TradingKey - Since Trump's return to power, the frequent changes in his tariff policies have become an unstable factor in global financial markets. Since late February 2025, U.S. stocks, bond yields, and the U.S. dollar index have all seen a concurrent decline. The GDPNow model provided by the Atlanta Fed has significantly revised its prediction for U.S. GDP growth in the first quarter of 2025, changing from a positive estimate to -2.4%, which implies that recent economic data point to a minor decline.

In this context, constructing and managing a robust investment portfolio is a primary goal for many investors. Not only does it help preserve and grow wealth, but it also effectively mitigates risk in a complex and ever-changing market environment, supporting the achievement of long-term financial objectives.

It is essential to learn about asset allocation strategies and rebalancing strategies to stabilize our investment portfolios.

What are the Fundamental Principles of Asset Allocation?

Asset allocation is at the core of building a robust investment portfolio, with diversification as its cornerstone.

The essential idea is "not to put all your eggs in one basket."

Theoretically, different assets perform differently amid market fluctuations; by diversifying investments across various asset classes like stocks and bonds, you can reduce the impact of any single asset's volatility on your portfolio, thereby effectively controlling overall risk.

(Source: Shutterstock)

What are the Methods of Asset Allocation?

1. Core-Satellite Asset Strategy

The core-satellite asset allocation strategy divides a portfolio into core assets and satellite assets, similar to the relationship between the sun and its satellites in the solar system.

Core assets operate steadily, while satellite assets provide flexible enhancements.

- Core assets typically account for a larger portion of the portfolio, generally around 60% to 90%. They are characterized by high stability and liquidity, capable of providing relatively stable long-term returns.

- Satellite assets represent a smaller portion, usually around 10% to 40%, using a small amount of capital to seize opportunities. This may include thematic funds focused on renewable energy or overseas markets (QDII). These assets may experience significant short-term volatility but also offer chances for excess returns.

2. Lifecycle Allocation

Lifecycle allocation is a strategy that adjusts asset allocation based on an investor's age and life stage, following the core logic of “taking risks when young and seeking stability when older.”

- Ages 25-35 (Aggressive Phase)

At this stage, you may have just entered the workforce. Although your income might not be substantial, you have ample time and can bear higher risks.

It is recommended to allocate 60%-80% of your funds into stocks or equity funds.

- Ages 35-50 (Balanced Phase)

During this phase, your career stabilizes, but you face pressures such as children’s education and elder care, leading to decreased risk tolerance.

The stock-to-bond ratio can be adjusted to 5:5 or 6:4.

Alternatively, consider investing in "target date funds," which automatically adjust their stock allocations downward and increase holdings in bonds and other stable assets as the retirement date approaches, eliminating concerns about dynamic asset allocation adjustments.

- Ages 50+ (Conservative Phase)

With a more conservative style and lower risk tolerance at this stage, it is advisable to allocate over 60% of your funds into low-risk products such as bonds, money market funds, or bank wealth management products. Equity investments should be limited to no more than 30%.

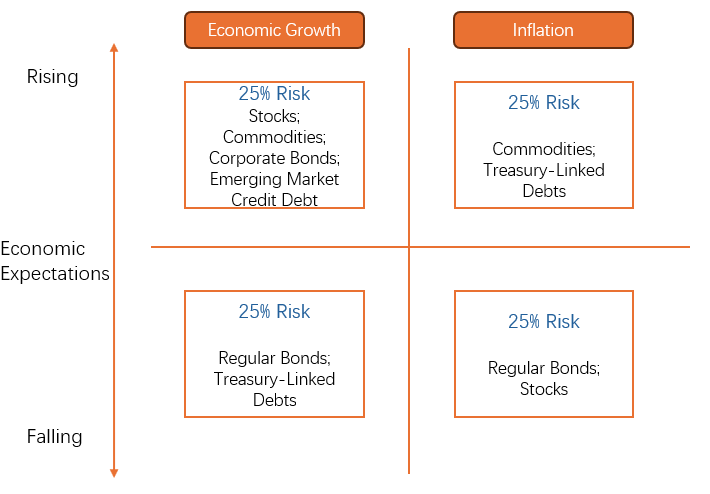

3. Merrill Lynch Clock Method: Adjusting Portfolios According to Economic Cycles

The Merrill Lynch Clock divides economic cycles into four stages: recovery, overheating, stagflation, and recession, similar to the changing seasons:

- Spring: Recovery Phase (Economic Growth ↑, Inflation ↓)

Economies begin warming up with gradually rising corporate profits; equities often perform as the best asset class during this period.

- Summer: Overheating Phase (Economic Growth ↑, Inflation ↑)

In this phase of economic overheating, where prices surge upward, resulting in central banks raising interest rates to curb inflation, commodities become highly sought-after.

- Autumn: Stagflation Phase (Economic Growth ↓ , Inflation ↑)

Here, economic growth stagnates while prices continue rising; holding cash or inflation-protecting assets (such as REITs or inflation-linked bonds) proves more prudent under these conditions.

- Winter: Recession Phase (Economic Growth ↓ , Inflation ↓)

As economies enter decline with deteriorating corporate earnings prompting central banks to cut interest rates, stimulating growth, falling interest rates drive bond prices upward, making government treasuries and high-grade credit bonds safe havens.

4. Strategic Asset Allocation

Strategic asset allocation is a strategy focused on achieving long-term investment goals while considering risk tolerance.

Taking the classic 60/40 stock-bond portfolio as an example, this allocation strategy invests 60% of funds in stocks to pursue long-term asset appreciation, while 40% of the funds are invested in bonds to ensure stability and a certain level of returns.

This combination balances both investment growth and income generation, making it a common and reasonable allocation choice.

5. Tactical Asset Allocation

Tactical asset allocation strategies lean more toward short-term adjustments, requiring sensitivity to macroeconomic data, market interest rate fluctuations, industry development trends, and other factors.

For example, during an economic recovery period with improving macroeconomic data and heightened corporate earnings expectations, the stock market often performs well.

In such cases, you can increase the allocation proportion of stock assets while reducing holdings in fixed-income assets like bonds, allowing you to fully capitalize on the gains offered by a rising stock market.

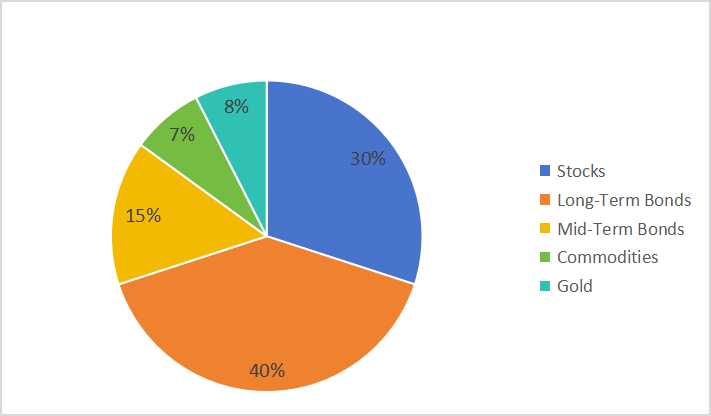

6. All-Weather Strategy

This classic strategy was proposed by Ray Dalio, founder of Bridgewater Associates.

Its core concept involves analyzing economic environments and allocating assets across different categories to adapt to various market conditions.

The economic environment is categorized into four states—a concept commonly referred to as the “four-quadrant” model:

Specific Allocation: 30% stocks + 55% bonds (40% long-term bonds + 15% intermediate-term bonds) + 15% commodities (7.5% commodities + 7.5% gold).

What is a Rebalancing Strategy?

Market fluctuations can subtly change the balance of various assets within your portfolio. For example, if you originally planned for a 60% stock and 40% bond allocation, a significant rise in the stock market might increase your stock allocation to 70%.

At this stage, your risk tolerance may have shifted from your original plan.

Rebalancing is the crucial action that helps bring your investment portfolio "back on track." The core logic of rebalancing is to sell off assets that have increased significantly (selling high) and buy into assets that have not performed as well (buying low), thereby restoring each asset's proportion to its original allocation.

(Source: Shutterstock)

What are the Types of Rebalancing Strategies?

1. Calendar-Based Rebalancing

This method is very straightforward: you set a fixed period (such as quarterly, semi-annually, or annually) to check your portfolio.

For example, you might log into your account on January 1st each year and find that your stock allocation has risen from 60% to 65%. In this case, you would sell 5% of your stocks and buy bonds to restore the ratio to 60:40.

2. Threshold-Based Rebalancing

This method involves setting a volatility "alert line" for each asset (for instance, allowing a deviation from the target allocation of 5% or 10%).

If you determine that the stock allocation should not exceed 65%, but market gains push it up to 66%, you would immediately sell 1% of your stocks and buy bonds.

3. Constant-Mix Strategy

In this strategy, investors maintain fixed allocation ratios across different asset classes.

Even a deviation of just 1% warrants an adjustment.

Regular checks and adjustments ensure that each asset class remains within designated ranges of its target allocation.

While this strategy can respond quickly to market changes, it may incur higher trading costs compared to calendar-based strategies.

4. Dynamic Rebalancing

Dynamic rebalancing strategies offer more flexibility compared to the previous strategies, adjusting target asset allocations based on continually changing market conditions and the investor's financial situation.

However, this approach may be more complex to implement and is suited for investors with a certain level of market judgment.

The "Pros" and "Cons" of Rebalancing Strategies

Benefits:

Rebalancing can help avoid excessive overheating of any single asset, thereby achieving risk control.

It employs a passive strategy of buying low and selling high: the more the market rises, the more you sell; the more it falls, the more you buy.

This rule-based approach helps eliminate emotional decision-making, avoiding greed during market surges and fear during downturns—something most retail investors struggle to achieve.

Potential Costs:

There are trading costs involved; rebalancing often entails frequent trading, which can lead to increased transaction fees.

Additionally, there are tax implications: selling profitable assets may trigger capital gains taxes (for example, in U.S. markets).