategic initiatives.

Further bolstering investor sentiment, AstraZeneca announced an increase in its annual dividend to $3.30 per share for 2026, following a 3% rise in the total dividend declared for fiscal year 2025 to $3.20 per share. This dividend increase signals the company's financial strength and commitment to returning value to shareholders.

Additionally, positive news regarding its drug pipeline contributed to the stock's upward momentum. AstraZeneca initiated a late-stage (Phase 3) program for its oral GLP-1 drug, elecoglipron, for obesity and type 2 diabetes, following successful mid-stage trials. This move positions AstraZeneca to compete in the lucrative weight-loss drug market. The company also announced plans for more than 20 Phase 3 trial readouts in 2026, with the potential for over $10 billion in peak revenue. Recent regulatory updates, including the FDA granting priority review for a label expansion of its cancer therapy Datroway for metastatic triple-negative breast cancer, further highlighted pipeline progress. However, the company also noted a mixed regulatory update with the denial of approval for an injectable version of Saphnelo, a lupus treatment. The European Medicines Agency's CHMP also recommended Imfinzi for approval in the EU for early gastric and gastroesophageal cancers, adding to the positive news.

Analyst sentiment remains largely positive, with a consensus "Moderate Buy" rating and an average 12-month price target that suggests potential upside. The company's recent strategic moves, such as its new NYSE listing and significant investments in China, also contribute to its long-term growth prospects.

Technically, AstraZeneca PLC (AZN) shows a MACD (12,26,9) value of [15.21], indicating a buy signal. The RSI at 85.41 suggests overbought condition and the Williams %R at -5.68 suggests oversold condition. Please monitor closely.

AstraZeneca PLC (AZN) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is 54.07B, ranking 9 in the industry. The net profit is 7.04B, ranking 11 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 120.46, a high of 242.22, and a low of 81.91.

Company Specific Risks:

- AstraZeneca faces multiple clinical development setbacks, including the discontinuation of the Phase 2 heart failure drug AZD3427 due to underwhelming efficacy and the termination of the Phase 1 trial for AZD0233 following an adverse nonclinical toxicology finding. Additionally, the company abandoned plans to file its PARP inhibitor Lynparza for newly-diagnosed, advanced ovarian cancer and discontinued the TROPION-Lung12 study due to operational feasibility concerns.

- Regulatory hurdles pose an immediate risk as the U.S. FDA denied approval for the injectable version of Saphnelo, a systemic lupus erythematosus treatment, requiring a resubmission and delaying its market expansion.

- A legal defeat regarding Louisiana's 340B contract pharmacy law limits AstraZeneca's control over drug discounts, as an appeals court upheld the state law, preventing the company from denying hospitals the same 340B discounts for drugs dispensed at community pharmacies.

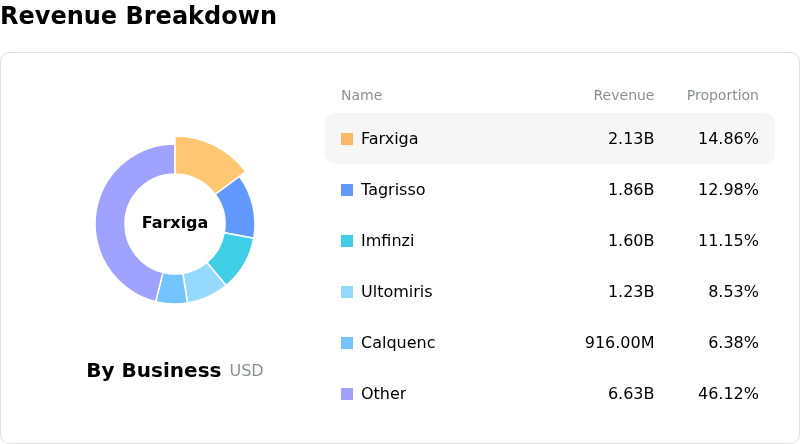

- The company is approaching "material patent pressures" in the first half of 2026, notably with its drug Farxiga, which could lead to significant revenue erosion from generic competition.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.