Will Crypto Explode If Kevin Hassett Takes Over The Fed In 2026?

Kevin Hassett, head of the White House National Economic Council, has suddenly become the market’s base case for the next Fed chair – and crypto investors are already gaming out what a “Hassett Fed” would mean. According to Bloomberg-sourced reporting, Hassett has “emerged as the frontrunner” for President Donald Trump’s choice to lead the Federal Reserve, seen as the candidate most aligned with Trump’s preference for lower interest rates. Earlier disclosures showed Hassett previously served as an adviser to Coinbase and holds at least $1 million in Coinbase stock.

How Will Hassett Impact The Crypto Market?

For crypto allocators, that combination of macro dovishness and direct exposure to a major US exchange is the core of the bull case. Bitwise senior investment strategist Juan Leon put it bluntly on X: “If Kevin Hassett becomes Fed Chair, the implications for crypto are strongly bullish.” He calls Hassett an “aggressive ‘dove’ who has publicly criticized current rates for being too high and advocated for deeper, faster cuts,” highlighting that he “served on Coinbase’s advisory board and owns large stake in COIN,” and that he “led the White House digital asset working group to shape pro-crypto regulation.”

But the potential Hassett regime cannot be separated from Treasury Secretary Scott Bessent’s emerging blueprint for the Fed. Bessent has been openly questioning the post-crisis operating framework. As Walter Bloomberg relayed from his CNBC appearance, “BESSENT ON FED: ‘AMPLE RESERVES REGIME’ MIGHT BE FRAYING.”

Forward Guidance host Felix Jauvin summarized the direction of travel in a post: “Bessent wants a fed chair that gets us out of balance sheet shenanigans and simplifying things to how they were pre-ample regime. Dovish FFR, hawkish balance sheet.” He added: “I don’t know if I can emphasize enough just how far away we are from any sort of QE copium.”

That framing matters for crypto. A Hassett Fed that cuts the policy rate faster in downturns is one thing; a return to full-blown quantitative easing is another. A “dovish FFR, hawkish balance sheet” mix would still be a friendlier macro environment than the post-2022 tightening cycle, but it is not a guaranteed repeat of the 2020–2021 liquidity wave that lifted every risk asset simultaneously.

Rate cuts without large-scale asset purchases support risk appetite and lower discount rates, yet they do not automatically recreate the extreme “everything rally” conditions that many in crypto implicitly associate with Fed dovishness.

The political logic behind Hassett’s rise has been described most clearly by macro commentator EndGame Macro (@onechancefreedm). In a thread, he argues that “Hassett isn’t leading because he’s the most academic or the most central bankerish. He’s leading because he checks the boxes Trump actually cares about.”

Trump, he writes, wants someone he already trusts, who has “spent years defending Trump publicly,” and who has been “openly critical of the Fed for being too slow, too cautious, and too political.” In that framework, “markets hear dovish. Trump hears I can deliver growth again. And crypto folks hear one of us.”

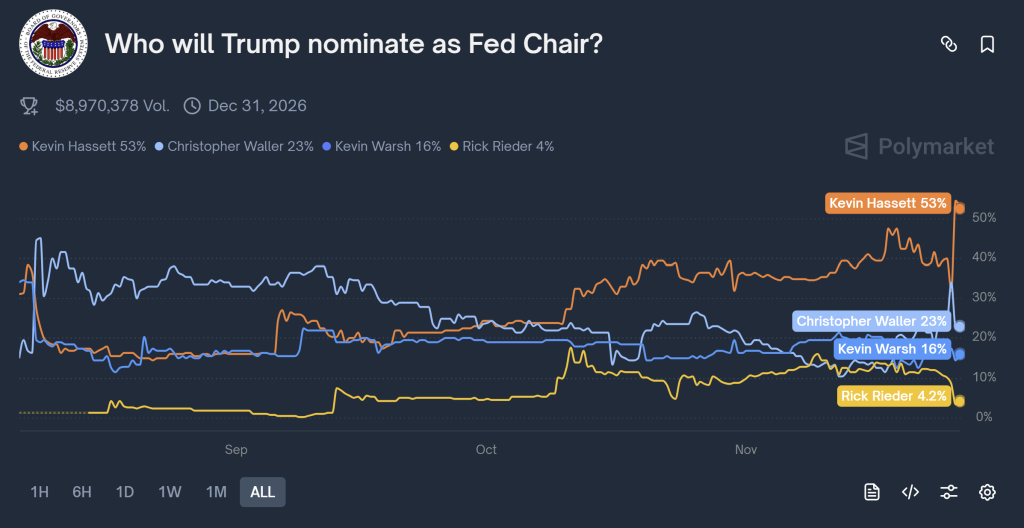

Markets are starting to agree. On Polymarket, contracts tracking the Fed chair race show Hassett around 53% at press time, reinforcing that shift from speculation to probabilistic base case.

Whether that translates into a genuine “explosion” in crypto will depend less on personalities than on the interaction of three forces: how aggressively a Hassett Fed actually cuts, how far Bessent is willing to go in shrinking or simplifying the balance sheet, and how markets reassess inflation, term premia and fiscal risk under a more overtly political central bank.

The odds market is signaling that crypto is moving closer to the center of US monetary power. The scale of any move in 2026 will be determined by the cycle – and by how a Hassett-led Fed balances “dovish rates” with “hawkish balance sheet” in practice.

At press time, the total crypto market cap stood at $2.96 trillion.

Related Articles

National Debt Bomb Ignited? Musk Warns U.S. Will Be 1000% Bankrupt Without AI

TradingKey - Tesla (TSLA) CEO Elon Musk recently issued another warning regarding the rapidly ballooning U.S. national debt. He stated clearly that without artificial intelligence and robotics, the United States will inevitably head toward fiscal bankruptcy.

Why Sanae Takaichi Winning Japan’s Diet Election Led to a Surge in Japanese Stock Indices?

TradingKey - Reports indicate that the ruling coalition led by Japanese Prime Minister Sanae Takaichi has secured a single-party majority in the parliamentary elections held on Sunday (February 8). Following the news, the yen weakened slightly, while the Nikkei Index surpassed 57,000 for the first t

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market