U.S. Liquidity Crisis in August? Fed’s Reverse Repo (RRP) Set to Dry Up, But Barclays Remains Calm

TradingKey - After the U.S. debt ceiling was raised, the Treasury Department has ramped up issuance of Treasury bills to rebuild its cash reserves at the Federal Reserve, draining excess liquidity from the financial system. As a result, the overnight reverse repo (RRP) facility, a key indicator of excess liquidity, is nearing exhaustion and has fallen to its lowest level since April 2021. The potential drying up of excess liquidity adds weight to historical concerns of a “crisis season” during the third quarter.

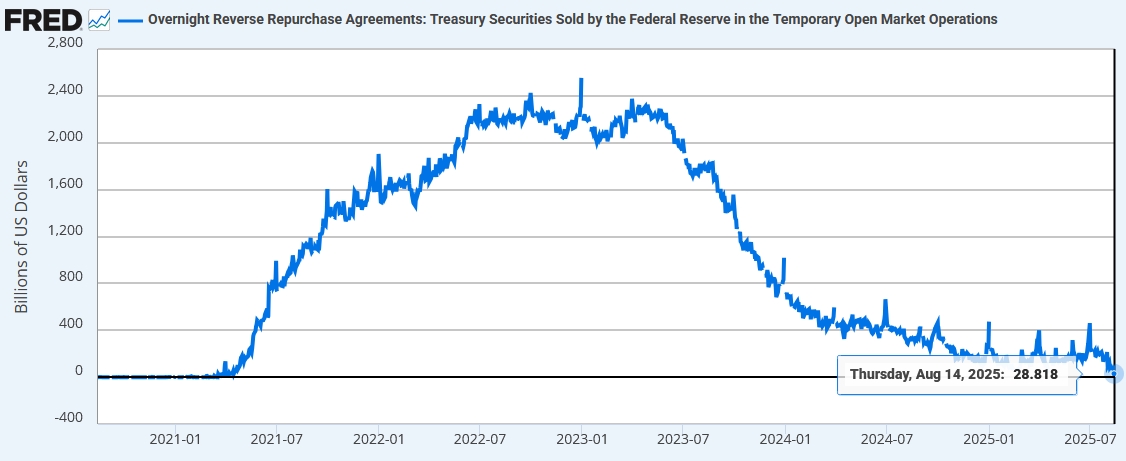

According to data from the New York Fed on August 14, the usage of the Fed’s overnight reverse repo facility has dropped from $240 billion at the start of 2025 to just $28.818 billion, the lowest level in over four years. At the same time, the number of institutional participants has fallen from 62 in July to only 14, the lowest since 2021.

Fed’s Overnight Reverse Repo (RRP), Source: FRED, New York Fed

The overnight reverse repo facility allows the Federal Reserve to absorb excess liquidity from financial institutions such as money market funds and insurance companies, which park idle cash at the Fed to earn interest.

The RRP is widely seen as a “reservoir” for excess funds in the non-bank financial sector, while bank deposits at the Fed are known as reserves. Because the RRP provides a safe, interest-bearing outlet for idle funds, it helps stabilize short-term interest rates and acts as a buffer for bank reserves.

After clearing the debt ceiling hurdle, the U.S. Treasury has aggressively issued Treasury securities — especially short-term T-bills — to replenish its Treasury General Account (TGA) at the Fed. This process drains liquidity from the financial system, first absorbing excess funds in the RRP, and then potentially drawing down bank reserves.

Citigroup analysts project that RRP usage could approach zero by the end of August. Market participants worry that as excess liquidity is “eliminated” from the system, and with bank reserves not as abundant as Fed officials had anticipated, a liquidity crisis may emerge — most visibly through a sharp rise in short-term funding rates.

However, current bank reserves of $3.3 trillion remain at “ample” levels.

Acadian Asset Management noted that most major U.S. market crises over the past 50 years have occurred between August and October. August and September are typically periods of abnormally low market liquidity, which weakens the market’s ability to absorb large, unexpected trades.

Despite the stock market repeatedly hitting new highs, concerns about a “dangerous August” persist. If excess liquidity in the financial system dries up, investors could face a wave of panic.

In a report on August 14, Barclays acknowledged that the market may face a sharp drawdown in reserves in September, with a significant liquidity shock around mid-month. However, due to the market’s demonstrated resilience and the Fed’s deployment of tools to manage liquidity, a systemic funding crisis is unlikely to occur.

Mid-September is seen as a critical period, as September 15 is the quarterly tax deadline, meaning large corporate tax payments will flow into the TGA. Additionally, a large volume of coupon settlements will occur on the same day.

Barclays noted that since August, the market has absorbed a net issuance of $350 billion in short-term Treasuries with relative ease, and the Secured Overnight Financing Rate (SOFR) has only risen slightly. In September, net issuance of short-term Treasuries is expected to be around $30 billion, with the second half of the month likely turning negative — helping to offset the liquidity drain from tax payments.

In short, while liquidity pressures are rising, the system appears better prepared than in past episodes.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.