3 Reasons to Buy This High-Yield Dividend King Like There's No Tomorrow

If you like boring companies that reward you well for sticking around, you'll love high-yield Dividend King and consumer staples giant PepsiCo (NASDAQ: PEP). It is out of favor on Wall Street right now, but it is actively working to get its business back on track. If history is any guide, the current situation is an opportunity for long-term dividend investors to buy a great company.

If you wait for some distant tomorrow there's a good chance you'll miss out. Here are three reasons to buy this stock like there's no tomorrow.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

1. Buy PepsiCo for the dividend

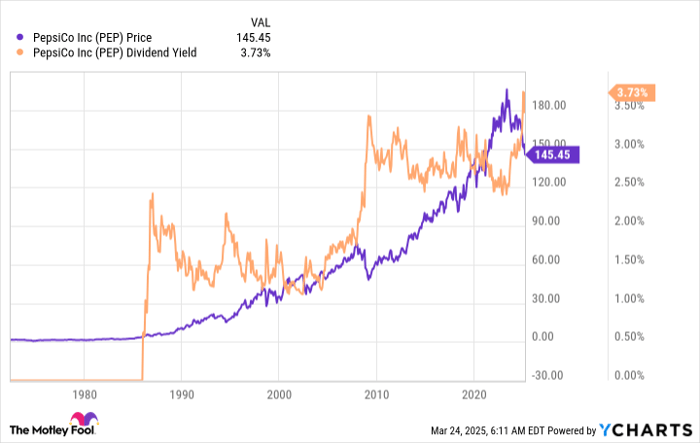

One of the very first reasons to be attracted to PepsiCo today is its 3.7% dividend yield. The average consumer staples stock has a yield of 2.6%. The S&P 500 has an even lower yield of just 1.2%. So, on a relative basis compared to peers and the broader market, PepsiCo's yield is highly attractive.

Data by YCharts.

PepsiCo's dividend yield is also attractive relative to its own history, sitting at the high end of the company's historical yield range. That suggests that PepsiCo is historically cheap, a fact that's backed up by more traditional valuation metrics like the price-to-sales and price-to-earnings ratios. Those metrics, and others, are below their five-year averages.

On top of the yield story, there's another dividend fact to know about: PepsiCo is a Dividend King, with 52 consecutive annual dividend increases behind it. So not only does the stock have a high yield and look cheap, but it also has an incredible history of returning value to investors via regular dividend growth in both good times and bad.

2. PepsiCo's business has a strong and diversified foundation

No company gets to be a Dividend King by accident. It requires a strong business model that is executed well through the inevitable business swings it will face. One of the key aspects of PepsiCo's approach is to diversify its portfolio.

For starters, PepsiCo is a consumer staples maker, which means it sells products that tend to be purchased regardless of the economic environment. From a big-picture perspective, it sells food. But there's more to the story.

PepsiCo is the dominant salty snack food company, it is the second biggest U.S. beverage maker, and it has a solid position in the packaged food space. It is probably among the most diversified food makers you can buy.

Given the company's massive size (it has a market cap of roughly $200 billion), it has scale advantages that set it apart as well. The company's portfolio is large and varied, it has a global distribution network, the marketing team is industry-leading, and the company can, and does, use acquisitions to update its portfolio. PepsiCo is, without a doubt, an industry-leading consumer staples company.

3. PepsiCo is executing its playbook to maintain growth

Having a good playbook is great, but every company goes through hard times. That's the case right now with PepsiCo, as growth has cooled off following a strong growth period driven by post-coronavirus pandemic inflation. The snack category, where the company is most dominant, appears to be facing particular headwinds.

PepsiCo isn't sitting around waiting for things to get better -- it is actively working to shift and change with the world around it. That has included buying the 50% of Sabra, a spread maker, it didn't own. It also bought Siete, a Mexican-American food maker with products that touch on both snacks and packaged foods. And most recently, PepsiCo agreed to buy Poppi, a prebiotic soda brand.

All three moves are right in line with the company's long-term playbook and should help it boost growth. In fact, for Siete and Poppi, all PepsiCo needs to do is plug the products into its vast distribution network and growth should be significant.

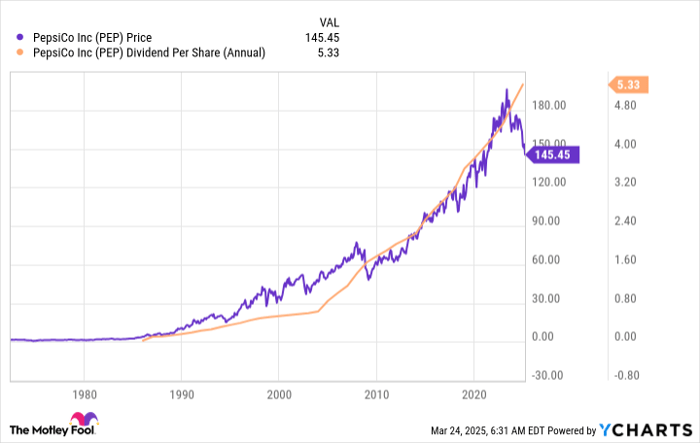

Data by YCharts.

The big takeaway here, however, is that PepsiCo is taking steps to get back on track. Historically it has managed that feat each time it has hit a soft patch. There's no particular reason to believe, given its actions, that it won't succeed again this time around.

Don't wait -- this opportunity won't last forever

There is a lot of uncertainty in the stock market today, and it might be hard to pull the trigger and buy an out-of-favor stock. But PepsiCo is an incredibly well-run company, and its valuation and yield are very attractive, historically speaking and relative to other investment options. Now is the time to buy like there's no tomorrow -- because tomorrow, this opportunity to buy at a discount might be gone.

Should you invest $1,000 in PepsiCo right now?

Before you buy stock in PepsiCo, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and PepsiCo wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $682,965!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of March 24, 2025

Reuben Gregg Brewer has positions in PepsiCo. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Related Articles

Tesla Stock Outlook: Competing With Rivian, Robotaxi Potential, and 2026 Prospects

There is much conversation about the prospect of investing in Tesla (TSLA) as we move closer to 2026. The volatility of its share price in 2025 is leading many investors to consider if they should purchase shares of Tesla given the alternatives available in terms of electric vehicles (Rivian, etc.).

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market