Move Over, Uber. Billionaire David Tepper Just Raised Appaloosa's Stake in This Other Ride-Hailing Stock By 98%.

David Tepper is a billionaire hedge fund manager known for founding the Miami-based investment firm Appaloosa Management. Back in September, he sat down for an interview with CNBC during which he expressed an outsized bullish stance on investing in China. Naturally, his comments led many investors to speculate which Chinese stocks the acclaimed investor may like.

Well, thanks to 13F filings, investors have their answer. During the September-ended quarter, Appaloosa scooped up shares in Chinese online retailers PDD Holdings and JD.com.

While I'm intrigued by these moves, Tepper made another decision during the third quarter that I found even more curious. Namely, the billionaire bought 7.8 million shares of Uber's primary rival, ride-hailing platform Lyft (NASDAQ: LYFT), increasing Appaloosa's position by 97%.

Below, I'm going to detail what may have influenced Tepper's decision and explain why I like the purchase. More importantly, I'll assess some valuation trends to help determine if now is an optimal time to follow Tepper's lead and pounce on Lyft stock.

Lyft's quiet turnaround is impressive, and...

Lyft has experienced some notable challenges in recent years. For starters, the COVID-19 pandemic took a toll on the travel industry at large; meanwhile, Uber has spent the last few years turning itself into much more than a ride-hailing app.

Through a series of acquisitions, Uber has started penetrating new markets, including food and alcohol delivery. These moves have turned Uber into a more ubiquitous platform overall, specializing in convenience-as-a-service rather than just an alternative to traditional mobility options.

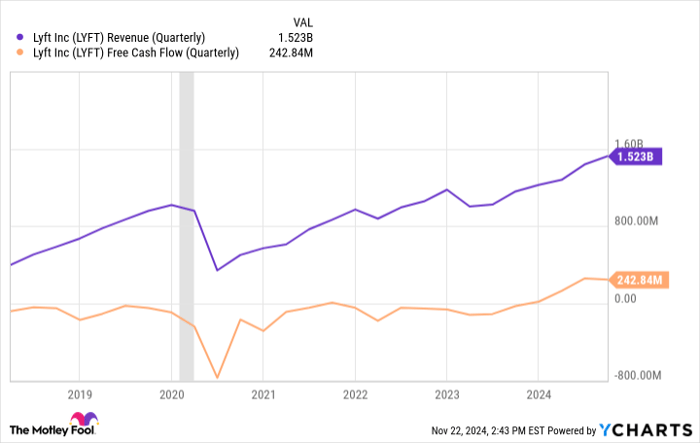

LYFT Revenue (Quarterly) data by YCharts

In the chart above, you can see that Lyft's growth really took a nosedive around the time of the COVID-19 pandemic (shaded in the grey bar). Since then, the trends illustrated above demonstrate that the company has quietly been executing on an impressive turnaround over the last few years.

Let's dig into some of the finer details and explore how Lyft navigated such a challenging environment over the last few years.

Image source: Getty Images.

...the ride could just be getting started

One of Lyft's biggest recent wins is its Price Lock program, which caps prices for riders who frequently take the same rides on a recurring basis. Looked at another way, Price Lock is Lyft's way of trying to acquire commuters on their way to work.

On the surface, I was skeptical that a campaign like this would actually work. After all, why can't commuters just drive themselves or take public transportation such as the subway or bus?

Well, during the company's third-quarter earnings call, management shared with investors that Lyft has 200,000 active Price Lock passes and that "commute rides make up nearly half of rides Monday to Friday."

In some ways, the demand for Price Lock has added a layer of recurring, predictable business for Lyft. And as such, the company has been able to yield stronger unit economics overall.

| Category | Q3 2023 | Q4 2023 | Q1 2024 | Q2 2024 | Q3 2024 |

|---|---|---|---|---|---|

| Gross bookings (in billions) | $3.5 | $3.7 | $3.7 | $4.0 | $4.1 |

| Rides (in millions) | 187.4 | 190.8 | 187.7 | 205.3 | 216.7 |

| Active riders (in millions) | 22.4 | 22.4 | 21.9 | 23.7 | 24.4 |

| Adjusted EBITDA (in millions) | $92 | $67 | $59 | $103 | $107 |

| Free cash flow (in millions) | ($329) | ($248 ) | ($0.2) | $368 | $641 |

Data source: Investor Relations.

There is a lot to unpack from the table above. The most important theme from my perspective is that Lyft has been able to actually translate the uptick in bookings and riders to profitability. At this time last year, Lyft was burning cash. Now, the company is not only consistently generating positive free cash flow, but the rate at which profitability metrics are rising is accelerating.

As the macroeconomic picture continues to strengthen thanks to cooling inflation rates and reduced borrowing costs, I see even better days ahead for Lyft.

Lyft stock looks like a bargain

One thing to note about Lyft's financial profile is that even though the company is now generating positive cash flow, it's still not consistently profitable on a net income basis. For this reason, it's a not entirely helpful to value Lyft using methods such as the price-to-earnings (P/E) or price-to-free cash flow (P/FCF) multiples.

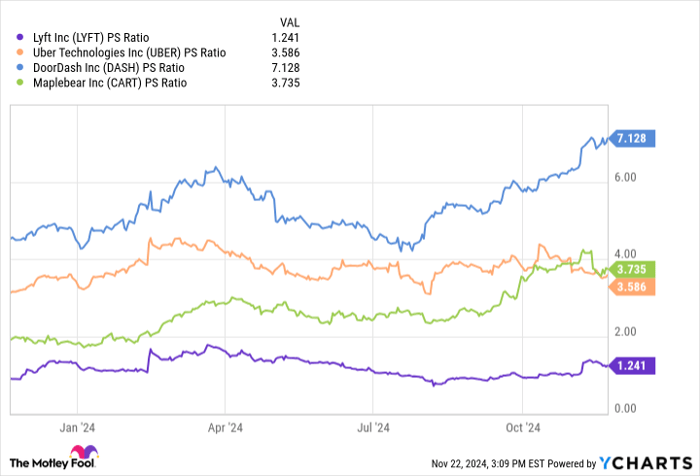

LYFT PS Ratio data by YCharts

Right now, Lyft is only trading at about 1.2 times its sales -- far lower than its peers in ride-hailing and delivery services. I find this dynamic peculiar considering that Lyft is a much more sophisticated and larger enterprise today than it was in the past.

In my eyes, it's this disparity that has been influencing Tepper's decision to double down on Lyft. Tepper looks for deep value stocks, and from my point of view Lyft has essentially been written off in favor of other opportunities in related markets.

I see Lyft as a no-brainer buy right now and think the stock is trading at a bargain. The financial trends explored above suggest the company is finally kicking into a new gear.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $352,678!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,102!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $466,805!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 25, 2024

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends DoorDash and Uber Technologies. The Motley Fool recommends Instacart and JD.com. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.