Amgen Inc Stock (AMGN) Moved Up by 3.25% on Apr 30: Key Drivers Unveiled

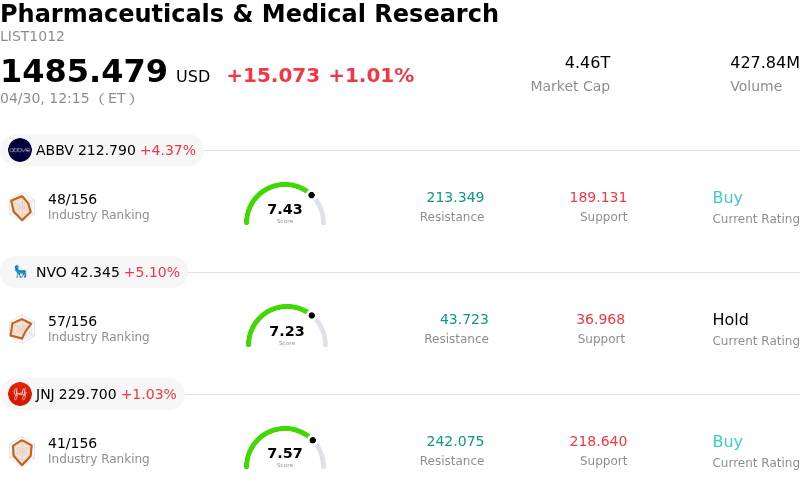

Amgen Inc (AMGN) moved up by 3.25%. The Pharmaceuticals & Medical Research sector is up by 1.01%. The company outperformed the industry. Top 3 stocks by turnover in the sector: AbbVie Inc (ABBV) up 4.37%; Novo Nordisk A/S (NVO) up 5.10%; Johnson & Johnson (JNJ) up 1.03%.

What is driving Amgen Inc (AMGN)’s stock price up today?

Amgen experienced significant intraday volatility, ending the day with a gain of 3.25%. This upward movement occurred amidst a complex backdrop of regulatory concerns, pipeline optimism, and anticipation surrounding its upcoming first quarter 2026 earnings report.

A primary factor contributing to recent market sentiment has been the U.S. Food and Drug Administration's (FDA) proposal to withdraw approval for Amgen's autoimmune drug, Tavneos. This news, which emerged on April 28, cited concerns about the drug's effectiveness, potential manipulation of clinical trial data, and serious safety issues, including instances of liver injury and fatalities. The regulatory overhang created considerable uncertainty and was noted as a source of potential near-term volatility, raising questions about the company's trial integrity. Despite these significant concerns, the stock's positive performance on April 30 suggests that investors may be reassessing the long-term financial impact of the Tavneos situation, possibly viewing it as contained within Amgen's broad product portfolio.

Conversely, market optimism ahead of the Q1 2026 earnings report, scheduled for release after market close on April 30, likely fueled the day's upward trend. Social media chatter indicated intensified investor interest and a generally bullish sentiment, supported by perceived strong fundamentals and other upcoming catalysts. Key pipeline developments, such as positive Phase 3 results for subcutaneous Tepezza in thyroid eye disease and the significant potential of the obesity candidate MariTide, are also contributing to a positive outlook. Analysts have maintained a mixed "Hold" consensus, but recent price target increases by some firms suggest growing confidence in Amgen's drug pipeline. Additionally, the biotech sector generally saw some rallying, with options flow hinting at building momentum, which may have provided a tailwind for Amgen.

In summary, while the FDA's proposed withdrawal of Tavneos presented a notable risk, the market's positive reaction appears to be driven by strong anticipation for Amgen's Q1 earnings results and an ongoing bullish sentiment surrounding its broader pipeline, particularly its obesity drug candidate MariTide. Investors seem to be weighing the potential impact of regulatory issues against the company's robust development prospects and overall financial strength.

Technical Analysis of Amgen Inc (AMGN)

Technically, Amgen Inc (AMGN) shows a MACD (12,26,9) value of [-3.42], indicating a sell signal. The RSI at 37.40 suggests neutral condition and the Williams %R at -81.30 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Amgen Inc (AMGN)

Amgen Inc (AMGN) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $36.75B, ranking 14 in the industry. The net profit is $7.71B, ranking 10 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $355.27, a high of $432.00, and a low of $200.00.

More details about Amgen Inc (AMGN)

Company Specific Risks:

- Analyst downgrade citing limited near-term catalysts, with key growth driver MariTide not expected to provide meaningful updates until 2027, indicating potential for prolonged revenue stagnation.

- Increased competitive and pricing pressures, particularly on established products like Repatha due to emerging rivals, and broader concerns over biosimilar competition and patent expirations for core assets.

- Anticipated Q1 financial headwinds following revised estimates reflecting a projected $250 million sequential channel inventory drawdown, suggesting potential for weaker-than-expected earnings.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.