Is Energy Transfer Stock a Buy Now?

With Donald Trump stepping into the presidency, an opportunity is on the horizon for the energy sector. Many expect more favorable policies to drive exploration and drilling within the United States, which could pave the way for expansion opportunities for oil and gas companies.

One area to watch is midstream energy stocks. These companies play a critical role in the energy supply chain, specializing in gathering, processing, transporting, storing, and exporting oil and gas. Midstream operators stand to gain from an uptick in production, and one midstream energy stock investors should consider today is Energy Transfer (NYSE: ET). Here's why.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. See the 10 stocks »

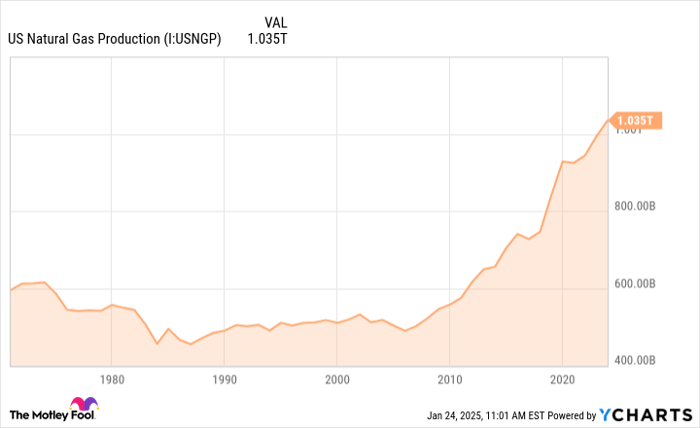

Natural gas production in the U.S. continues to climb

Energy Transfer is a powerhouse in the midstream sector, specializing in the transportation, storage, and terminal operations of vital energy commodities, including natural gas, crude oil, natural gas liquids (NGLs), and liquefied natural gas (LNG). The company boasts an extensive network of pipelines and storage facilities, ensuring efficient movement of natural gas from production sites directly to utilities, industrial clients, and other pipelines.

What sets Energy Transfer apart is that it is one of the largest integrated midstream operators in the United States, and recent trends have benefited it significantly. Since the 2010s, the U.S. has experienced an explosion in natural gas output, propelled by advancements in hydraulic fracturing (also referred to as fracking) and horizontal drilling -- techniques that have tapped into vast reserves of shale gas.

The U.S. is making significant strides in natural gas production, reaching 1,035 billion cubic meters in 2023, thanks to improved extraction techniques. Not only that, but many see natural gas as a bridge fuel to transition from higher-carbon sources like coal to more renewable sources such as wind, solar, and nuclear energy. Natural gas emits about 50% less carbon dioxide than coal.

Data by YCharts.

Energy Transfer has made significant moves to grow its footprint

With steady revenue streams generated from transportation fees and storage services, Energy Transfer is well-positioned to benefit from the increasing volumes of products flowing through its systems. The company has also made moves to boost its natural gas infrastructure footprint.

The company has reached a positive final investment decision for constructing the Hugh Brinson pipeline through central Texas. Previously known as the Warrior Pipeline, this infrastructure will link the Permian Basin to key markets and trading hubs, enhancing transportation capacity to satisfy the increasing demand for natural gas.

This project will be completed in two phases. In phase one, 200 miles of pipeline will be constructed, with a capacity of 1.5 billion cubic feet per day (Bcf/d). This part of the project is expected to be in service by the end of 2026. In phase two, the new pipeline's capacity would be increased to about 2.2 Bcf/d. The buildout will cost about $2.7 billion.

Image source: Getty Images.

In other news, Energy Transfer is making solid progress with its Lake Charles export facility in Louisiana. The company, which has spent years securing customers to commercialize this facility, entered into a 20-year LNG sale and purchase agreement with Chevron. As part of the agreement, Energy Transfer will supply Chevron with 2 million tonnes per annum (MTPA) of capacity.

Is Energy Transfer a buy today?

Demand for natural gas is growing, and Energy Transfer is well positioned to capitalize on this growth. The U.S. Energy Information Administration projects that natural gas demand in the U.S. will grow more than supply. In its forecast, the agency projects demand will rise by 1.4 Bcf/d while demand grows by 3.2 Bcf/d, primarily due to growing exports.

Investors must remember that Energy Transfer operates as a master limited partnership (MLP). This structure offers advantages to investors, including consistent cash flows and appealing distribution yields. However, it also comes with specific reporting requirements that could delay and complicate your taxes come tax season.

That said, Energy Transfer is one of the largest midstream operators in the U.S. and is priced quite reasonably compared to its peers. The MLP has also done a good job expanding its footprint, and a more favorable regulatory environment should bode well for it going forward -- making it a solid energy stock for investors to consider buying today.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $369,816!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $42,191!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $527,206!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of January 21, 2025

Courtney Carlsen has positions in Chevron. The Motley Fool has positions in and recommends Chevron. The Motley Fool has a disclosure policy.

Related Articles

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market

Why Ripple ETFs are Winning the Capital War Against Bitcoin

While Bitcoin and Ethereum ETFs face massive outflows, XRP ETFs have defied market trends with a historic 30-day inflow streak reaching $1.37 billion. Explore why institutional "smart money" is rotating into Ripple, the structural impact of the "Liquidity Lock," and why analysts set a 2026 price tar