Endeavour Silver Q2 revenue up 46%, beats analyst estimates

Overview

Endeavour Silver Q2 revenue rises 46%, beating analyst expectations, per LSEG data

Adjusted EPS for Q2 misses consensus, impacted by Terronera losses

Company completed Minera Kolpa acquisition, boosting production capacity

Outlook

Company expects Terronera to achieve commercial production soon

Endeavour Silver focuses on operational efficiency and capital management

Company highlights growth potential from Minera Kolpa acquisition

Endeavour Silver sees expanded resource base enhancing future opportunities

Result Drivers

MINERA KOLPA INTEGRATION - Increased silver equivalent production by 13% due to Minera Kolpa acquisition

HIGHER REALIZED PRICES - Revenue boosted by higher sales volumes and favorable market prices for silver and gold

TERRONERA IMPACT - Operating losses from Terronera project during commissioning phase affected results

Key Details

Metric | Beat/Miss | Actual | Consensus Estimate |

Q2 Revenue | Beat | $85.30 mln | $84.40 mln (2 Analysts) |

Q2 Adjusted EPS | Miss | -$0.03 | $0.01 (5 Analysts) |

Q2 Adjusted Net Income |

| -$9.20 mln |

|

Q2 Net Income |

| -$20.50 mln |

|

Q2 EBITDA |

| $1.40 mln |

|

Q2 Pretax Profit |

| -$14.60 mln |

|

Analyst Coverage

The current average analyst rating on the shares is "buy" and the breakdown of recommendations is 7 "strong buy" or "buy", 1 "hold" and no "sell" or "strong sell"

The average consensus recommendation for the non-gold precious metals & minerals peer group is "buy"

Wall Street's median 12-month price target for Endeavour Silver Corp is C$9.08, about 12.8% above its August 12 closing price of C$7.92

The stock recently traded at 19 times the next 12-month earnings vs. a P/E of 11 three months ago

Press Release: ID:nGNX6jLVxK

Related Articles

U.S. Stock Market Risk Assessment: Learning from History, Mid-Term Outlook Remains Secure

We argue that the Federal Reserve’s monetary policy is the most critical factor influencing the stock market.

Don't Miss Walmart's Aug 21 Earnings: $0.73 EPS Forecast, Grocery + E-Com Dual Engines – Unlimited Upside Potential?

TradingKey - Walmart's stock price has shown an overall fluctuating upward trend since the release of its first-quarter earnings report, benefiting from investors' favoritism towards Walmart as a defensive stock, as well as expectations for its stable growth in e-commerce and grocery businesses.

Powell's Jackson Hole Speech: For U.S. Stocks, Hawk or Dove Signal Could Be a Lose-Lose?

TradingKey - As U.S. inflation and labor market data show signs of rebalancing, Treasury traders and Wall Street banks have largely priced in a rate cut at the September FOMC meeting — the first of 2025. Yet both a more dovish-than-expected tone and a potential surprise hawkish signal from Fed Chair

Eurozone Q2 GDP Commentary: Will the Euro's Upward Momentum Persist?

TradingKey - On 14 August 2025, Eurostat published Q2 GDP figures, revealing a drop in the Eurozone's quarter-on-quarter growth from 0.6% in the first quarter to 0.1%. Consequently, annual growth eased from 1.5% to 1.4%. The slowdown primarily stems from the diminishing boost from European...

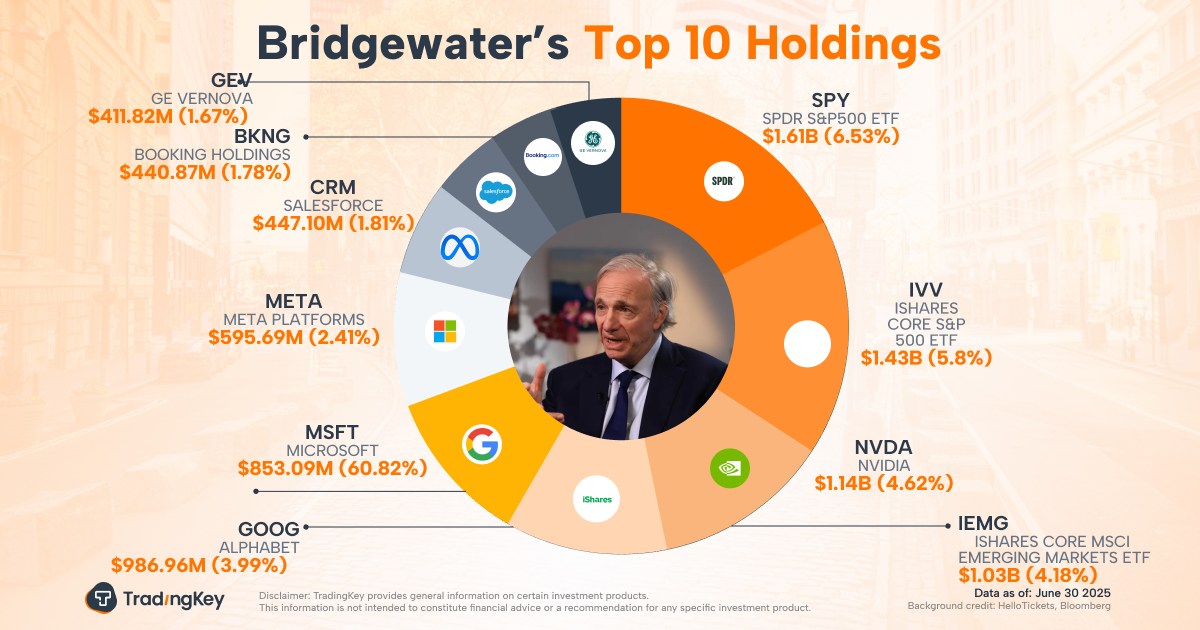

Bridgewater Associates Q2 2025 13F Analysis: Founder Ray Dalio’s Final Act

TradingKey - Bridgewater Associates, the world’s largest hedge fund and renowned for its macroeconomic analysis, continues to command market respect with its “risk parity” strategy and precise economic cycle timing.