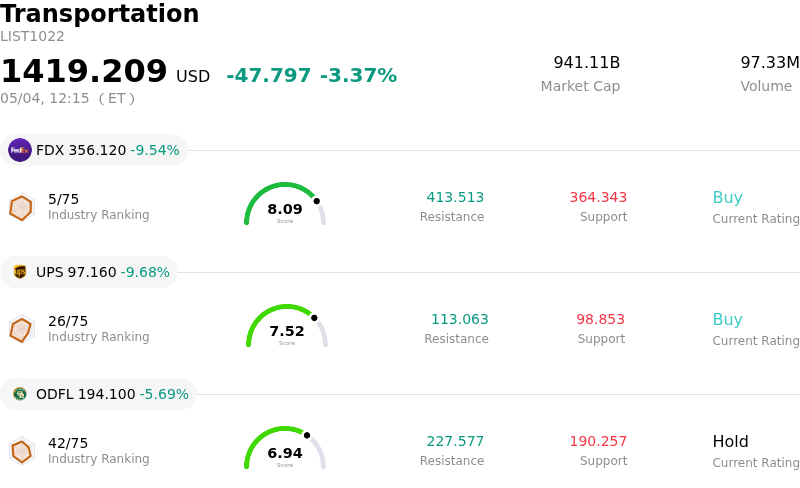

United Parcel Service Inc Stock (UPS) Moved Down by 9.68% on May 4: What Investors Need To Know

United Parcel Service Inc (UPS) moved down by 9.68%. The Transportation sector is down by 3.37%. The company underperformed the industry. Top 3 stocks by turnover in the sector: FedEx Corp (FDX) down 9.54%; United Parcel Service Inc (UPS) down 9.68%; Old Dominion Freight Line Inc (ODFL) down 5.69%.

What is driving United Parcel Service Inc (UPS)’s stock price down today?

The significant intraday decline in UPS's stock price is primarily attributed to a major competitive development in the logistics sector. On May 4, 2026, Amazon announced the launch of its "Amazon Supply Chain Services," making its extensive logistics infrastructure, including freight, distribution, fulfillment, and parcel shipping capabilities, available to external businesses. This move positions Amazon as a direct and formidable competitor to established freight and delivery service providers like UPS and FedEx, creating increased competition within the industry. The market reacted negatively to this news, causing shares of both UPS and FedEx to fall.

This new competitive pressure comes at a time when UPS is already navigating a complex operational landscape. The company recently reported its first-quarter 2026 earnings, which, despite meeting non-GAAP adjusted earnings per share estimates and reaffirming full-year guidance, showed a notable decline in GAAP earnings year-over-year. U.S. domestic and supply chain revenues also experienced decreases during this period.

Furthermore, broader macroeconomic headwinds, such as elevated fuel prices and ongoing shipping disruptions, potentially linked to geopolitical events like the closure of the Strait of Hormuz, have contributed to a fragile sentiment around the stock. UPS has also been engaged in a multi-year transformation strategy aimed at cost reduction, including significant workforce reductions and facility closures, and has been actively reducing its reliance on Amazon volumes. This strategic repositioning, coupled with the new direct competition from Amazon, has led investors to reassess the company's long-term growth prospects and earnings power.

Technical Analysis of United Parcel Service Inc (UPS)

Technically, United Parcel Service Inc (UPS) shows a MACD (12,26,9) value of [1.19], indicating a buy signal. The RSI at 57.98 suggests neutral condition and the Williams %R at -24.17 suggests oversold condition. Please monitor closely.

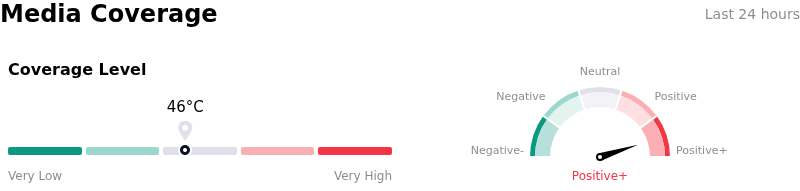

Media Coverage of United Parcel Service Inc (UPS)

In terms of media coverage, United Parcel Service Inc (UPS) shows a coverage score of 46, indicating a moderate level of media attention. The overall market sentiment index is currently in extremely bullish zone.

Fundamental Analysis of United Parcel Service Inc (UPS)

United Parcel Service Inc (UPS) is in the Transportation industry. Its latest annual revenue is $88.66B, ranking 1 in the industry. The net profit is $5.57B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $114.09, a high of $135.00, and a low of $75.00.

More details about United Parcel Service Inc (UPS)

Company Specific Risks:

- Increased competition emerged today with Amazon's launch of "Amazon Supply Chain Services," directly targeting third-party logistics and causing a drop in UPS shares.

- Weakness in the U.S. Domestic Package segment was evident in the Q1 2026 earnings report, showing a 2.3% decline in revenue due to reduced volume, primarily from the company's strategic shift away from lower-margin Amazon deliveries.

- Management's cautious outlook following the Q1 2026 earnings call, where the CEO indicated it was "too early" to raise guidance, contributed to a decline in stock price despite meeting some estimates.

- Ongoing large-scale operational restructuring, including the closure of 23 facilities with 27 more planned and the elimination of 30,000 jobs (including 7,500 driver positions), introduces execution risks and potential for internal disruptions.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.