Bitcoin's Dramatic Crash! Key Support at $90,000 Shattered—What’s Next for the Trend?

TradingKey — Bitcoin plummeted over 5%, hitting a low around $86,000. Is a rebound on the horizon?

On Tuesday evening, the U.S. reported its largest drop in the consumer confidence index since 2021, triggering a downturn in the stock market and dragging the crypto market down with it. In the past 24 hours, Bitcoin has fallen over 5%, breaking the critical support level of $90,000, with a low of $86,050 and is currently standing at $88,367.

Bitcoin Price Chart, Source: TradingView.

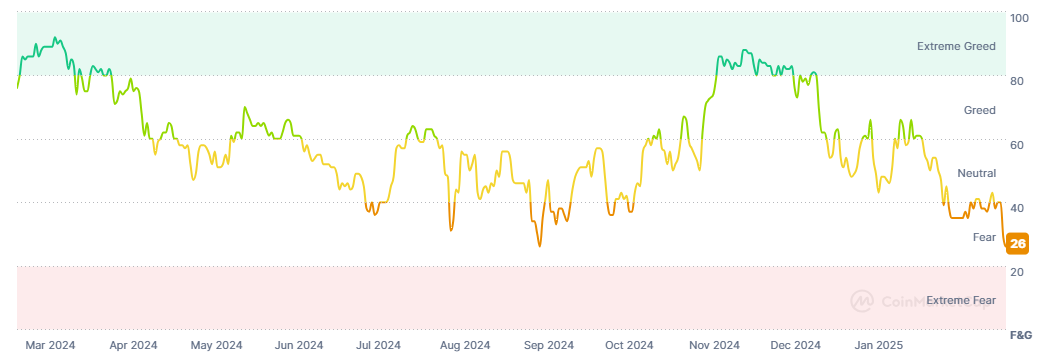

The drop in Bitcoin has led to a significant decline in other cryptocurrencies, many of which have fallen around 10%. This has resulted in liquidations for 230,000 traders, amounting to a staggering $1 billion, sending the market into a state of extreme panic. Data shows that the fear index is at 26, marking a new low since September of last year.

Crypto Fear and Greed Index, Source: CoinMarketCap.

Will Bitcoin continue its downward trend and hit new lows? BitMEX co-founder Arthur Hayes posted on X, stating, "The crypto market is currently in an adjustment phase, awaiting further developments. If President Trump fails to pass his budget proposal to increase spending and raise the debt ceiling, Bitcoin could revisit pre-election levels, around the $75,000 to $70,000 range."

From a technical analysis perspective, with Bitcoin breaking below $90,000, the next support level is indeed around $70,000. From March to October 2024, this level has historically acted as a barrier for Bitcoin's upward movement, now shifting from resistance to support. However, if Bitcoin can rebound and reclaim the $90,000 mark this week, this decline could be seen as a temporary dip.

Despite the grim outlook for Bitcoin, Bernstein maintains its price target of $200,000, believing that "Bitcoin has yet to reach its cycle peak and could approach the $200,000 mark within the next 12 months." Additionally, Bernstein noted that "there may be potential buying opportunities within the current price correction."

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.