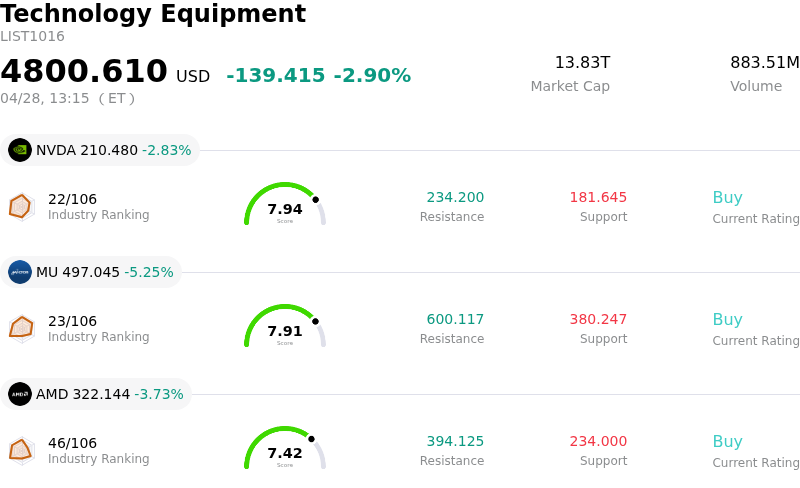

Marvell Technology Inc Stock (MRVL) Moved Down by 3.96% on Apr 28: Key Drivers Unveiled

Marvell Technology Inc (MRVL) moved down by 3.96%. The Technology Equipment sector is down by 2.90%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 2.83%; Micron Technology Inc (MU) down 5.25%; Advanced Micro Devices Inc (AMD) down 3.73%.

What is driving Marvell Technology Inc (MRVL)’s stock price down today?

Marvell Technology (MRVL) experienced a notable intraday decline, primarily influenced by a confluence of factors including revised market sentiment around artificial intelligence (AI) spending and specific concerns raised by analysts. A significant contributor to the negative movement appears to be a report indicating that OpenAI has missed key user and revenue targets, which has fueled investor apprehension regarding the sustainability of the broader AI spending boom. This sentiment negatively impacted several AI capital expenditure-sensitive companies, including Marvell Technology.

Adding to the pressure, analysts have recently voiced concerns regarding Marvell's valuation. One firm downgraded the stock to "Hold" on April 27, 2026, citing an overextended valuation following a substantial rally, placing the stock significantly above its estimated fair value. Another analyst downgrade on April 21, 2026, was driven by the strong conviction that Marvell lost Amazon's custom XPU business to a competitor and potentially faces losing Microsoft as an AI customer, highlighting customer concentration risk and its potential impact on future revenue streams. Concerns have also been expressed about Marvell's custom silicon and XPU outlook, with projected growth for the fiscal year 2027 considered insufficient to justify the current high valuation.

Furthermore, recent insider and institutional selling activity may have contributed to negative market sentiment. Company executives, including the CFO and COO, sold shares in mid-April. Additionally, institutional investors such as FengHe Fund Management and M&T Bank Corp significantly reduced their stakes in Marvell during the fourth quarter. While Marvell recently announced the acquisition of Polariton Technologies to bolster its optical technology portfolio for AI and cloud data centers and reported strong past earnings, these recent headwinds appear to have outweighed the positive developments, leading to the stock's downturn.

Technical Analysis of Marvell Technology Inc (MRVL)

Technically, Marvell Technology Inc (MRVL) shows a MACD (12,26,9) value of [14.73], indicating a buy signal. The RSI at 78.19 suggests buy condition and the Williams %R at -20.91 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Marvell Technology Inc (MRVL)

Marvell Technology Inc (MRVL) is in the Technology Equipment industry. Its latest annual revenue is $5.77B, ranking 22 in the industry. The net profit is $-885.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $125.72, a high of $170.00, and a low of $85.00.

More details about Marvell Technology Inc (MRVL)

Company Specific Risks:

- Multiple analysts have recently downgraded Marvell Technology or reiterated "Hold" ratings, citing concerns that the stock is overextended and trades significantly above fair value estimates, implying considerable downside risk.

- Concerns persist regarding high customer concentration risk, with recent analyst downgrades explicitly tied to a "high degree of conviction" that the company has lost Amazon's Trainium 3 and 4 designs to a competitor and faces a potential loss of Microsoft's AI custom chip business to Broadcom.

- Key company insiders, including the CFO and COO, have recently sold a substantial volume of shares, with reports detailing sales as current as April 28, 2026, and significant insider selling over the last quarter.

- Analysts express concern over the custom silicon/XPU growth outlook, with a projected 20% growth for FY27 deemed weak and insufficient to justify the stock's current high valuation, suggesting a potential slowdown in this critical segment.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.