Morgan Stanley Warns Oracle Credit Protection Nearing Record High

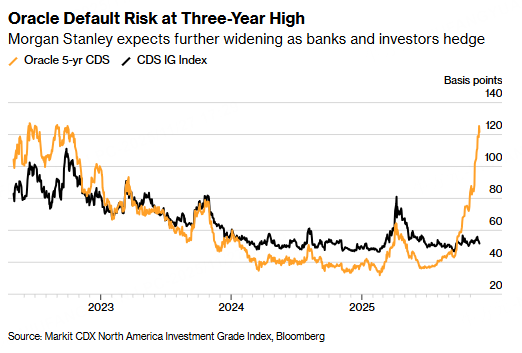

According to Morgan Stanley, as of November, the risk indicators of Oracle's debt have reached their highest level in three years. And by 2026, the situation will only get worse unless this database giant can alleviate investors' concerns about the large-scale artificial intelligence investment boom.

According to credit analysts Lindsay Tyler and David Hamburger of the brokerage firm, the risks faced by Oracle include funding gaps, expanding balance sheets, and technological obsolescence, among others. According to ICE Data Services, the cost of providing default insurance for Oracle's debt has risen to 1.25 percentage points per year within the next five years.

The price on the five-year credit default swaps is at risk of toppling a record set in 2008 as concerns over the company’s borrowing binge to finance its AI ambitions continue to spur heavy hedging by banks and investors, they warned in a note Wednesday.

The CDS could break through 1.5 percentage point in the near term and could approach 2 percentage points if communication around its financing strategy remains limited as the new year progresses, the analysts wrote. Oracle CDS hit a record 1.98 percentage point in 2008, ICE Data Services shows.

A representative for Oracle declined to comment.

Oracle is among firms taking part in an artificial intelligence spending race, which has quickly made the data center giant the credit market’s barometer for AI risk. The company borrowed $18 billion in the US high-grade market in September. Then in early November, a group of about 20 banks arranged a roughly $18 billion project finance loan to construct a data center campus in New Mexico, which Oracle will take over as tenant.

Banks are also providing a separate $38 billion loan package to help finance the construction of data centers in Texas and Wisconsin developed by Vantage Data Centers, Bloomberg reported last month. Lenders involved in these construction loans linked to Oracle are likely a key driver of the surge in trading volume on the Oracle’s CDS recently, a trend that may persist, according to Morgan Stanley.

“Over the past two months, it has become more apparent that reported construction loans in the works, for sites where Oracle is the future tenant, may be an even greater driver of hedging of late and going forward,” wrote the analysts.

There is a risk that some hedges by banks could unwind if and when banks distribute these loans to other parties, they wrote. Still, other parties may also hedge at some point even if down the road plus the construction debt funding needs don’t stop after the Vantage sites and the New Mexico site.

Last month, the analysts said they expect near-term credit deterioration and uncertainty to drive further hedging by bondholders, lenders and thematic players.

“The bondholder hedging dynamic and also the thematic hedging dynamic could both grow in importance down the road,” they added.

Oracle CDS have underperformed the broader investment-grade CDX index and Oracle corporate bonds have underperformed the Bloomberg high-grade index amid the jump in hedging demand and the weakening sentiment. Concerns have also started to weigh on Oracle’s stock, which the analysts said may incentivize management to outline a financing plan on the upcoming earnings call, including details on Stargate, data centers and capital spending.

Previously, analysts had been recommending that investors purchase Oracle's bonds and CDS. This type of operation is known as "basis trading", and the aim was to profit by taking advantage of their expectation that credit derivatives would experience greater fluctuations than bonds. Now, they have stated that directly purchasing CDS products would be a simpler trading method.

“Therefore, we are closing the ‘buy bond’ part of the basis trade, and keeping the ‘buy CDS protection’ leg of it,” they wrote. “We think a trade in CDS outright is cleaner right now and will result in a greater spread move.”

Related Articles

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market

USD Dollar Trend Forecast: Dollar Index Falls Below 97.0 to 4-Year Low, Will the Dollar Continue To Fall or Bottom Out in 2026?

TradingKey - In January 2026, the US Dollar Index continued its downward trend from 2025, officially breaking below the key 97.0 level and reaching a low of 95.5, marking a nearly four-year low since February 2022.