Alphabet Drops 7% Due to Two Shocks in Q4 Financial Results

TradingKey – On Tuesday, February 4, Google (GOOG.US), one of the "Magnificent Seven" U.S. tech giants, released its fourth-quarter earnings report for the period ending December 31, 2024. Shares of the Google parent company plummeted 7% in after-hours trading, likely due to investor dissatisfaction with slowing cloud growth and surging AI-related expenditures.

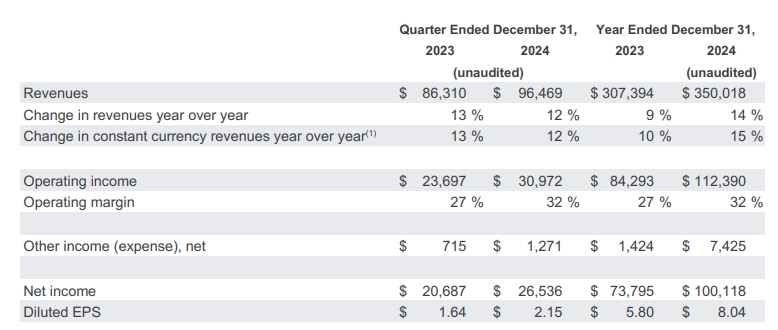

Overall, Google's Q4 revenue fell short of expectations, while earnings per share (EPS) exceeded estimates. However, both metrics showed slower growth compared to the previous quarter, with revenue growth hitting its lowest level since Q3 2023. For the full fiscal year 2024, Google reported total revenue of $350.02 billion and an EPS of $8.04, both below expectations.

In Q4 2024, Google’s total revenue was $96.47 billion, reflecting an annual increase of 12%, slightly below the LSEG consensus estimate of $96.56 billion. Net income rose 28% year over year to $26.54 billion, with an EPS of $2.15, exceeding expectations of $2.13.

【Google Q4 2024 Earnings Report, Source: Google】

Google Cloud Disappoints

Breaking down the results by segment, Google's search, advertising, and YouTube services outperformed expectations. However, its cloud division, which is seen as a key beneficiary of AI advancements, fell short of growth forecasts.

● Advertising: $72.46 billion (+10.6% YoY) vs. $71.73 billion expected

● Search: $54.03 billion (+12.5% YoY) vs. $53.29 billion expected

● Google Cloud: $11.96 billion (+30% YoY) vs. $12.19 billion expected

Analysts attribute the after-hours stock decline primarily to the cloud segment's underperformance. As of February 5, Google's latest closing price stood at $207.71, reflecting a 9% year-to-date gain.

Despite the slight miss, TradingKey Analyst Petar Petrov does not see GOOGL's results as remotely bad. The company delivered well on its ad business, with both Google Search and YouTube meeting revenue estimates.

The main disappointment came from the cloud business, with Q4 cloud revenue at $11.96 billion versus the expected $12.19 billion. However, Petrov believes the market reacted a bit too harshly for two reasons: (1) first, the revenue miss was small - just less than $250 million; (2) management clarified on the earnings call that the miss was due to supply bottlenecks, not lower demand for cloud services. Google Cloud still grew at a solid rate of 30% year-over-year, outpacing Microsoft's cloud growth of 19%.

CapEx Skyrockets

Petrov also points out that another aspect investors probably did not like is the capex (AI spending). GOOGL will be spending $75 billion in 2025, higher than the previously expected $59 billion and 36% more than the capex spent in 2024. The amount is quite substantial, indeed, but not unprecedented. For comparison, META will be spending $65 billion in 2025 – 75% more than what they spent in 2024.

GOOGL is already the cheapest-valuated stock among the Mag7, and after these earnings will be even cheaper. However, it is the uncertainty with regards to the legal/ regulatory issues that prevents the stock from going up significantly.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.