Intel Corp Stock (INTC) Moved Down by 3.39% on Apr 20: Key Drivers Unveiled

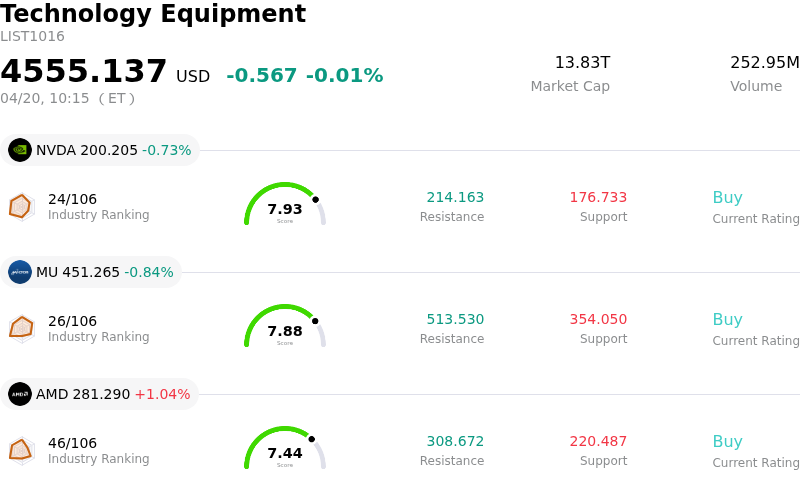

Intel Corp (INTC) moved down by 3.39%. The Technology Equipment sector is down by 0.01%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 0.73%; Micron Technology Inc (MU) down 0.84%; Advanced Micro Devices Inc (AMD) up 1.04%.

What is driving Intel Corp (INTC)’s stock price down today?

Intel (INTC) experienced a downward movement in its share price today, largely attributable to market participants engaging in profit-taking ahead of its upcoming first-quarter 2026 earnings report. The stock has seen a substantial rally throughout the year, reaching near 26-year highs and trading at elevated multiples of its projected earnings for the year. This significant appreciation has led to increasing concerns among some analysts and investors that the stock's valuation has become stretched, making it susceptible to a pullback.

Analyst sentiment, while showing some positive adjustments to price targets from certain firms, remains broadly cautious with a consensus "Hold" or "Reduce" rating. The average analyst price target is below the current trading level, implying a potential downside. Some recent analyst commentary explicitly highlighted that the stock's rapid ascent has outpaced its underlying fundamentals, leading to calls for a downgrade or caution against overvaluation. This cautious outlook, combined with the stock's strong performance year-to-date, incentivized investors to de-risk their positions before the quarterly financial results are disclosed.

Expectations for Intel's first-quarter earnings, set for April 23, include relatively modest revenue and earnings per share. Concerns persist regarding the profitability of its foundry business, which remains a cash-intensive operation facing intense competition from rivals such as TSMC and Samsung. Furthermore, despite positive developments around its 18A process node and strategic partnerships, manufacturing capacity constraints and the need for strong forward guidance, particularly for AI server demand, place a high bar for the upcoming report. The general market sentiment is characterized by high volatility, with futures markets pricing in a significant swing post-earnings, reflecting the uncertainty surrounding whether the company's financial performance can justify its current valuation.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of [3.96], indicating a buy signal. The RSI at 78.20 suggests buy condition and the Williams %R at -6.15 suggests oversold condition. Please monitor closely.

Media Coverage of Intel Corp (INTC)

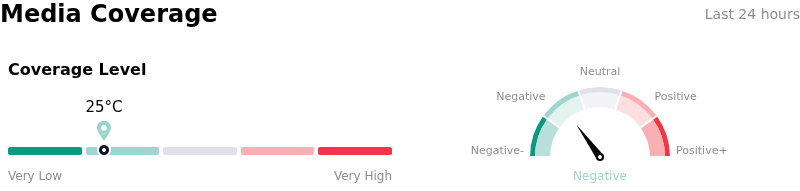

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 25, indicating a low level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 109 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $51.18, a high of $92.00, and a low of $20.40.

More details about Intel Corp (INTC)

Company Specific Risks:

- Intel faces ongoing financial underperformance with its foundry division posting approximately $10 billion in annualized losses and the company reporting declining revenue and gross margins year-over-year, alongside negative free cash flow.

- The company issued a weak Q1 2026 forecast, with revenue projections falling short of analyst estimates and an anticipated break-even earnings per share, primarily due to persistent manufacturing yield issues and acute internal supply constraints hindering its ability to meet demand.

- Intel is experiencing intensified competitive pressure from rivals like TSMC and Samsung, coupled with a lack of significant external customer wins for its foundry nodes, undermining its business turnaround efforts and market position.

- Analyst downgrades indicate that Intel's stock is significantly overvalued, trading at over 100x P/E, with its recent rally driven by future expectations rather than proven fundamental improvements or a clear turnaround in its core business.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.