UK CPI Holds Steady in August — Central Bank Warns of 4% Peak in September! Why Is Inflation So Sticky?

TradingKey - Data released on Wednesday showed that the UK’s Consumer Prices Index (CPI) rose 3.8% year-on-year in August, unchanged from July and remaining at an 18-month high.

While in line with forecasts, the print underscores the persistent stickiness of inflation — a major headwind for the Bank of England as it considers further rate cuts.

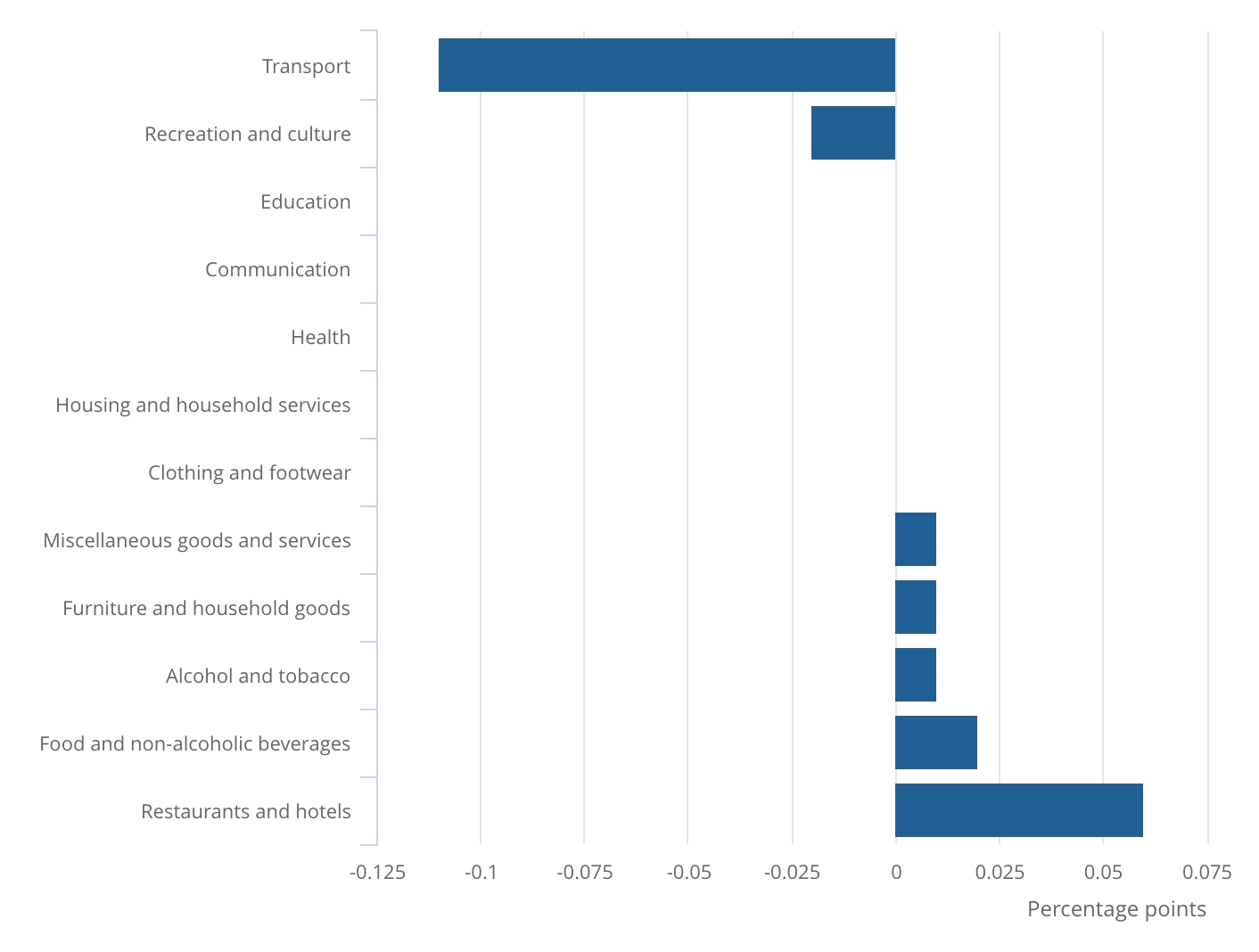

Although airfare prices cooled significantly after the summer travel peak, this relief was offset by continued increases in food, dining, and hotel costs. Food inflation accelerated to 4.8%, the highest since early 2024, with widespread price hikes in vegetables, cheese, and seafood. Services inflation dipped slightly to 4.7%, still well above the BoE’s 2% target.

Source: Office for National Statistics

Analysts attribute the pressure to rising business costs following the Labour government’s April increase in employer national insurance contributions and the minimum wage — costs now being passed on to consumers. Dining and hotel prices rose 3.8% annually, the fastest pace since late 2024.

Meanwhile, a stabilizing labor market and stronger-than-expected GDP growth have eased recession fears, reducing the urgency for monetary easing.

More concerning is the rise in household inflation expectations, which could trigger a self-reinforcing wage-price spiral.

Monica George Michail, Assistant Economist at the National Institute of Economic and Social Research, said current inflation is now “entrenched,” driven by a combination of higher labor costs, elevated inflation expectations, and sustained food price pressures.

The Bank of England now expects inflation to peak at 4% in September.

This persistent inflation has forced the UK to keep interest rates high. In contrast, U.S. inflation has fallen below 3%, while eurozone inflation is nearing the ECB’s 2% target.

Markets widely expect the Monetary Policy Committee to hold rates steady at 4% when it meets on Thursday, with only one more cut priced in by the end of 2026.

As JPMorgan analyst Zara Nokes noted, the path to rate cuts in the UK is narrowing — and may not open up until inflation shows clear signs of retreat.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.