Microsoft Q2 FY2025: Earnings Beat But Wall Street Left Unimpressed – Should Investors Be Worried?

Cloud computing, gaming, and office software giant Microsoft Corporation (NASDAQ: MSFT) just released its fiscal Q2 2025 earnings (for the three months ending 31 December 2024). Despite strong numbers, Wall Street wasn’t thrilled.

Microsoft shares fell 5% in after-hours trading, reflecting concerns about Microsoft Azure’s cloud growth missing expectations. But was the reaction justified, or is this a golden buying opportunity for long-term investors?

Let’s break it all down as we take a closer look at the key numbers, what investors should do next, and the biggest risks to watch.

Microsoft’s Earnings: What Investors Need To Know

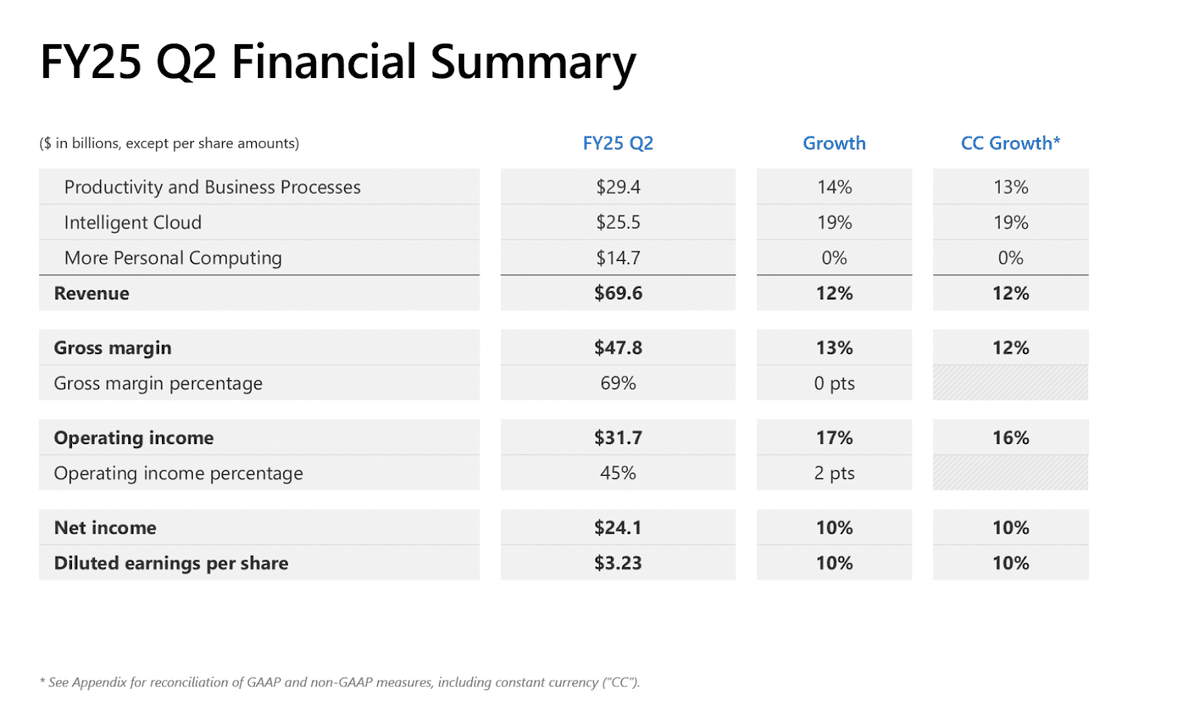

For the quarter, Microsoft’s revenue came in at US$69.6 billion, a 12% year-over-year increase and slightly above analyst estimates. The company also posted earnings per share (EPS) of US$3.23, beating the expected US$3.12.

Source: Microsoft’s Q2 FY2025 earnings presentation

But here’s where things got tricky: Azure’s cloud revenue growth came in at 31% year-on-year which, while strong, was at the lower end of Microsoft’s own guidance (31% to 32%) and below some analysts’ expectations. Given that Azure is a key growth driver for Microsoft, investors were hoping for a stronger beat.

Other highlights from the quarter included Microsoft Cloud revenue hitting US$40.9 billion, up 21% year-on-year. On the artificial intelligence (AI) side, AI-related revenue surged to a US$13 billion annual run rate, up 175% year-on-year.

For Microsoft 365, Commercial revenue grew 15%, helping sales from the Productivity & Business Processes segment to rise 14% year-on-year to US$29.4 billion. On the gaming front, Xbox revenue increased 2% year-on-year, driven by Call of Duty and Game Pass subscriptions.

LinkedIn revenue grew 9%, fuelled by premium subscriptions surpassing US$2 billion in annual revenue.

For Search & News advertising, revenue jumped 21% year-on-year and outperformed expectations.

Despite the strong numbers in AI, cloud demand, and consumer software, Microsoft guided Q3 FY2025 revenue in a range of US$67.7 billion to US$68.7 billion but this came in below Wall Street estimates of US$69.8 billion.

Microsoft results seem quite mixed. Microsoft beat the expectations on both revenue and EPS lines but the sales guidance of $67.7 billion to $68.7 billion for the next quarter did not meet the previous guidance of $69.78.

Also, the Cloud business did not impress either as the segment posted $40.9bn, below what analysts expected at $41.1bn, which further intensified the fears that Microsoft is trailing in cloud compared to Amazon and Alphabet. All this comes with $22.6 billion in capital expenditures, surpassing the consensus estimate of $20.95 billion. Even in terms of profitability, the Cloud gross margin decreased to 70% due to more spending.

Apparently, investors are worried that the MSFT increased spending does not translate into a competitive edge against peers, thus we see a 4% drop in the stock price after market-close.

What Should Investors Do?

According to TradingKey's Senior Equity Analyst, Petar Petrov, Microsoft's results seem quite mixed. While Microsoft beat the expectations on both revenue and EPS lines but the sales guidance of $67.7 billion to $68.7 billion for the next quarter did not meet the previous guidance of $69.78.

He also commented that, " The Cloud business did not impress either as the segment posted $40.9 billion, below what analysts expected at $41.1 billion, which further intensified the fears that Microsoft is trailing in cloud compared to Amazon and Alphabet. All this comes with $22.6 billion in capital expenditures, surpassing the consensus estimate of $20.95 billion. Even in terms of profitability, the Cloud gross margin decreased to 70% due to more spending.

Apparently, investors are worried that the MSFT increased spending does not translate into a competitive edge against peers, thus we see a 4% drop in the stock price after market-close."

So, the question remains whether the 5% drop is a buying opportunity or a warning sign for investors?

Long-term investors should see this as a minor setback. Microsoft’s business remains fundamentally strong, and AI growth is clearly accelerating. The 31% Azure growth might not have smashed estimates, but it's still outpacing key rivals like Google Cloud.

Meanwhile, Microsoft’s AI strategy is working. The company is at the forefront of AI innovation with OpenAI, DeepSeek partnerships, and the expansion of Copilot products, showing it has a real shot at dominating AI-driven enterprise software.

Finally, the business is still one with a solid moat. Microsoft owns multiple high-margin, subscription-based businesses that generate predictable cash flows. With nearly US$300 billion in remaining performance obligations (RPO), its future revenue pipeline looks rock solid.

For long-term investors, the dip could be an opportunity to buy shares at a slight discount, especially if you believe in the long-term potential of cloud computing and AI.

Risks to Monitor

That said, investors should also keep an eye on a few risks. One of the biggest ones is cloud capacity constraints: Microsoft admitted it is still struggling with supply constraints in cloud infrastructure and this could limit Azure’s growth in the short term.

Meanwhile, even though Microsoft is a leader in AI and cloud, rivals like Amazon’s AWS and Google Cloud are also ramping up investments in AI-powered enterprise solutions.

Finally, investors are concerned on costs. Microsoft’s capital expenditures are set to increase in the coming years, raising questions about the return on investment (ROI) from these massive AI-driven data centre expansions.

Microsoft Earnings Still Look Strong

Microsoft’s Q2 FY2025 earnings were solid, but the market fixated on Azure’s slight revenue shortfall and cautious guidance. While short-term traders may be nervous, long-term investors should recognise Microsoft’s dominance in cloud, AI, and enterprise software remains intact.

If you’re a long-term investor, this post-earnings dip could be an opportunity to buy shares at a better valuation before AI-driven revenue accelerates further.

However, staying patient and watching how Microsoft navigates its cloud capacity challenges and AI monetization obstacles will be key. Simply put: Microsoft isn’t perfect but it’s still one of the best long-term investments in the tech space.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.