This High-Yield Stock Is My Worst-Performing Investment and I Still Love It

When I look at my brokerage account, there is one stock that stands out as particularly disappointing performance-wise: Hormel Foods (NYSE: HRL). And yet, I haven't once thought of jettisoning it from my portfolio. Here's why I still love Hormel despite the fact that it is my worst performer.

Hormel Foods has a good core business

Even good companies go through difficult times. That's a key part of my investment approach, as I specifically try to find what are often called fallen angels. Hormel, specifically, owns the No. 1 or No. 2 brands in 40 retail categories. Some of its iconic brand names include Hormel, SPAM, Planters, and Skippy, but there are many more beyond that quartet.

Image source: Getty Images.

It also has a heavy focus on innovation, working to keep its brands relevant through new and improved variations. "New" and "improved" are two of the most tantalizing words in the retail sector. In fact, the company estimates that its net sales from "innovation" increased 1.4 percentage points year over year in fiscal 2024. Some of the new offerings include updated flavors of SPAM and seasoned varieties of Planters nuts, notably cashews.

Year in and year out, food maker Hormel gets the little things right. Even though it is dealing with headwinds right now, it is still focused on improving. And this means that my big-picture thesis on the company remains intact.

Rewarding me for sticking around

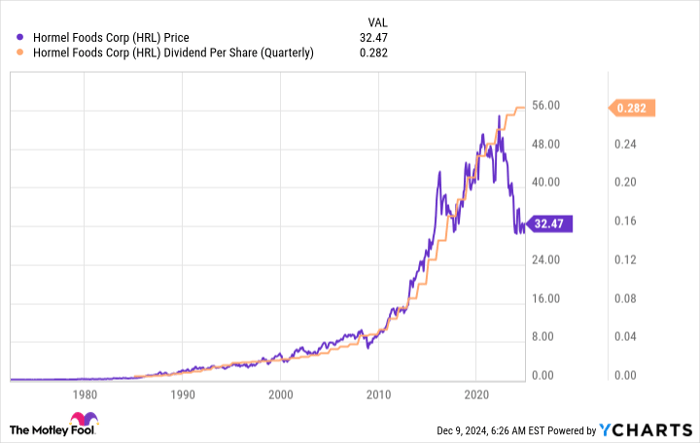

One of the reasons I selected Hormel was that it had a historically high dividend yield. At around 3.6%, it is higher now than when I bought it, so this attribute remains intact. That dividend has been increased annually for 59 consecutive years, which is another reason why I bought it. That makes Hormel a Dividend King, part of a highly elite group of companies. A company can't increase its dividend year in and year out for 50 years without doing something right.

To be fair, dividend growth is slow right now. The company just announced a dividend increase of roughly 2.5% or so. That's much lower than the 10-year average of roughly 11%. But given that the company is facing headwinds (including inflationary pressures, avian flu, a slowdown in the Planters business, and a slow pandemic recovery in China), that's not shocking.

What's more notable is that management and the board of directors are still positive enough about the future to keep increasing the dividend despite those headwinds.

There's an insider on my side

There's one more factor here that's very unique to Hormel: the involvement of The Hormel Foundation. This entity was created by the founders of the company to both give back to the community and to ensure that Hormel remains a stand-alone company. The Hormel Foundation controls nearly 47% of Hormel stock. This suggests that Hormel is going to remain independent.

But there's another little wrinkle here that's more important. The Hormel Foundation, the largest shareholder, uses the dividends it collects to support its philanthropic activities. So it desires a strong and growing dividend, which is exactly what I want, too. The foundation is also a long-term investor, thinking in decades and not days, so it is willing to deal with temporary near-term weakness in the business so long as the company continues to improve over the long term, just like me.

I believe being aligned with The Hormel Foundation gives me a strong advocate inside of the Hormel Company, which I continue to happily own.

Wall Street is fickle, but long-term value takes time to create

The big disconnect here is that Wall Street is focused on the short term. And there are short-term problems at Hormel. But Hormel is focused on the long term, as am I. There is nothing going on at Hormel that upends my thesis on the company. It continues to operate by the same playbook it has successfully used before. That's very different from, say, Kraft Heinz (NASDAQ: KHC), which is also out of favor.

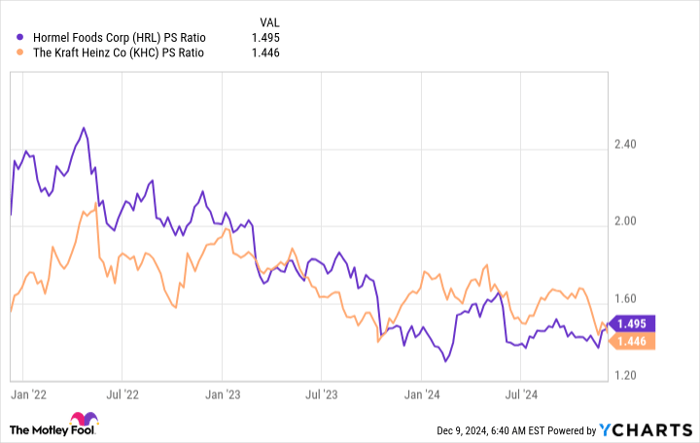

HRL PS Ratio data by YCharts

Kraft Heinz merged two old and bloated food makers with the idea that cost-cutting would lead to improved results. That didn't work out as well as hoped and now the company is focusing on a new approach, owning leading brands and investing heavily in them. And that also isn't working out quite as well as hoped right now.

And then there's the not-so-subtle fact that Kraft Heinz's troubles led to a dividend cut. Sure, the yield is 5.1%, but I would rather own lower-yielding Hormel, the Dividend King. On the valuation front, meanwhile, they have very similar price-to-sales ratios. I believe Kraft Heinz will survive, but I think Hormel is a better company. I'm happy to give up some yield in this situation to own what I believe is the better company.

Sure, it's frustrating to own Hormel right now given its laggard performance, but sometimes that's just part of investing for the long term.

Should you invest $1,000 in Hormel Foods right now?

Before you buy stock in Hormel Foods, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Hormel Foods wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $827,780!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 9, 2024

Reuben Gregg Brewer has positions in Hormel Foods. The Motley Fool recommends Kraft Heinz. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.