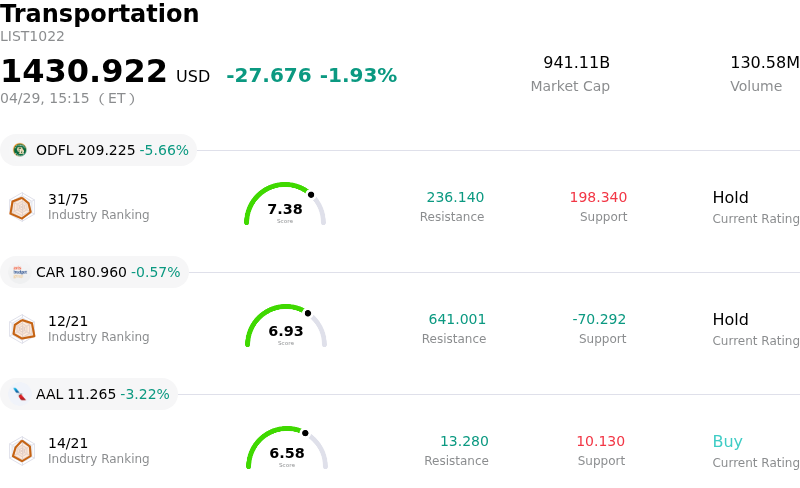

Canadian National Railway Co Stock (CNI) Moved Down by 5.81% on Apr 29: Drivers Behind the Movement

Canadian National Railway Co (CNI) moved down by 5.81%. The Transportation sector is down by 1.93%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Old Dominion Freight Line Inc (ODFL) down 5.66%; Avis Budget Group Inc (CAR) down 0.57%; American Airlines Group Inc (AAL) down 3.22%.

What is driving Canadian National Railway Co (CNI)’s stock price down today?

The share price decline experienced by Canadian National Railway (CNI) appears to be primarily driven by investor reaction to the company's first-quarter 2026 earnings report, released on the same day. While the company largely met analyst expectations for adjusted earnings per share and slightly exceeded revenue estimates, several underlying financial details and the reiterated outlook likely fueled investor apprehension.

A key concern stemming from the earnings report was the deterioration of the adjusted operating ratio, which worsened compared to the prior year. This indicates higher operating costs relative to revenue, a trend investors tend to view negatively. Increased expenses related to winter conditions, various incidents, a higher effective tax rate, and general labor and material costs contributed to this margin pressure. Additionally, freight revenue per revenue ton mile saw a decline, partly influenced by a stronger Canadian dollar and the removal of Canada's federal carbon tax program.

Despite some positive operational metrics, such as increases in revenue ton miles and carloads, and a substantial rise in free cash flow, the market's focus on these cost-side pressures and margin performance overshadowed the positive aspects. Management maintained its full-year 2026 outlook for flat revenue ton mile growth and adjusted EPS growth slightly exceeding volume growth. While this guidance was consistent, it also highlighted ongoing macroeconomic and geopolitical uncertainties that could pose demand risks throughout the year. The market reaction suggests that investors were looking for a more robust outlook or stronger margin performance to justify current valuations.

Broader industry dynamics also paint a picture of a challenging environment for railroads. The general sentiment for the Class I railroad sector in 2026 suggests a largely stagnant year for volumes, with expectations for weaker international intermodal traffic. While some freight categories like grain and chemicals show strength, overall demand remains muted. Potential labor disputes in the Canadian rail sector, despite a past resolution, introduce an element of operational risk that could weigh on investor sentiment. This confluence of company-specific financial performance details and a cautious industry outlook likely contributed to the negative share price movement.

Technical Analysis of Canadian National Railway Co (CNI)

Technically, Canadian National Railway Co (CNI) shows a MACD (12,26,9) value of [1.91], indicating a buy signal. The RSI at 68.89 suggests neutral condition and the Williams %R at -12.28 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Canadian National Railway Co (CNI)

Canadian National Railway Co (CNI) is in the Transportation industry. Its latest annual revenue is $12.71B, ranking 7 in the industry. The net profit is $3.47B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $116.71, a high of $164.00, and a low of $76.04.

More details about Canadian National Railway Co (CNI)

Company Specific Risks:

- Canadian National Railway reported a deterioration in its adjusted operating ratio for Q1 2026 to 64.2%, up from 63.4% in Q1 2025, reflecting increased operating expenses linked to winter conditions and other incidents, thereby compressing margins.

- The company experienced a 1% year-over-year revenue decline in Q1 2026 and faces persistent "heightened demand risk" for 2026, driven by factors such as a stronger Canadian dollar and the removal of the federal carbon tax program impacting freight revenue per revenue ton mile.

- Despite meeting Q1 2026 EPS expectations, the stock price fell over 5% in premarket trading, indicating significant investor apprehension regarding the mixed financial results and the company's operational expenses and flat revenue growth.

- The company's substantial consolidated total debt of $22,624 million as of March 31, 2026, coupled with a debt-to-equity ratio exceeding 100%, introduces financial leverage risk amidst rising operating costs and potential demand headwinds.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.